Rate sheet influential MBS coupons hit new one-month highs today.

REPRICES FOR THE BETTER HAVE BEEN REPORTED

Following reprices for the better, on average among the five major lenders, C30 rebate is 25.2bps more aggressive than it was on Friday afternoon. These gains are in-line with price appreciations in the secondary market. The largest improvements are seen in note rates below 4.875% but the cost to permanently buydown the rate from 4.875 to 4.75 is still almost 1 point, on average. That is expensive! It would take borrowers 10+ years to recover the upfront fees they paid at closing to obtain this permanent buydown. We have however noticed a few lenders pricing 4.75% at rebate levels that would allow an originator to quote this rate with lower costs, but that deal would be very skinny, especially with new LTV risk-based pricing adjustments. A wide gap between 4.875 and 4.75 pricing will be obvious on rate sheets until lenders are able to hedge their pipelines with 4.0 MBS coupons. READ MORE

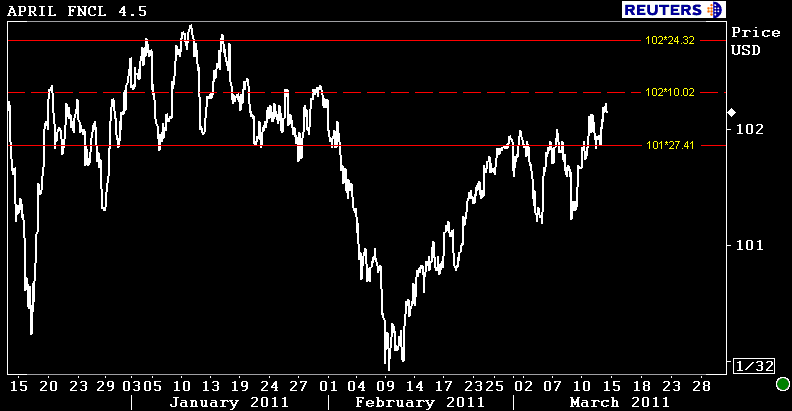

The FNCL 4.5 is currently +9/32 at 102-05 after trading up to 102-08 earlier in the session. The last time FNCL 4.5s touched 102-08, it was January 31st.

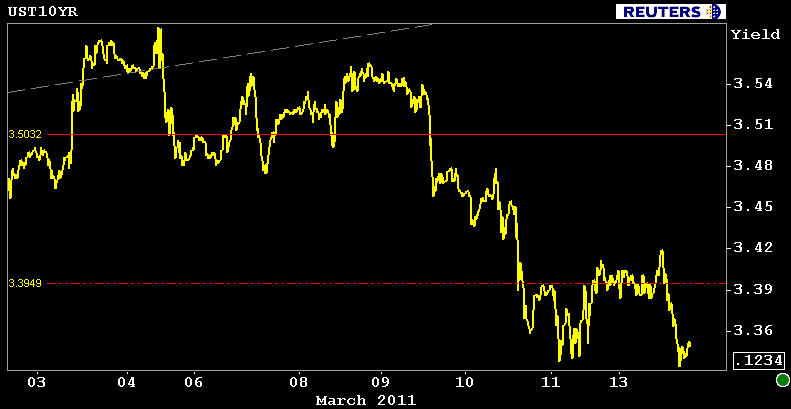

The benchmark 10-year TSY note traded mostly sideways last night before it dipped to lower levels in the 7AM hour. The move to Friday's low yield print was direct, 10s have yet to trade through that resistance today. Yields are currently backing up a bit....

As you might have already heard, Japan's main stock index, the NIKKEI, fell 633 points or 6.18% when it opened last night for the first time since the earthquake/tsunami leveled the coastline and knocked out power to around 330,000 people. The NIKKEI is charted below to illustrate the speed and size of the sell-off. The stopping point was technically driven as traders pushed the index directly to the 62% fibonacci retracement of the 2010 low before moving on with more pressing issues...like finding family and friends. I can't imagine trying to manage a position in that sort of environment. Ugh.

Notice volume was VERY high into the down trade...

WATCH OUT FOR PROFIT TAKING IN THE BOND MARKET.