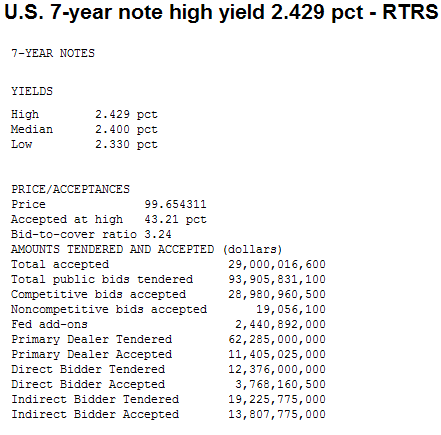

Treasury just finished its final auction of the week with a $29 billion 7-year note offering.The fundraising process went smoothly, completing the 2s/5s/7s trifecta with ease even though the curve continues to trade at extremely overbought levels.

Demand as measured by the bid to cover ratio was 3.24 bids submitted for every one accepted by Treasury. That is the highest BTC ratio we have on record for 7s. Bidders were also willing to pay up for this issue as demonstrated by the 2.429% auction high-yield vs. the 1pm "When Issued" yield of 2.438%.

Direct buyers were the top star, taking down a well above-average 13% of the issue and 30.5% of what they bid on. Directs tendered about $4bn more than usual here which indicates a burning desire to add inventory (short covering).

Indirects were average participants but like directs they tendered about $4bn more than normal, which indicates a need to add inventory. Last but hopefully least, the Dealer award was slightly below average even though the street tendered almost $6bn more than usual, which smells like an inventory shortage!!!

By now we hope you've noticed our repeated comments on upsized bidder tenders. Not just from one account base though, from all three competitive bidders: dealers, directs and indirects. This is the main headline. It means there were many willing buyers in this auction, some folks (directs) were just a bit more aggressive than others. Those who failed to pick up much needed inventory did so because they were only willing to buy at cheaper prices/higher yields.

Plain and Simple: There is clearly no shortage of demand for U.S. debt (thx to large short base in belly of curve). That demand was illustrated this week. Indirects were the aggressor yesterday, direct bidders were the lucky winners today. That leaves dealers on the short end of the stick...in need of inventory.

The bond market hasn't rallied on in the aftermath but that's OK because we're still hovering near the best levels of the session regardless of stocks, which just printed new intraday highs themselves.

S&P futures +0.49% at 1323

10s +13/32 at 100-12 yielding 3.083%.

2s/10s curve 1bp flatter at 258bps wide

FNCL 4.0s +13/32 at 100-21

FNCL 4.5/4 swap at 3-03 (stack compressing)

GN/FN swap still in outer space at 1-27.

Reprices for the better are still very possible.