The week ahead is relatively quiet on new data, the housing market will however be in focus with three new reports set to print. Investors will be watching for data on housing starts and building permits, existing home sales, and homebuilder sentiment.

Beyond scheduled economic releases, global markets will be paying close attention on Wednesday to a meeting between Chinese President Hu Jintao and our own President Barack Obama. Reuters says their talks are expected to focus on a host of thorny issues, from rebalancing the global economy to dealing with North Korea and the value of the Yuan. Analysts are calling the visit the most important by a Chinese leader in 30 years given China's growing military and diplomatic influence and its emergence as the world's second largest economy after the United States.

Another potential attention grabber will be debate over whether or not the euro zone's rescue fund needs before new stress tests are performed on Euro zone banks.

The Q4 earnings season also picks up this week with results from Citigroup, US Bank, Goldman Sachs, Wells Fargo, Morgan Stanley, Bank of America, tech heavyweights IBM, Apple and Google, and economic bellwether General Electric. “Expectations are high after strong reports from JPMorgan, Intel and Alcoa,” BMO Capital Markets said.

Here are two posts discussing the status of the bond market and mortgage rates.

Mortgage Rates: Varying Degrees of Opportunity Presented

Stored Energy: The Sideways Freight Train is Running Out of Room

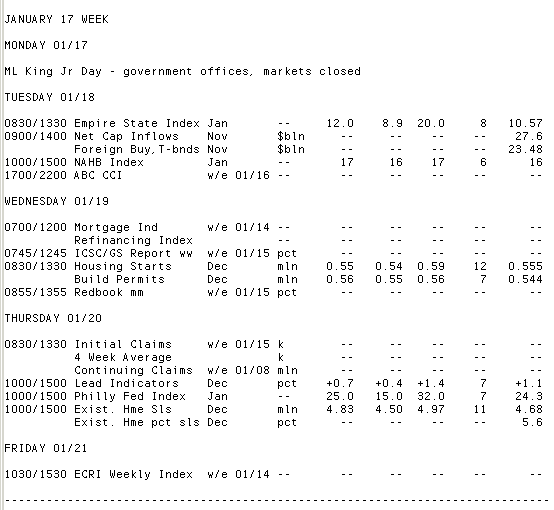

Key Events This Week:

Tuesday:

8:30 ― The Empire State Manufacturing Survey, the first regional manufacturing index released each month, is expected to rise 1.5 points to 12 in January. Forecasts from the eight economists surveyed by Thomson Reuters range from 9 to 20, reflecting the volatility the index has seen over the past three months. The index fell dramatically to contraction levels in November ― the first negative print since July 2009 ― before rebounding to 10.5 in December.

“Because of its small sample size ― about 100 respondents ― the index is often quite noisy,” said economists at Nomura Global Economics. “However, we think the underlying trend of manufacturing activity in the region continues to improve at a steady pace. Assuming few distortions from sampling noise, we expect the index to remain almost unchanged at 10.0 in January relative to the previous month's reading of 10.6.”

9:00 ― Forecasts were not available for the November’s TIC Flows or Treasury International Capital report. The report looks at what the import and export ― or flow ― of U.S. financial instruments, from private buyers as well as foreign central banks.

“We suspect the report will show weaker foreign official flows into US Treasuries, which would be consistent with the rates market sell-off,” said economists at Nomura. “In contrast, private inflows into US assets may have picked up as global investors fled the euro zone. Finally, we look for outflows into foreign bonds and equities to have slowed from an above-normal pace in October.”

In October, net capital inflows totaled $27.6 billion. Foreign purchases of Treasuries totaled $23.5 billion.

10:00 ― Don’t expect much excitement from the NAHB’s Housing Market Index, a measure of homebuilder sentiment. Economists guess the index will rise a single point to 17 in January, still well below the 50-mark indicating optimism. The index has been below that threshold for nearly five years now, and with a glut of houses on the market and unemployment above 9%, there is little reason for construction workers to become more optimistic soon.

“Until job growth strengthens, demand for, and construction of, new homes will remain tepid,” said economists at BMO Capital Markets. “Buyers are attracted to cheaper pickings in the resale market, where distressed properties account for one-third of sales.”

2:45 ― The Financial Stability Oversight Council meets to discuss how to implement the Volcker rule. In addition, the Federal Deposit Insurance Corp. board is expected to meet and discuss the implementation of the Dodd-Frank financial reform law.

Wednesday:

7:00 ― Loan applications to purchase a home fell 3.7% in the latest weekly MBA Mortgage Applications index. Economists remain pessimistic about the level of purchases going forward.

