The week ahead is busy to say the least. President Obama will give the State of the Union Address on Tuesday night. The Federal Reserve will hold a two day FOMC meeting to discuss monetary policy and share an updated outlook on Wednesday. We'll get a trio of housing reports as well as a trifecta of Treasury coupon auctions totaling $99 billion. Scattered in between, the New York Fed will conduct four QEII open market Treasury operations. And rounding out the week ahead, the Q4 earnings season continues with key reports from 3M, Procter & Gamble, Boeing, Caterpillar, Ford, Honeywell, and Johnson & Johnson.

So needless to say there is a plethora of news and events that might just serve to provide some directional guidance for the MBS market and mortgage rates, which have been stuck in a well-defined yet wide range in 2011.

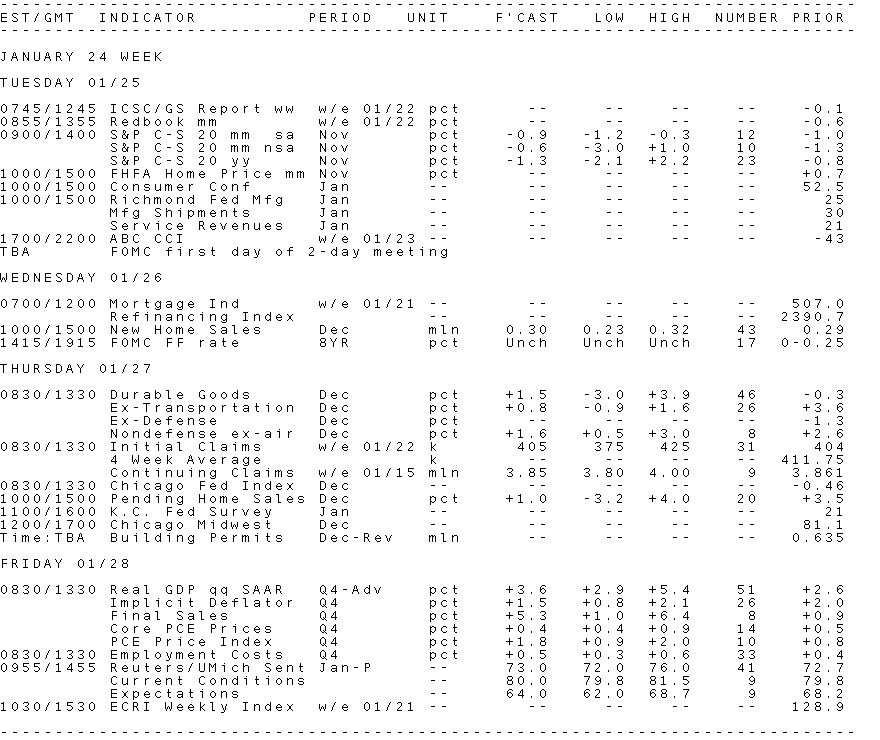

Key Events This Week:

Monday:

10:15 — The Fed will purchase an estimated $7-9 billion in Treasuries maturing between 7/31/2016 and 12/31/2017.

Tuesday:

9:00 — The S&P Case-Shiller Home Price Index is expected to see prices fall for the second straight month in November. The back to back declines follow eight months of rising prices. Economists polled by Reuters look for the seasonally-adjusted index to drop 0.9% in the month, just less than the 1% slide a month before. Annually, prices should be down just 1.3%, suggesting a fair bit of stability considering the glut of houses still on the market.

“It is not the indication of another downward trend because existing housing demand improved significantly in the last quarter of the year,” said economists at BBVA. “Home prices are currently at favorable levels for consumers and attractive affordability ratios will play a role in attracting demand and reducing inventories of existing homes.”

10:00 — Consumer Confidence is expected to tick up to 54.7 in January from 52.5 in the final month of 2010. Some economists doubt the index will increase at all, as unemployment remains high and prices for food and gasoline have been rising in recent weeks. However, the consensus for the Conference Board index to move up along with stock prices and general economic growth.

“With stock prices rising and initial jobless claims falling, we think it will start to pick up this month, although gains will be limited as long as joblessness remains very high,” said economists at Nomura, adding that the current conditions component is closely correlated with the unemployment rate.

10:15 — The Fed will purchase an estimated $6-8 billion in Treasuries maturing between 1/31/2015 and 6/30/2016.

1:00 — Treasury will auction $35 billion 2-year notes maturing on January 31, 2011.

9:00 — President Barack Obama will give the State of the Union Address. The President will talk about "what America needs to do to create jobs today, make America more competitive tomorrow, and win the future for our children and our country".

Wednesday:

7:00 — The latest MBA Mortgage Applications index showed the level of refinances at a six-week high, but the more important index looking at purchases continued to fall. The level of loan applications for purchases is 16% lower than this time last year, and mortgage rates have been on the rise. Some economists have been saying the year of housing recovery will be 2012.

“The past three weeks of positive growth in this indicator followed five consecutive weeks of declines,” noted analysts at Nomura Global Economics. “We discourage relying heavily on this volatile index as a signal of housing market health. We await a sustained trend in mortgage purchase applications before using it to confirm housing's recovery or continued slump.”

10:00 — New Home Sales are expected to inch forward from levels recently described as “miserable” and “at rock bottom” in December. Economists polled by Reuters expect the index to report the annualized pace of sales to be 300k, just up from 290k in November. That’s not much higher than August’s all-time low of 274k (with data going back to 1963). In November, the index rose 5.5%.

