Can killing the world's most infamous terrorist give a boost to global equity markets?

The markets unambiguously answer: yep.

After President Obama told the world that U.S. forced has gunned down Osama Bin Laden, Dow futures jumped as much as 100 points and Asian markets soared. 60 minutes before the opening bell, S&P 500 futures are up 0.50% at 1366 points and Dow futures are up 0.56% to 12,827. These half-percentage point gains follow a strong rally last week which pushed the Dow up 304.6 points, or 2.44%. Year-to-date the blue chip index has now jumped 1,233 points, or 10.65%.

Strength in stocks has benchmark yields slightly higher to start to the week. The 10-year note is -4/32 at 102-21 yielding 3.305%. The FNCL 4.5 MBS coupon is -1/32 at 102-28.

Key Events This Week:

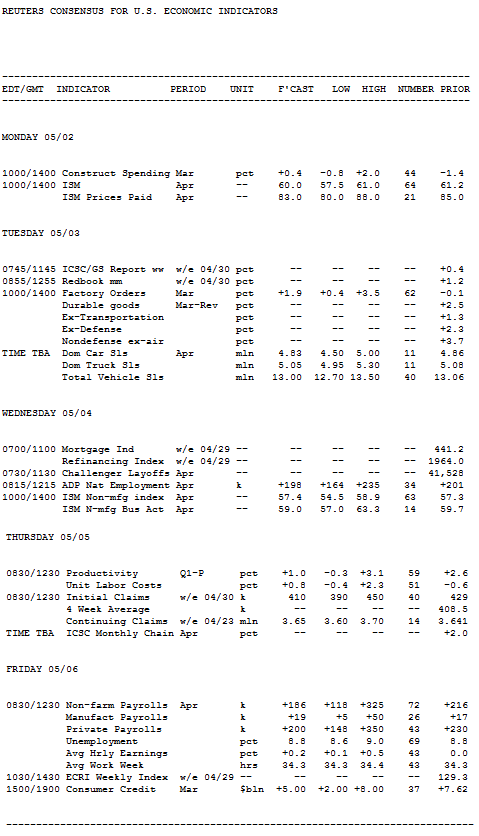

Monday:

10:00 - The economy may have only grown at a 1.8% pace in the first quarter, but manufacturing growth was robust thanks to demand from emerging global economies. The ISM Manufacturing Index boasted levels above 60 for each of the past three months, representing the best quarter since spring 2004 and, according to Citigroup, the highest levels of orders, production and employment of the past 25 years.

Any score above 50 marks growth in the sector, and any reading above 42.5 co-relates with broader GDP growth. Economists aren't so sure the growth will continue at so healthy a level in the current quarter. Forecasts for the April survey range from 58 to 60.5 - all below the 61.2 score in March - and the consensus is at 59.5

"Manufacturing currently is one of the strongest sectors and is leading the recovery," said analysts from Citigroup. "But some automakers are reporting supply disruptions that could hamper output in coming months. Vehicle assemblies have slipped in April. We look to business surveys for a first indication that these disruptions are widening out."

Economists at IHS Global Insight point out that regional reports from Philadelphia, Richmond, and Dallas "have all showed less strength than in prior months, so some softening is not hard to anticipate."

Still, they said a score of 57.5 would be "robust," versus "exceptional" levels in the first quarter.

"A wildcard that could push the index higher is complaints about vendor performance following the earthquake in Japan, as both motor vehicle and electronics makers scramble to get supplies," they wrote. "The index calculation interprets slower deliveries as a sign of strength, regardless of whether they result from booming demand or from an interruption of supply."

10:00 - Look for a modest rebound in Construction Spending, economists say. While new construction activity fell 3.2% in December, 1.8% in January, and 1.4% in February, the expectation is for a 0.5% bump in March as employment began to pick up.

Forecasters at BBVA look for a 0.8% advance, based on increases in public expenditures for infrastructure projects. "Residential building may rise as well as housing starts increased in March but non-residential building will still remain weak for several months. However, the construction sector continues to be a drag on the economic recovery."

The March employment report showed construction jobs climbed by a revised 37,000 in February, which according to IHS Global Insight is the largest increase in 47 months. However, they are not convinced the employment gain will translate into bigger spending.

"Nonresidential construction still has months to go before it hits bottom," they wrote. In a report last month they added: "This sector is performing worse than housing - it is still contracting, while housing has been stuck at the bottom for the past 24 months."

Forecasts for the report very widely, from -0.5% to +1%.

- Treasury Auctions:

- 11:30 - 4-Week Bills

- 11:30 - 3-Month Bills

Tuesday:

10:00 - Factory Orders are anticipated to jump 2% in March. Economists can be reasonably confident in their optimism after the new orders for durable goods figure jumped 2.5% in March and February orders were revised to +0.7% from -0.6% previously.

"It appears that the vehicle manufacture industry contributed 1.4% to total output growth of 1.8%," said economists at Janney Capital Markets, referring to GDP. "That's quite the impressive performance, one based on an uptrend in auto sales from an average annual rate of 11.6 million in 2010 to 13 million in the first three quarters of the new year. As the first quarter growth numbers show, the domestic economy depends hugely on the auto industry as a source of continued expansion."

Analysts at Citigroup added that a large gain in petroleum products will provide a boost on top of durable goods orders, and that spike "will probably be repeated in April as the spot price for crude oil continued to rise."

