Turmoil in Egypt and the broader middle-east continues to weigh on investors. As riots broke out late last week, U.S. equity markets saw their steepest single-day declines in months. This led to a flight to safety in the government bond market and helped mortgage rates improve a few basis points. The flight to safety was however not enough to break the recent MBS trading range.

The release of the Employment Situation Report is the main event on the economic calendar in the week ahead. However continued civil unrest in Egypt is expected to stir up commotion in the marketplace and potentially dictate the direction of mortgage in advance of jobs data on Friday morning. After ending an eight week rally last Friday, bond investors will be keeping a close eye on the sentiment of stocks and shifts in foreign exchange rates for leadership.

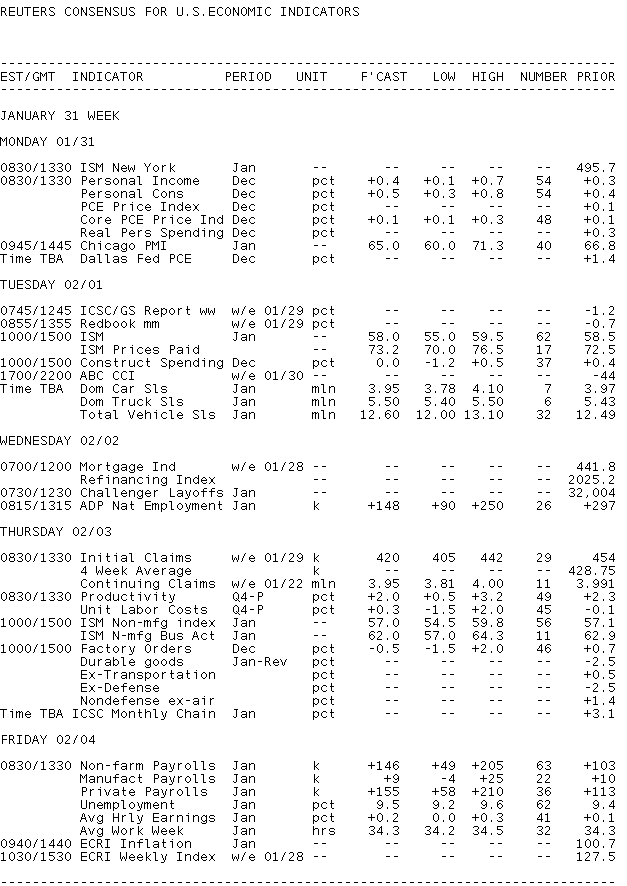

Key Events This Week:

Monday:

8:30 ― The BEA’s Personal Income & Outlays report is anticipated to show income and spending levels rising in December, while core prices remain virtually stagnant. Economists polled by Reuters look for a 0.4% rise in income, a slightly faster pace than the 0.3% gain in November. Spending ― which was the biggest contributor to Q4 GDP growth of 3.2% ― is forecast to rise 0.5% on top of November’s 0.4% gain. And core inflation ― a measure that strips out volatile food and energy components ― is supposed to repeat a 0.1% uptick.

“Note that about a third ― or perhaps even half ― of the total increase in real December spending will likely be in the gas and electric utility component, which is driven by variations in the weather in the short term,” said Ian Shepherdson from High Frequency Economics. “This surge will reverse in due court, perhaps as soon as January, adding support to our view that first quarter consumption will be markedly slower than in the fourth.”

Economists at BMO note that 0.1% inflation would leave the annual rate unchanged at 0.8%, “which is still just half the bottom of the FOMC’s projected 1.6%-to-2.0% longer-term range and the key reason what the Fed is still in easing mode despite signs of firmer economic activity.”

9:45 ― The Chicago Business Barometer has outperformed consensus forecasts in each of the last three months. In December, the index of midwestern services and manufacturing jumped six points to its strongest growth rate in more than 21 years. The index was at 68.6 ― nearly 19 points above the level indicating growth. To start 2011, economists predict some moderation to 65. The best forward-looking component, new orders, boasted a 73.6 figure in December, suggesting the consensus might be wrong once again.

“We look for a modest decline in the Chicago PMI in January as payback from a large increase in December,” said economists at Nomura Global Economics. “Although our forecast for January is 62.0 ― 4.8 points down from the post-crisis highest reading of 66.8 in the previous month ― this level is still relatively high from the historical norms. The index of prices paid is also expected to slide to 72.0 from 78.0 previously.”

12:00 ― Dennis Lockhart, president of the Atlanta Fed, holds discussion with Miami Dade College students.

Tuesday:

10:00 ― The ISM Manufacturing Index, the nation’s key report on manufacturing, is expected to move up 0.5 points from the December score of 57.0 ― the highest level in seven months. Forecasts are in a relatively tight range of 56.5 to 59.5, with any score above 50 indicating growth in the sector. The employment component will be key in light of two items: a) in December it dropped to nearly two points to 55.7; and b) everyone is looking ahead to Friday’s nonfarm payrolls report.

“[This index] increased in the last 6 consecutive months and has been higher than 50 since August 2009, indicating that manufacturing activity is expanding compared to the previous month,” said economists at BBVA. “Regional Fed’s manufacturing activity indices confirm that the manufacturing activity in the U.S. continues expanding.”

