Coming off a slow week of scheduled data the markets are ready for activity to pick up in the day's ahead. Monday and Friday each boast just one Federal Reserve speech, but the three days in between are full of new data.

“Economic indicators next week should continue in the positive vein, as retail sales are projected to power up by about 0.6% in January, and industrial production is expected to rack up another fairly solid positive gain,” said economists at IHS Global Insight. “The housing market, however, is expected to report considerable weakness early in 2011, partly as a result of poor weather conditions.”

The market focus this morning could be on President Obama’s annual budget proposal, which NPR calls “a $3.73 trillion spending blueprint that pledges $1.1 trillion in deficit savings over the next decade through spending cuts and tax increases.”

The budget projects a current year deficit of $1.65 trillion, the highest ever.

“That reflects a sizable tax-cut agreement reached with Republicans in December,” NPR reports. “For 2012, the administration sees the imbalance declining to $1.1 trillion, giving the country a record four straight years of $1 trillion-plus deficits.”

The 10-year Treasury note went out Friday yielding 3.65%. It has since strengthened and now yields 3.63%. The FNCL 4.5 MBS coupon is -2/32 at 100-16. Equity futures are pointing modestly downwards Monday morning as President Obama prepares to reveal his 2011 budget proposal. S&P 500 futures are down 1.25 points to 1,326.00 and Dow futures are trading 3 points lower at 12,238. So far this year the benchmark S&P has gained 5.69%

Commodity prices are mixed. Light crude oil is down 0.40% at 85.24 0.08% per barrel, while gold prices are up 0.29% at $1,360.00 per ounce.

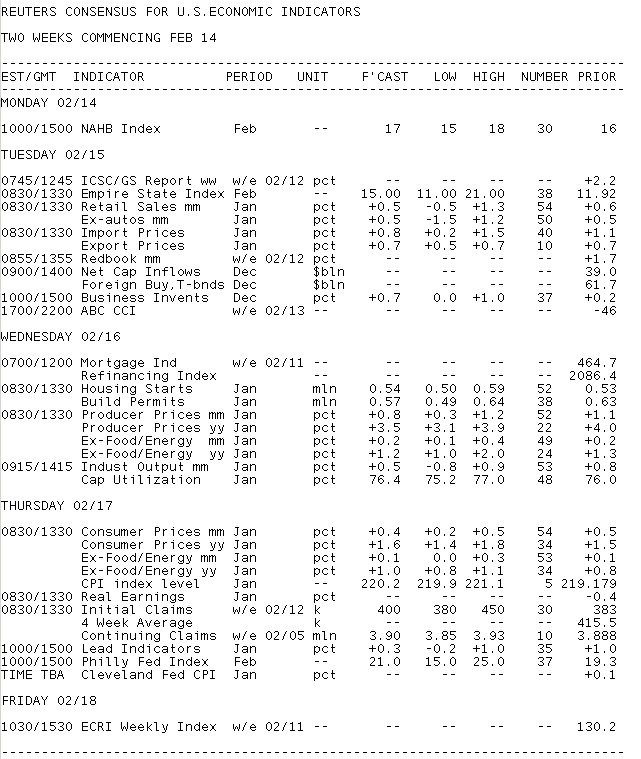

Key Events This Week:

Monday:

10:00 ― William Dudley, president of the New York Fed, speaks at the quarterly regional economic press briefing on household debt and current trends, in New York.

10:15 ― The Fed will buy an estimated $1-2 billion of TIPS dated 4/15/2013 to 2/15/2040

President Obama releases his 2012 budget.

Tuesday:

8:30 ― Retail Sales are anticipated to kick off 2011 with a 0.5% increase, following a 0.6% gain in December and 0.8% uptick in November. The survey has been showing sales growth for the last six months, including the best holiday shopping period in years. Economists are anticipating the growth to be broad: excluding autos, retail sales should rise 0.5% for the second straight month.

“Consumers have been spending more due to relatively good news on the employment front, pent-up demand, low prices, and a significant decline in the non-mortgage debt to disposable income ratio,” said economists at IHS Global Insight. “However, consumers are not throwing caution to the wind because of gasoline and food prices, a high and persistent unemployment rate, and an extremely depressed housing market.”

Economists at BTMU pointed out that fourth-quarter retail sales advanced 4.4%, the fastest pace since early 2006, and that January should confirm the momentum continues into 2011.

“In general, the retail sector continues to battle a high unemployment rate, but consumer confidence is improving and recent government stimulus should help boost spending in 2011,” they wrote.

