"After failing to confirm a break of the broader 3.27 to 3.56% range, benchmark 10 year TSY yields shot 13bps higher in an aggressive manner this morning, releasing stored energy in an originator unfriendly direction. This has led production MBS coupon prices sharply lower in just a matter of minutes, which [led] to reprices for the worse."

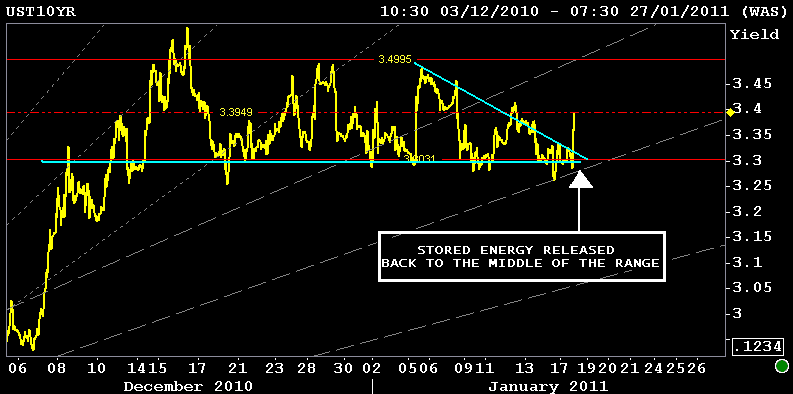

That paragraph is from this morning's MBS commentary, with the small exception being that "may lead" was changed to past tense as we did indeed see reprices for the worse. But if lenders didn't get sheets out before the initial high-volume selling this morning, they generally did not reprice as bonds held firm after a strong support bounce near the midpoint of the range. That midpoint was well illustrated even before the bounce was seen in AQ's morning chart:

Although I'd be more inclined to weight recent technicals in favor of the higher volume January action, even the charts that look back to mid December support the technical nature of today's seemingly spiky movement.

In the chart below we can see treasury yields touched or came close to touching both sides of the those trendlines today. So naturally, if the market awaits further confirmation before challenging lower yield resistance, where else was there to go this morning? (remember that the rightmost candlestick encompasses the entire day's yield movement.)

Additionally, MBS entered a narrow and moderately improving range into the afternoon, prompting lenders who had either repriced or who were otherwise out of the gate with bad pricing to reprice for the better this afternoon, and they are still trickling in.

As has been the case for weeks, the larger choppier movements are being seen as prices and yields move in the central parts of the range whereas they move in narrow, sideways paths when at or near the outer limits of the range. This is clearly illustrated in today's MBS chart.

AQ adds..."MBS extended vs. the curve today and went at session wides."

The conclusion is the same as it was on Friday night, the range is the range until it's not.

If you ascribed to that principle, you saw benchmark yields as good as they'd been in quite some time and despite our DESIRES to see the range broken favorably, were nonetheless given a big hint to sell that dip and subsequently await a chance to buy the next rip.

To put that in more originator friendly terms, as long as this range prevails, it's lowest yield levels continue to be ideal lock suggestions, while it's weaker levels are entry points better suited for float boaters. We still haven't seen enough motivation to change this fact. Until we do, we'd continue to favor playing the range until the range plays us.

{kind=link}