- Treasury Auctions:

- 11:30 - 4-Week Bills

- 11:30 - 52-Week Bills

Wednesday:

8:00 - Eric Rosengren, president of the Boston Fed, speaks to the NAIOP (the Commercial Real Estate Development Association) in Boston.

8:15 - The growth of private jobs is expected to be trimmed a bit in April. Forecasts for the ADP Employment Report find a median at 195k, versus 201k new jobs in March and 208k in February. Forecasts range from 165k and 240k.

In part because of this report's volatility, economists don't generally provide commentary for their forecasts on the ADP figures, but a surprise in either direction can cause last-minute revisions to forecasting Friday's nonfarm payrolls report.

10:00 - Like its manufacturing cousin, the ISM Non-Manufacturing Index has been particularly robust in recent months. A key measure of the services, financial, and construction industries, this survey has reported readings of 59.4 and 59.7 in January and February, then 57.3 in March. Economists look for a marginal reduction to 57.0 in April, but only 50 is required to show growth.

"The services industry seems to be having its day, an assessment supported by the 9.3% annualized increase in software investment recorded during the first quarter, as well as earnings trends from the likes of healthcare and IT providers, sectors in which companies have experienced sales growth of 5% and 20%, respectively," said economists at Janney Capital Markets. "Moreover, the services sectors are less sensitive to higher commodities costs, an area which has taken on greater importance in recent months."

3:00 - John Williams, president of the San Francisco Fed, gives his first policy speech on maintaining price stability in a global economy, in Los Angeles.

7:00pm - Dennis Lockhart, president of the Atlanta Fed, speaks on the economic outlook to the National Funding Association in Atlanta.

Thursday:

8:30 - Initial Jobless Claims have been a major disappointment so far in April. The report has posted above-400k levels for the past three weeks, causing the four-week average to jump 15k from the March average, to 408.5k. The last week was the worst, as new claims for unemployment insurance unexpectedly surged 25k to 429k - the highest since Jan. 8.

Economists anticipate 410 new claims in the week ending April 30.

"Initial jobless claims probably retreated, but remained above 400,000 a fourth week," said economists at Citigroup. "There is a risk that first filings could be dampened during the survey period as a series of catastrophic storms affecting 21 states might delay filings or reporting in seriously effected areas.

" ... Certain states have noted modestly increased filings from the auto and transportation sectors. It is not clear if these are due to intermittent shutdowns of certain Japanese car manufacturers or other factors. On balance, it appears that claims have been little impacted by the global supply chain disruptions, but this could change as key inputs become scarcer in coming months."

8:30 - The first-quarter Productivity & Costs report should back up what we already know from the recent GDP release, which showed the real growth rate falling to 1.8% from 3.1% in the fourth quarter. The productivity numbers may not look good, but they point to job growth in the coming months as companies face the reality of needing more workers to keep productivity rising.

Productivity levels should come in at +1.3% - half the pace of growth in the fourth quarter - while unit labor costs should rise 0.8% versus a 0.6% cutback in the prior quarter.

"The sharp rise in labor productivity growth during 2009 and 2010 is mostly the result of cost cutting," said economists at IHS Global Insight. "This strategy has reached its limit, and in order for companies to expand to meet growing demand, they will need to increase hiring. As a result, productivity growth is slowing down."

9:30 - Ben Bernanke, chairman of the Fed, speaks at the Chicago Fed's Annual Conference on Bank Structure and Competition in Chicago.

11:00- Treasury announces the terms of 3-yr, 10-yr, and 30-yr debt to be auctioned in the following week

1:15 - Narayana Kocherlakota, president of the Minneapolis Fed, speaks on contingent planning for monetary policy in Santa Barbara, California.

The April MBS prepayment report will be released late Thursday afternoon.

Friday:

8:30 - The recent rise in initial jobless claims doesn't bode well for April's Employment Report, the most closely-watched report in the nation. While economists anticipate nonfarm payrolls to grow by 185k in the month, that growth is quite a bit down from the 216k new jobs created in March. The Unemployment Report is to remain at 8.8%, after a precipitous fall in previous months, and the average workweek should stay at 34.3 hours.

The good news is that this growth does reflect real jobs, rather than government stimulus programs or temporary blips. The bad news is that public sector hiring is likely to continue falling as local governments struggle to balance budgets without taking on much new debt.

"It appears that job growth has reached a sustainable level, with expansion set to continue at a 150 - 250 thousand pace per month without outside influence," said economists at Janney. "Our current base case forecast has population growth-adjusted payrolls returning to pre-recession levels only by 2016. In the short term, the April uptick in weekly initial jobless claims has cast a doubtful eye on the recent improvement in labor market trends."

3:00 - Consumer Credit has been rising for five consecutive months now, most recently improving $7.6 billion on February. But the headlines can't be trusted entirely.

Revolving loans that are closely linked to consumer activity - including credit card loans - were trending lower in recent months, according to economists at Nomura Global Economics. Indeed, revolving credit contracted $2.7 billion in February, and the boost to non-revolving credit was entirely due to federal loans.

The March report is expected to keep this contrast going. The headline figure should show consumer credit was up $5 billion, but the details are what will matter.

Mortgage Rates: As Good As It Gets?