“With a slowly improving job market, December sales should see a modest bounce from November's fifth lowest reading on record,” said economists at IHS Global Insight., who project a modest increase owing to an improving job market and growing economy.

“December's improvement in single-family housing permits ― normally a good leading indicator for new home sales ― might seem to point to a much stronger outcome,” they added. “But December's rise in permits was distorted by pending building code changes in New York, Pennsylvania and California.”

2:15 — Not much is being forecast for the FOMC Meeting Announcement, despite this being the first meeting of 2011 with the Fed’s new lineup of voters.

“Despite the shift in the composition of the FOMC to a slightly more hawkish Fed, the course for monetary policy is unlikely to be altered in anyway meaningful way this year,” said economists at TD Securities.

The new voting members are Chicago Fed President Charles Evans, Minneapolis Fed President Narayana Kocherlakota, Dallas Fed President Richard Fisher and Philadelphia Fed President Charles Plosser.

The most significant departure from the lineup is Kansas City Fed President Thomas Hoenig, who had dissented at every FOMC decision in 2010.

Speaking of the direction of monetary policy, analysts at IHS Global Insight said now isn’t the time to make any changes to the Fed’s program of quantitative easing, which remains in its early stages.

“While the economy is improving, the rates of growth of output, prices and employment are still far below the ‘thresholds’ that would precipitate a policy change from the Fed,” said analysts at IHS Global Insight. “We expect the new FOMC members to generally support Bernanke's approach, with a possible dissent from Dallas Fed Chief Fisher, in which case he would carry the baton passed on by Kansas City Fed Chief Hoenig, who rotated off the FOMC at the end of 2010.”

1:00 — Treasury will auction $35 billion 5-year notes maturing on January 31, 2016.

Thursday:

8:30 — Durable Goods are anticipated to jump 1.5% in December, following a sharp rebound among core goods a month earlier. The November headline fell 1.3%, but the decline was due almost solely to commercial aircraft orders. For December, the core index ― non-defense goods excluding aircrafts ― is expected to rise 1.6%.

“Headline orders will be pulled down by another drop in aircraft orders, with sluggish gross new orders at Boeing combining with some cancellations to leave net new orders for complete aircraft near zero,” said economists at IHS Global Insight.

They added that core goods should see another uptick, and defense orders could provide a little lift, but the latter will be faint next to the bounce seen in November when it recovered from an 18-month low.

8:30 — The average for Initial Jobless Claims over the past three weeks had been 419k, a higher level than December’s 414k average but lower than November’s 432k. The most recent report showed claims at just 404k, setting up some forecasters to predict as few as 375k claims in the report. The consensus view is more temperate at 405k.

“The substantial seasonal adjustments required by atypical holiday employment diminish the reliability of this indicator,” said economists at Nomura. “We expect claims to come in near the 4-week moving average ― a more reliable statistic, in the neighborhood of 411k.”

10:00 — Look for a 1% increase in the Pending Home Sales Index. While the index jumped 3.5% in November, poor weather in December is leading economists to view any increase as marginal at best.

Moreover, economists at Deutsche Bank add a warning that a ‘double-dip’ is still a possibility for the housing market.

But, they added, “the outlook on housing will depend on the trajectory of the labor market [and] if our forecast for an 8.8% unemployment rate by the end of next year proves correct, we are likely to see the worst of the housing market collapse behind us.”

10:15 — The Fed will purchase an estimated $4-6 billion in Treasuries maturing between 7/31/2012 and 7/15/2013

1:00 — Treasury will auction $29 billion 7-year notes maturing on January 31, 2018.

Friday:

8:30 — The advance estimate for fourth-quarter GDP is expected to come in at +3.6%, according to economists polled by Reuters. Estimates range from +2.9% to +5.4%, indicating the final three months of 2010 were clearly stronger than the prior quarter’s +2.6% rate. Leading the way is retail sales, which may have jumped 4% in the quarter, and exports.

“We believe that 2010 ended with a +3.8% bang,” said economists at BTMU, adding that full-year GDP likely grew 2.9%. “That’s really a paltry rebound when you compare it to such a sharp drop in 2009 (-2.6%), but it was above the +2.5% rate considered to be the minimum growth needed to hold the unemployment rate steady. Indeed, it was enough growth to bring the unemployment rate down to 9.4% at the end of 2010 from 9.9% at the end of 2009.”

Economists at TD added that the economy is “beginning to pick-up significant tailwind” on account of loose fiscal and monetary policies.

“Strong consumer spending, which accounts for close to 70% of overall U.S. economic activity, should be the key driver for the burst in activity, with personal consumption expenditures expected to grow in excess of 3.5% Q/Q ― its fastest pace since late 2006,” they said.

9:55 — The preliminary Consumer Sentiment survey from Reuters / U of Michigan fell 1.8 points to 72.7, marking the first fall in several months. The slide surprised economists who believed a rising stock market would translate into higher sentiment. Instead, consumers were focused on higher prices and continued joblessness. In this final reading, the consensus forecast is set at 73.0, a bit up from two weeks ago but still below December’s 74.5 score.

Economists at IHS Global Insight are more pessimistic than the consensus, forecasting a drop to 71.8.

“The current and expectations indices are both expected to fall, with the current situation index taking the bigger hit,” they predicted. “Consumer sentiment is being negatively impacted by high gasoline and food prices, although these are not severe enough to derail the increased consumer spending momentum.”

10:15 — The Fed will purchase an estimated $7-9 billion in Treasuries maturing between 2/15/2018 and 11/15/2020.