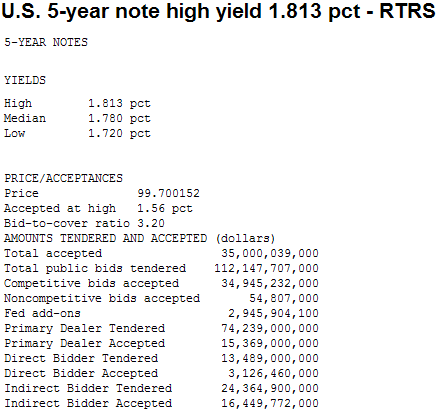

Treasury just auctioned $35 billion 5-yr notes.

Demand metrics were strong on all fronts. The bid-to-cover ratio came in at 3.20 bids submitted for every one accepted, which is well-above recent averages. Treasury was able to sell 98 percent of the issue at a price above the lowest bid tendered by auction participants (good for taxpayers. sell at higher prices!). Because of that the high-yield (1.813%) was 1.6bps below the 1pm "When Issued" bidder yield.

In terms of the buyer breakdown, indirect accounts were the clear cut MVP with a well above-average 47.1% award. Dealers and Directs were non-factors with subpar awards and hit rates. In all actuality, the buyer breakdown is sorta ho-hum besides the massive influx of indirect bidder demand ($24bn tendered = huge). Dealers did tender a larger $$$ amount than usual, which makes sense given their large short position in the 5-yr note, but someone else outbid them, as illustrated by the bidding metrics above and the indirect award. Hedge Funds covering short positions or Central Bankers putting cash to work? Likely both.

Plain and Simple: This was a strong auction because indirect bidders made it strong. Dealers behaved like very willing buyers based on their upsized tender size($74bn vs. $66bn previous), but they weren't willing to pay the more expensive price tag like indirects. This leaves the street in an awkward position... praying for higher rates to allow for cheaper short covering down the road. Smells like a short-squeeze is brewing (either that or a massive selloff-doubtful).

Much like the market's reaction to yesterday's 2yr auction, TSYs are again rallying after today's 5yr auction. 10yr notes initially moved down to 3.11%, exactly like yesterday, but have since been able to extend the rally down to the morning yield lows near 3.09%. MBS are taking part in the price move as well with FNCL 4.5's up about 3 ticks since the auction at 103-18, but have been unable to test the intraday high of 103-21.

This greatly reduces risk of reprices for the worse. Reprices for the better are possible if the post-auciton rally can be extended back to the best levels of the day, but resistance isn't far ahead.

re:Potential Short Squeeze

There's a whole lotta paper shuffling going on out there in the bond market, not much legit directional movement. It seems like everyone is waiting for something bad to happen. Waiting for a levee to break. If a bond bearish event does come (steady drip lately) and dealers haven't squared up their short positions, a snowball rally could push 10s all the way to 2.85%. On the flip side, because the market is heavily short 5s and 10s, even the slightest bit of negative momentum could lead to snowball selling. The short base would gladly pile on new short positions if it meant they'd get the chance to square-up for free at lower prices. There'd be no one to catch the falling knife (unless shorts were covered