8:30 ― The Empire Fed Manufacturing Survey, the first regional index to be released for the sector each month, is forecast at +15 in February, compared to +11.9 in January. The threshold for growth is zero. Predictions range from 11 to 20, indicating stability in the sector after a low +2 reading was seen in November ― called a bizarre aberration by one economist. Forward-looking components in the January index provide some optimism for this month, including a +12.4 score for new orders and +25.4 for shipments

“Momentum in the manufacturing sector looks solid, with all the major survey indexes reporting healthy results in recent months,” said economists at Nomura Global Economics. “We see little reason for this trend to break in February ― and at 11.9, the Empire State index is not particularly elevated compared to its cyclical highs. Watch the ‘prices received’ index in the survey for evidence of pass-through from higher commodity prices onto finished goods.”

10:00 ― Business Inventories are expected to end 2010 with a 0.7% climb, versus a modest 0.2% increase the month before. The November index was inconsistent, with manufacturing inventories advancing 0.8%, wholesale inventories slipping 0.2%, and retail inventories unchanged. Recent expansion in factory orders and wholesale inventories point to more consistency of growth for December.

10:00 ― The Housing Market Index, an index of Homebuilder Sentiment Index compiled by the National Association of Home Builders, continues to stagnate well below the 50 level which indicates general optimism. The January index remained at just 16, failing to live up to modest expectations. Worse, the 'traffic of prospective buyers' component was at 12. Continued cold weather is expected to keep the index low in February, though a consensus forecast was not available at the time of writing.

“The index of homebuilder sentiment remains low, and at some point could rise quickly,” said economists at Nomura Global Economics. “But for the time being we believe the index will remain stuck at low levels. Recent news on home construction, construction employment, home sales have all been quite poor. We therefore see little reason for greater optimism among builders.”

10:00 ― Sandra Pianalto, president of the Cleveland Fed, speaks on regional and national economic conditions to Women's Boards of Summa Health Systme in Akron, Ohio.

10:15 ― The Fed will buy an estimated $5-7 billion in Treasuries maturing between 2/28/2015 to 8/15/2016

Wednesday:

8:30 ― Look for Housing Starts to improve in January, economists say. The consensus is for the annualized pace of new construction to rise to 540k from 529k, a decent advance after the index shed 4.3% in December. Cold weather hurt the December index and will likely play a role in January too.

Beyond the headline, the two main components need to be looked at closely given their volatility: in the last index, single-family starts fell 9.0% while multi-family starts jumped 17.9%. Housing Permits, which offer a forward-looking assessment, were similarly inconsistent ― single-family permits increased 5.5% and multi-family permits jumped 53.5%.

In contrast to the consensus, economists at BMO believe snowstorms will pull the index down for a second straight month, to 520,000 units.

“This would be the third lowest level on record and less than half the rate of long-run household formation,” they wrote. “Thankfully, residential construction accounts for a record-low 2.2% of GDP, so the decline will have little impact on Q1 growth, which we currently peg at 3.8% annualized.”

Economists at IHS Global Insight are more pessimistic and expect housing starts to fall to 499k.

“Permits jumped 15% in December, but pending building code changes in three states ― New York, Pennsylvania and New Jersey ― were responsible for the surge,” they wrote. “A payback should follow in January, when we expect permits to dive 17%.”

8:30 ― Energy prices continue to cause high inflation in the monthly Producer Price Index. The last two indexes yielded jumps of 1.1% (Dec) and 0.8% (Nov), while January prices are anticipated to grow 0.7%. Energy prices rushed forward by 3.7% and 2.1% in the prior two indexes. Core inflation, which excludes volatile energy and food prices, continues to be rather tame: the January index is expected to be 0.2%, the same at in December and lower than November’s 0.3% uptick.

“Energy ― up over 3% again ― will be the bane of the producer price index for the fourth consecutive month, and push overall prices up by 0.9% in January,” predicted economists at IHS Global Insight. “We expect to see some pass-through of higher materials costs pushing up core prices by 0.3%, rather than the 0.2% increase in December. Food prices should also rise, though the steep increases in commodities like wheat, corn and soybeans are only gradually filtering through to the finished goods PPI.”

9:15 ― Industrial Production ended 2010 with a bang: the index rose 0.8% in December, the highest since July, and annual output was +5.7% ― the strongest performance in over a decade. January is anticipated to be less dramatic but still positive. Economists look for a 0.5% increase, with predictions ranging from -0.8% to +0.7%. Utility output played a big role in the December advance as it jumped 4.3%. It’s unlikely to climb as much in January, but storms across the county should keep utility usage positive.

“Rising output of business machinery and automobiles should provide support, while utilities output was probably stoked by the coldest January in 23 years,” said economists at BMO Capital Markets. “Rising production could lift the capacity utilization rate to 76.6%, the highest since August 2008. However, that’s still less than the presumed inflation-safe norm of 81%, suggesting plenty of inflation-dampening slack remains in the industrial space.”