More broadly, economists at Deutsche Bank added: “We remain positive on the manufacturing outlook in 2011 as rising auto demand and tax incentives for capital expenditures provide significant tailwinds for the sector.”

10:00 ― Construction Spending is forecast to rise a measly 0.2% in December, versus a 0.4% increase in November. Forecasts are deeply divided, with some economists looking for a drop as big as -0.9%. The potential culprit was an unusually cold December, as suggested by the drop in residential construction of new homes. A negative print would break a three-month trend.

“Construction spending increased 0.8% on average in the last three months,” noted economists at BBVA. “We expect that construction spending increased slightly due to relative improvement in real estate industry. Since the construction spending data is released with a long lag, the market reaction could be limited, yet it would help us understand current conditions in both the residential and nonresidential construction industry.”

Wednesday:

7:00 ― The MBA Mortgage Applications index is failing to inspire much optimism in the housing market. The weekly index fell nearly 13% in the week ending Jan 21, as refinances fell more than 15% to the lowest level in a full year. Purchases also fell nearly 9%.

“The past week's negative growth meant the end to three weeks of positive numbers,” said economists at Nomura Global Economics. “The 30-year fixed rate is hanging near 4.8% after reaching lows of 4.2% just a few months ago. We suggest this explains much of the decline in refinancing activity, which declined 15.3% week-over-week. We continue to emphasize the high volatility and low reliability of this weekly indicator.”

8:15 ― The ADP Private Employment Survey is anticipated to show that 150k jobs were created in January. Anything too far from the consensus won’t be taken too seriously after last month’s debacle, in which ADP showed 297k new jobs ― about triple the consensus figure. That motivated the market to raise their expectations for the official government figures released two days later, which turned out to be much lower than original forecasts.

“Because of the particular way in which the ADP data are constructed, we believe it is appropriate to ignore the December report, and assume that a more typical gap between the ADP and BLS measures returned in January,” said economists at Nomura Global Economics. “Specifically, before December, the six-month average gap between the growth rates in private payrolls measured by the ADP and BLS reports was about 70,000. Our forecast for a 160,000 increase in the official measure of private employment should thus be consistent with an ADP result of about 90,000.”

Thursday:

8:30 ― The market will be closely watching the Jobless Claims report for the week ending Jan 29. The previous week was a major disappointment as initial claims grew 51k to 454k ― the highest since late October. That raised the four-week average to 428,750.

“Holidays and storms are providing distortions to the data that is even larger than usual,” said economists at BTMU. “I suspect that the latest week’s jump in claims is reflecting the aftermath of the snowstorm in the South that resulted in a huge backlog of claims.”

For the final week of January, the consensus looks for 425k new claims. Forecasts are especially wide, ranging from 354k to 434k.

8:30 ― The fourth-quarter Productivity & Costs report, unlikely to receive much attention given that Q4 GDP hit the wires last week, is expected to be unchanged from the previous quarter. Nonfarm Productivity is seen as +2.3%, while unit labor costs are to forecast at -0.1%.

“Productivity growth has cooled in recent quarters after a brief boom in 2009,” said economists at Nomura Global Economics. “However, the current growth rate still suggests output growth would have to accelerate further to lower the unemployment rate quickly.”

10:00 ― ISM Non-Manufacturing Index, which looks at the services, financial, and construction sectors nationwide, is expected to slip a marginal 0.1 points to 57.0 in January, representing strong growth to start the New Year. One reason for the strong predictions is the new orders component in December, which jumped more than 5 points to 63.0, the highest level since the recession began. The December index also marked the first time since June 2009 that this index outperformed its manufacturing counterpart.

“Freight activity has picked up in recent weeks, and financial market dynamics generally have been positive,” noted economists at IHS Global Insight. “However, employment market conditions did not improve much in January, possibly as a result of negative weather impacts on construction activity. Orders are expected to hold about the same pace. On net, therefore, not much change in the index.”

12:30 ― Ben Bernanke, chairman of the Federal Reserve, speaks to reporters at the National Press Club.

8:00 ― Narayana Kocherlakota, president of the Minneapolis Fed, speaks in St. Paul, Minn.

Friday:

8:30 ― Expectations are pretty humble for the January Nonfarm Payrolls report. The median forecast is for 150k new jobs, beating the disappointing 103k and 71k figures for December and November, but well below the 210k jobs created in October. The gain isn’t even big enough to reduce the Unemployment Rate, which is seen increasing one-tenth to 9.5%.

“There are presently no compelling inputs suggesting we should be braced for a strong payroll gain,” said economists at RBC Capital Markets. “Claims have been erratic […] job indexes from the various confidence reports ― such as the one found in the RBC Consumer Outlook Index ― advanced modestly in January. This appears like a recipe for a payroll gain that’s fairly close to the recent average.”

Some economists have said cold weather could throw off the payrolls report by 60k to 70k.

“The main wild card this month is the weather, which was severe enough in some southern states to disrupt the registration of unemployment insurance claims, and may have held down the payroll count, too,” said economists at IHS Global Insight. “As for the unemployment rate, the sharp drop in December to 9.4% from 9.8% looks odd, and we expect a retracement to 9.6% this month.”