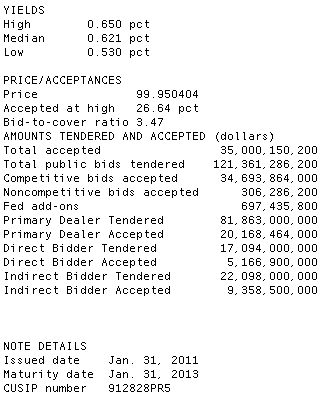

Treasury just sold $35 billion 2 year notes maturing on Jan. 31, 2013.

Dealers had to bite the bullet on this one...

For the second 2-year note auction. indirect bidders were notably absent, taking home a well-below average 26.9% of the competitive bid and 42% of what they bid on. Compare that to 22.6% in December, 38.3% in November, 39.9% in October, and 39.0% in September.

Hmm...

I guess with inflationary threats growing in overseas markets it makes sense that overseas investors might be looking for larger return (yield) as their currency appreciates against ours in the near term. Their local inflation premium isn't baked into our 2-year benchmark yields....creating less incentive to arbitrage with the short end of our yield curve. ??? Maybe I'm reaching but it makes sense....

The lack of indirect interest forced primary dealers to carry a larger load. The street picked $20.1bn or 58.1% of the issue. That is well above average. Also note dealer tenders fell by almost $4bn and their hit rate spiked...force feeding! Blame the indirects...blame overseas inflation expetations.

Direct participation was average.

The high yield was 0.65% which was slightly below the 1pm "When Issued" yield if 0.655%. Basically on the screws.

The bid to cover ratio was close to the recent average at 3.47%....which is still high.

Plain and Simple: Not a terrible auction. Not great either. Average is a fair evaluation.

Benchmarks are bull flattening (rallying) and MBS are following the leader. On the heels of short covering the 10 year note has backed down from 3.40% all the way to 3.33%. The FNCL 4.5 is at four session price highs but running into resistance. It looks like we're seeing a modest bid in production MBS coupons. Yield spreads are still wider on the downtrade but the current coupon is shortening up a bit vs. the curve and the bid/ask spread has been bouncing around. Choppy flows....

Plain and Simple: REPRICES FOR THE BETTER ARE LIKELY