Rate sheet influential MBS prices took took a beating yesterday. The bond market's behavior was so unfriendly that Best Execution mortgage rates nearly shifted higher as a result. The main motivation behind this unfavorable directional display was a significant rally in stocks.

Although this market event didn't break any long-term positive trends in bonds, it was certainly scary enough to make one question the strength of our bullish bias. Fortunately that skeptical stress was alleviated today. Stocks erased all of yesterday's gains and the bond market recovered all its losses. Lenders repriced for the better and home loan borrowing costs corrected. Best Execution mortgage rates didn't rise. Bullet dodged!

Why did stocks tank? This headline played a major role in "outing" entrenched technical weakness.

(Reuters) - Greeks rage on austerity, PM offers to quit: Greece's prime minister offered to quit and make way for a national unity government after mass protests against a new austerity plan turned violent on Wednesday, with the country teetering on the brink of default. The dramatic move came after euro zone finance ministers failed to agree on how to involve private investors in a second financial rescue for highly-indebted Greece, and senior EU officials said a deal was now unlikely to be reached at a summit next week and was likely to be delayed until mid-July. Tens of thousands of angry Greeks massed outside parliament to demonstrate rising hostility against draconian spending cuts required to win a second bailout. Rioters hurled petrol bombs at the finance ministry and police fired volleys of tear gas in clashes in the main Syntagma Square as protesters tried to stop lawmakers adopting new tax rises, spending cuts and sell-offs of state assets. Growing risks to the Greek budget plans and signs of deep divisions over the role private creditors should play in a new aid package pushed the euro to a two-week low against the dollar and sent bond yields of peripheral euro states rocketing.

Plain and Simple: After more than a year of "kicking the can down the road", we seem to be nearing a tipping point in the EU debt crisis situation. Every country for itself? The return of the drachma? Debt markets are certainly acting as if default is imminent.

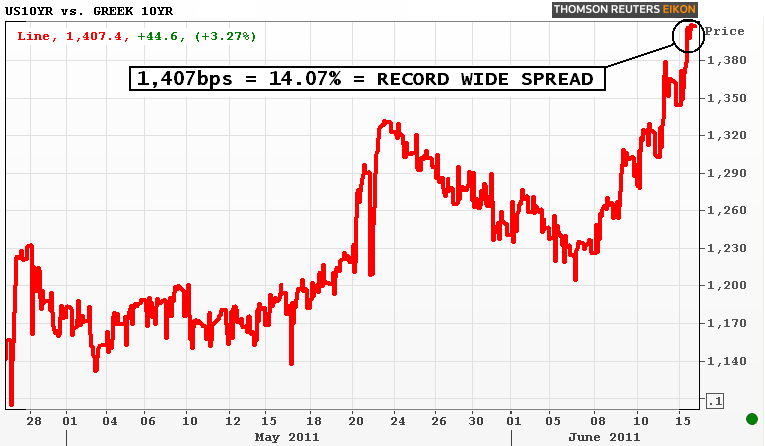

The spread between benchmark 10yr U.S. debt yields and benchmark 10yr Greek debt yields gapped out to a record wide level today. The Greek 2-year note is now yielding 26.8%. Their 10yr note went out at 17.7%.

The Euro lost 1.86% vs. the U.S. dollar as a flight to safety poured into dollar denominated assets....

U.S. equities proved that yesterday's rally was purely a desperate measure taken to defend against a breakdown of 1270 technical support. S&P futures went out down 25 points (-1.94%) at 1266.00. Failure to move back above 1270 in the near future would be considered a bearish breakdown for stocks, which could lead to capitulative selling. Equities are just barely hanging on here...

The U.S. 10-year note completely recovered from yesterday's scary sell-off, again thanks to a flight to safety into dollar denominated assets. Technial support held near 3.10%. The post-jobs data rally remains intact as does our long-term bullish bias. 10s went out +1-03 at 101-09 yielding 2.975%, 12.6bps better. The yield curve bull flattened 6bps to 260bps wide...

Aaaaaand production MBS coupons played follow the leader into higher price territory (from a widening distance...12 ticks at 70% hedge ratio). The Fannie Mae 4.0 finished the day +17/32 at 100-23. At 5pm I had the secondary market current coupon marked at 3.911%, 6.3bps lower on the session but 6bps wider to the 10yr note yield and 3bps wider to swaps.

Still, lagging performance or not, Fannie 4.0s bounced off our Fibonacci Fan target last night and rallied higher today. Reprices for the better were reported.

CURRENT GUIDANCE: Today's recovery rally is encouraging from a big picture perspective as it keeps the door open for our longer-term bullish mortgage rate bias to extend deeper into the summer months. Still, short-term scenarios should take caution. The past few days provide a perfect example of how quickly unfriendly corrections can occur in the mortgage market. Hopefully these back-ups illustrate why we normally urge defensive short-term stances, even as rates improve. We may have dodged a bullet today, but we're not out of the woods yet. More bouts of volatility are very possible.