“The nascent improvement in the weekly index of mortgage purchase applications has recently stalled,” said economists at Nomura. “Given the notorious volatility of this measure, we will need to see a few more weeks of data to confirm a change in trend. However, if the index remains at the current level, it would arguably signal that home sales may remain weak for the time being.”

8:30 ― Housing Starts, a measure of new home construction, are expected to fall 5k to an annualized pace of 550k in December. That leaves the index 60% below its historical average, according to analysts at BBVA. Generally, economists blame the the anemic housing recovery on the attractive supply of existing home inventories, plus weak demand. For December, cold weather likely slowed development even further.

“A combination of cold weather in the South, wet weather in the West, and snowstorms that blanketed much of the Northeast and Midwest most likely suppressed housing starts in December,” said economists at IHS Global Insight. “Our projection is that housing starts dropped 2.7% to a 540,000 rate. With the economy slowly adding jobs, we are expecting an increase in housing permits to 562,000.”

In contrast, economists at Nomura look for the annualized rate to jump 2.7% to 570k, with building permits rising 4.8% to 570k.

“The expected improvement reflects a judgment that multi-family starts and permits were artificially depressed in November and should recover strongly,” they said. “However, we also see an improvement in single-family building activity.”

Thursday:

8:30 ― Initial Jobless Claims will be closely watched this week as the market attempts to discover what the underlying trend is. The index saw new claims for unemployment insurance jump 35k to 445k in the week ending Jan. 8 ― the highest level since late October. The expectation is that claims fall back this week to a level closer to the 4-week average of 417k.

“Either the claims numbers are just pure wonky (likely) or businesses are slashing payrolls again (unlikely, since this would fly in the face of every other jobs indicator),” said economists at BMO Capital Markets. “Nonetheless, after climbing for two straight weeks, jobless claims need to reestablish a downward trend before we can confidently anticipate a meaningful pickup in employment.”

Analysts from RDQ added, “Extracting signal from noise is often very difficult early in the new year so we will just observe that despite the sharp rise in claims, the four-week average rose only 5,500 to 416,500, which still puts it below the level seen in the survey week for December payrolls.”

10:00 ― Forecasts are divided for December’s Existing Home Sales Index. The index jumped 5.6% in November to 4.68 million ― the top reading in seven months. For some economists that jump was too big, suggesting a correction in December, while for others it was underwhelming in light of the 10.1% gain in October’s pending home sales index (the strongest predictor for the index).

“November’s increase of +5.6% in existing home sales actually underperformed what was implied by pending home sales so there is a chance that December will see an outsized jump to ‘catch-up’ to pending home sales,” said economists at BTMU. “In that case, existing home sales would finish out the year closer to the 5 million mark. Five million units is well above the housing correction low of 3.84 million units seen in July 2010, but miles below the bubble-induced high of 7.25 million in September 2005.”

Economists at Nomura, however, said December will see a bit of payback from the strong November figure. They add that normal month-to-month volatility will also play a role, as well as inclement weather in some parts of the country.

The consensus forecast is to see an annualized pace of 4.83 million sales, which would mark the fourth increase in five months. Forecasts range from 4.50 million to 4.97 million.

“Nonetheless, with sales likely to stay below 5 million annualized, it could take a while to sell off the overhang of unsold and vacant houses, meaning prices could sag further this year,” added economists at BMO.

10:00 ― The Philadelphia Fed Survey should be relatively stable in January. Analysts forecast the index to rise 0.7 points to 25, with predictions ranging from 15 to 32. The December index rose 2.2 points, much more than forecasters had assumed, as the component for capital expenditure expectations jumped to the highest level in five and a half years.

However, economists at Nomura point out that in the Fed’s Beige Book last week, the region’s growth was described as “erratic” and “choppy.”

“We forecast the index of Philadelphia area manufacturing activity will likely decline by about 2 points to 18.5 in January from 20.8 previously,” they added. “On the inflation side, the prices paid index is expected to remain elevated at 50.0 in the month, inching up from 47.9 in the previous month.”

10:00 ― Leading Economic Indicators, a composite measure seeking to track turning points in the economy, is seen rising 0.7% in the final month of 2010. The index rose 1.1% in November, marking the strongest increase among five consecutive gains. Everything but housing appeared to contribute, one economist noted, as jobless claims declined, interest rates widened, and consumer confidence inched forward, while building permits declined.

For December, economists at Nomura point to a gain based on lower initial claims, higher equity prices and widening interest yield spreads.

Treasury Auctions:

1:00 ― 10-Year TIPS

Friday:

No significant events.