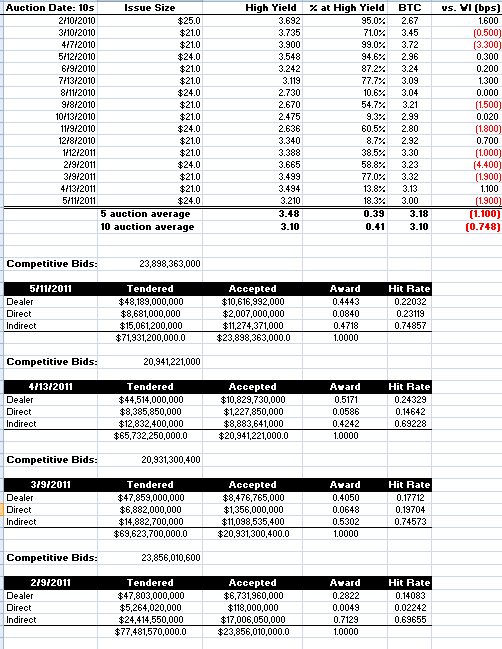

Treasury just auctioned $24 billion 10-year notes. Every bid below 3.210% was accepted by Treasury, which was 1.9bps below where the market had priced the issue at 1pm ("When Issued" note yield). A 1.9bp "tail" indicates demand for this debt offering was strong. Subtracting a bit from that optimism was a relatively weak "bid to cover" ratio, which at 3 bids submited for every 1 accepted, was below average. It's hard to complain anytime you see 3x demand in an auction though.

As far as who got what goes...

Dealers were the aggressive bidder of note today, adding $10.616bn in newly-issued 3.125% coupon 10yr note inventory. This represented an above-average 44.4%of the competitive award and a supply hungry 22% of what dealers bid on (tendered $48.189bn).

Direct bidders weren't apathetic but they didn't chase too hard either. At 8.4% their takedown was slightly above recent averages, but as a whole directs were average buyers. The same can be said about indirects, who took home a slightly below average 47.2% of the competitive bid and 74.9% of what they bid on.

Plain and Simple: Overall it was a strong auction. We remain skeptical of the underlying motivations though. The 1.9bp tail tells us folks needed some inventory here. It appears the market was comfortable with the concession it priced in before the auction. The relative weakness seen in the bid to cover ratio indicates a defensive inclination to overbid this issue though. Smells like short covering.

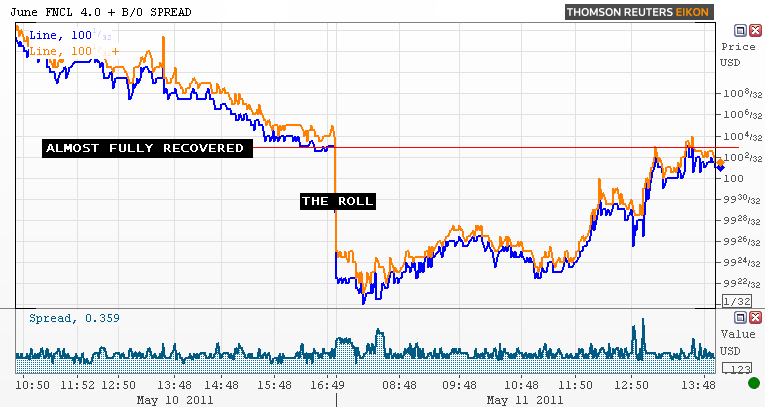

Market Reaction....

Rates rallied! Benchmark 10s shot like a rocket from 3.215% to 3.153%, helping lead the June delivery FNCL 4.0 to almost a full-recovery from the "the drop". This warrants reprices for the better!

The underlying motivation?

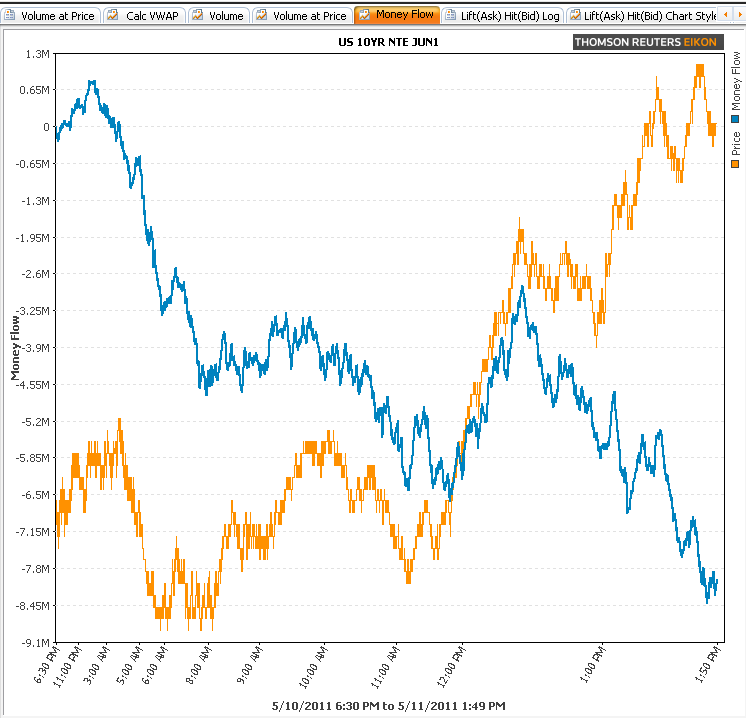

Short covering was obvious before and after the auction in the 10yr TSY futures contract....

Short covering has played a pivotal role in the ongoing rates rally. "Short covering" is when a bearish trader closes a position that was opened with the intention of capitalizing on lower prices/higher yields. The term "short" describes the trader's directional bias. "Covering" simply means closing the position. The resulting effect of short covering is a contraction in "open interest", which represents the number of open contracts in the marketplace. If a trader has set a short position and prices continue to rise, then their position is considered to be under water or "in the red". Leaving a short position open as rates continue to rally can be dangerous because the position gets more expensive with every uptick in price. So it should make sense that as rates have continued to rally it has forced more short covering which has led to snowballing in the bond market. When prices fall and shorts are covered into lower levels, it means investors are waving the white flag on their bearish positions but it doesn't mean there is more rally to come.

Plain and Simple: We're still defensive. This behavior is encouraging, especially when done so in mass, but it must be intensified by real money investors (as opposed to fast$) who need to move their funds "down in coupon". It must also be backed by a CONFIRMATION of weaker economic fundamentals and shorter hedge ratios....

ALERT: REPRICES FOR THE BETTER REPORTED