10:15 ― The Fed will buy an estimated $1.5 to 2.5 billion in Treasuries maturing between 5/15/2021 to 11/27/2027

2:00 ― FOMC Minutes from the first meeting in 2011 could of interest to Fed-watchers because the committee lineup changed, but markets were content to ignore the report when it came out and will likely pay little attention to details released here. The statement from the meeting contained few changes save for an economic upgrade, and not one of the voters dissented.

Economists at Nomura said the minutes will look stale next to Ben Bernanke’s congressional speech on Feb 9. Still, they said two items could be of importance.

“First, they will contain updates of the Fed's forecasts,” they wrote. “Forecasts for the unemployment rate may still be high because they will have incorporated only the 0.4 percentage point decline to 9.4% in December. However, we expect that the central tendency for 2011 GDP growth will move up 0.25-0.50pp.

“Second, the minutes will likely contain detailed discussion of communication options, such as inflation targeting and post-meeting press conferences. We suspect the committee may be moving forward on the latter, but other communication changes will remain under discussion for now.”

Thursday:

8:30 ― The Consumer Price Index is anticipated to move upwards by 0.3% in January, averaging out from the 0.5% gain in December and the 0.1% increase in November. A 9.5% surge in energy prices was the culprit for December’s gain, but even so the yearly rate was just 1.5%, well below the Fed’s preferred 2% rate. Core prices, which exclude volatile energy and food components, continue to be moderate. The core index is forecast at a modest 0.1% in January, the same as in December, which followed three months of no gains.

“Aggressive discounting should keep core consumer prices unchanged in the month, though the yearly rate likely edged higher to 0.9%,” said economists at BMO. “While up from October’s all-time low of 0.6%, the core rate is still about one percentage-point below the Fed’s long-run ‘target’. Meantime, rising gasoline and food costs could kick the headline CPI rate up a couple of tenths to 1.7%.”

8:30 ― The closely-watched Initial Jobless Claims survey has been too volatile to be of much use recently. For the week ending Feb 12, economists look for 410k new claims, 27k higher than in the previous week and broadly in line with the 415k four-week average. The last week’s headline number was surprisingly low as claims fell 36k in the week to the lowest level since early July 2008. The Labor Department indicated the cold weather and seasonal adjustment issues were playing a role in the recent figures.

To avoid the week to week volatility, economists at BTMU took a look at much broader trends.

“In 2009 claims averaged 572,000 compared to 418,000 in 2008, which was the largest annual jump in claims since 1974, but fell back to average 457,000

in 2010,” they wrote. “Thus far in 2011 claims are averaging 405,000.”

10:00 ― Ben Bernanke, chairman of the Federal Reserve, testifies before Senate Banking Committee on Dodd-Frank reforms, alongside SEC Chair Mary Schapiro, FDIC Chair Sheila Bair, and CFTC Chair Gary Gensler, in Washington.

10:00 ― Leading Economic Indicators, a composite index designed to measure turning points in the economy, is expected to rise for the seventh straight month in January. The bad news: the index is rise 0.2%, versus a 1% gain in December a 1.1% boost a month before. Also, economists from BMO point out that the year-to-year comparisons have been shrinking in recent months, and the impressive 1% gain in December was largely attributable to a single component (building permits).

“The biggest drag on the index comes from a steep decline in building permits,” said economists from Nomura Global Economics, who anticipate a 0.1% gain overall and a big reversal among building permits. “The decline in the average manufacturing workweek and the rise in the moving average of initial jobless claims are other negative contributors to the index.”

10:00 ― The Philadelphia Fed Index is expected to grow at a steady rate for the third consecutive month in February. Economists look for a score of 22, up from 19.3 in January and 20.8 in December. The three months of growth follow a slight increase of 1.2 in October and a contraction in late summer. New orders, an indicator of future activity, more than doubled in January to 23.6 ― the strongest reading since September 2004. Shipments, an indicator of current activity, also more than doubled to 13.4.

“Like the Empire State index, we expect the Philly Fed report to show a modest gain in overall activity,” said economists at Nomura Global Economics. “We will be closely watching the ‘prices received' index for evidence of commodity price pass-through.”

10:15 ― The Fed will buy an estimated $6-8 billion in Treasuries maturing between 5/15/2018 to 2/15/2021

11:30 ― Dennis Lockhart, president of the Atlanta Fed, asks questions of Irish Ambassador Michael Collins at a World Affairs Council discussion in Atlanta.

1:10 ― Richard Fisher, president of the Dallas Fed, speaks on the economy and the Fed at a community forum in Houston.

1:20 ― Charles Evans, president of the Chicago Fed, speaks on the economic outlook to the Rockford Chamber of Commerce in Rockford, Ill.

Friday:

8:00 ― Ben Bernanke, chairman of the Federal Reserve, speaks on global imbalances and financial stability at the Banque de France Financial Stability Review, in Paris.

10:15 ― The Fed will buy an estimated $5-7 billion in Treasuries maturing between 8/31/2016 to 2/15/2018