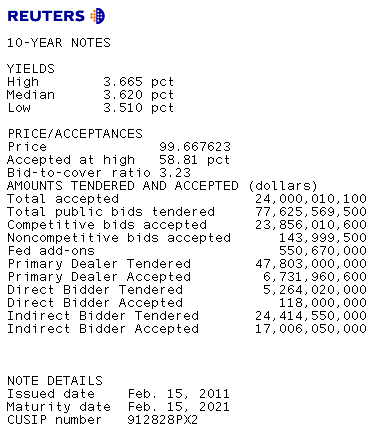

Treasury just sold $24 billion 10 year notes. Hello Bargain Buyers....

Demand was extremely strong for this newly issued 3.625% coupon. The bid to cover ratio was 3.23 bids submitted for every 1 accepted by Treasury. Compare that to a five auction average of 3.04 and a 10-auction average of 3.13. Beyond that, any bid to cover over 3x should be considered "strong" anway. In terms of the price investors were willing to pay, participants bid through screens to get their hands on this issue. The "high yield" was 3.665% vs. the 1pm "When Issued" yield of 3.709%. That is a difference of 4.4bps! Hello bargain buying! This is why we were encouraged by pre-auction short covering...

So we know demand was strong, but the real story lies in the breakdown of that demand.

First and foremost, indirect bidders were awarded a MASSIVE 71.3% of the competitive bid or $17.0 billion of the $23.9 billion they could have taken down. Call Guinness because I believe that is a new record. Although the "indirect" category includes hedge funds, the metric is mainly viewed as a barometer for overseas demand, including foreign Central Banks. These are your bargain buyers people. All I can say is WOW. What a turnout from indirect bidders. They were aggressive too! Taking home 70% of the $24.4 billion they tendered.

This is a story of two extremes though. With indirect accounts foaming at the mouth to get their hands on new issue 10-year paper, demand had to suffer elsewhere. That's where we call out Direct bidders. I honestly had to triple check the data because I thought it was wrong. Direct bidders were awarded a measly 0.5% of the issue. Not even 1%. This is a record low. It wasn't like directs were not aggressive in their bidding, they just didn't bid! Compare a $5.2billion tender today vs. an $10.9 billion tender last month and a $8.7 billion tender in the December re-opening. Directs were just not interested and indirects were more than happy to accomodate their apathy (OK so indirects may have gotten a little more inventory then they bargained for).

Market Reaction...

Benchmark 10s are rallying, the yield curve is bull flattening and while production MBS prices have fallen behind, some lenders are repricing for the better. The FNCL 4.5 is just off intraday highs.

We need to share some sobering news though, this post-auction rally is encouraging but was still a factor of IMMEDIATE SHORT COVERING.

Remember a short seller wants prices to fall and yields to rise. This is not a sign of outright optimism for lower rates but it definitely tells us there is bargain buyer demand for longer-dated Treasuries when prices fall and the yield curve bear steepens. It tells us the short base in the Treasury market is defensive of profits once 10s break 3.70% support.

We need to see some follow through from real$ accounts like banks, insurance companies, and loan servicers if this rally is to extend and reverse bearish bond market technicals. A steep yield curve and well-grounded Fed Funds Rate should attract real money bond investors but we're still teetering on a snowball event and technicals still favor higher yields. We gotta break the back of fast$ short sellers. MORE SHORT COVERING PLEASE!!!! It will only fuel a recovery bounce. Stay defensive but be encouraged by the turnout at today's 10-year note refunding. SAY NO TO SNOWBALLING. SAY NO TO ANOTHER DURATION SHEDDING EVENT!

We're outlining resistance levels and inflection points on the MBSonMND Dashboard. Discussion activity is buzzing....