The December Employment Situation Report has been released. The market is digesting two diverging headlines.

The first is Wall Street's preferred hiring indicator: Non Farm Payrolls (Establishment Survey).

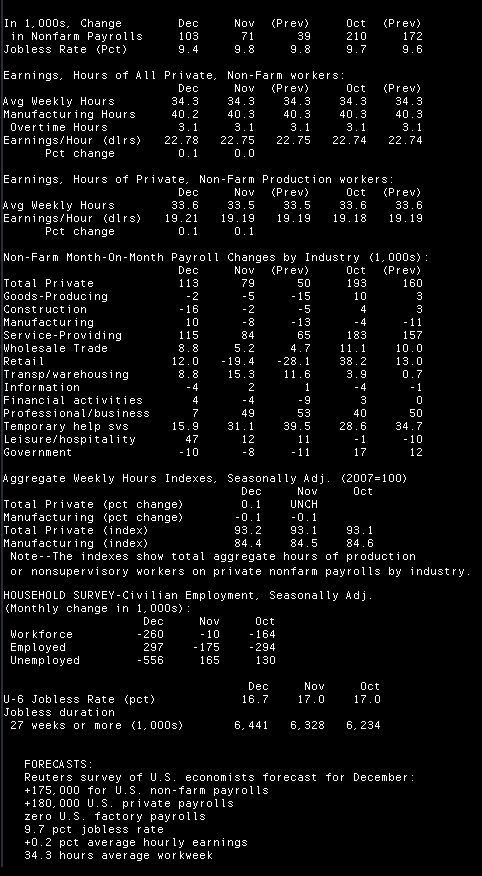

Non Farm payrolls grew by 103,000 in December. This is less than economists had forecast in December but November was revised higher by 32,000 heads to +71,000 (vs. an originally reported +39,000 which is still lower than anticipated). October NFP also saw upward revisions, adding 38,000 more jobs to the tally. So in total, including revisions to the previous month's data, the street is seeing 173,000 more jobs this morning which is close to consensus.

The second metric is more influential on the sentiment of Main Street, the Unemployment Rate (Household Survey).

The Unemployment Rate (UNR) fell from 9.8% in November to 9.4% in December vs. calls for a print of 9.7%. The falling UNR reflects a shrinking labor force and a sharp decline in the number of unemployed as measured by the less quantitative/more qualitative household survey.

Here is the Reuters Quick Recap...

RTRS-U.S. DEC NONFARM PAYROLLS +103,000 (CONSENSUS +175,000) VS NOV +71,000 (PREV +39,000), OCT +210,000 (PREV +172,000)

RTRS-US DEC PRIVATE SECTOR JOBS +113,000 (CONS +180,000), NOV +79,000 (PREV +50,000)

RTRS-U.S. DEC GOVERNMENT JOBS -10,000 VS NOV -8,000 (PREV -11,000)

RTRS-U.S. DEC JOBLESS RATE 9.4 PCT (CONSENSUS 9.7 PCT) VS NOV 9.8 PCT (PREV 9.8 PCT)

RTRS-U.S. DEC AVERAGE HOURLY EARNINGS ALL PRIVATE WORKERS +0.1 PCT (CONS +0.2 PCT) VS NOV +0.0 PCT, TO $22.78 VS NOV $22.75; DEC YEAR-ON-YEAR EARNINGS +1.8 PCT

RTRS-U.S. DEC AVERAGE WORKWK ALL PRIVATE WORKERS 34.3 HRS (CONS 34.3 PCT) VS NOV 34.3 HRS, FACTORY 40.2 VS 40.3, OVERTIME 3.1 VS 3.1

RTRS-U.S. DEC FACTORY JOBS +10,000 (CONS. ZERO) VS NOV -8,000 (PREV -13,000)

RTRS-U.S. DEC GOODS-PRODUCING JOBS -2,000, CONSTRUCTION -16,000, PRIVATE SERVICE-PROVIDING JOBS +115,000, RETAIL +12,000

RTRS-U.S. DEC AGGREGATE WEEKLY HOURS INDEX FOR ALL PRIVATE WORKERS +0.1 PCT VS NOV UNCH

RTRS-U.S. DEC JOBLESS RATE LOWEST SINCE MAY 2009 (9.4 PCT)

RTRS-TABLE-U.S. Dec nonfarm payrolls rose by 103,000

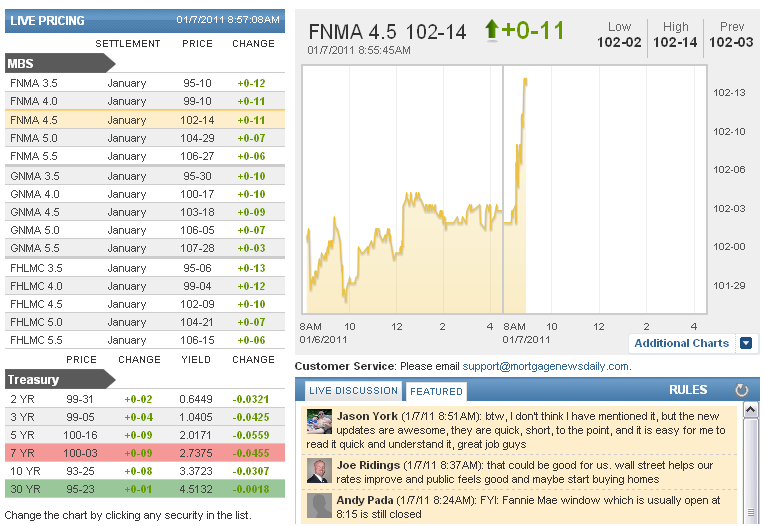

Market Reaction...

Underwhelming & Uninspired. But rates are still slightly lower!

Payrolls growth was disappointing relative to recent "strength" in the labor market as seen in Jobless Claims and ADP. And the bond market knows better than to react to a steep decline in the UNR. It's a smoke and mirrors number based on the amount of people moving in and out of the labor force. President Obama will however be glad to lean on that crutch as a sign of improving conditions. I tend to disagree with that perspective. If the labor market was really getting more liquid folks would be re-entering the labor force not leaving it.

The potential for fireworks still exists when Chairman Bernanke sits before the Senate Budget Committee at 10am.