The market has become more optimistic for Friday’s non-farm payrolls report since

Wednesday’s ADP survey tripled expectations by showing a private

payroll gain of 297,000 jobs.

A number of economists promptly revised their estimates higher, while others were skeptical the report was accurate.

IHS

Global Insight, for instance, revised its forecast for December

employment gains to 190,000, from 150,000, with a prediction of 200,000

private sector jobs versus an original projection of 160,000.

Analysts

from Nomura Global Economics, by contrast, said the ADP number

“primarily reflects seasonal adjustment distortions,” which they said

are common at the end of each year.

“Given these known

distortions and ADP's spotty track record in predicting the BLS count of

private employment, we are leaving our forecasts for Friday unchanged,”

they wrote. “We expect growth in nonfarm payrolls of 165,000 and an

unemployment rate of 9.6%.”

Meanwhile, the jobs component in

yesterday’s ISM non-manufacturing report fell from to 50.5 in December

from a three-year high of 52.7 a month before. Any score above 50

indicates growth, but the slowing pace throws some cold water on the ADP

report, according to economists at BMO Capital Markets.

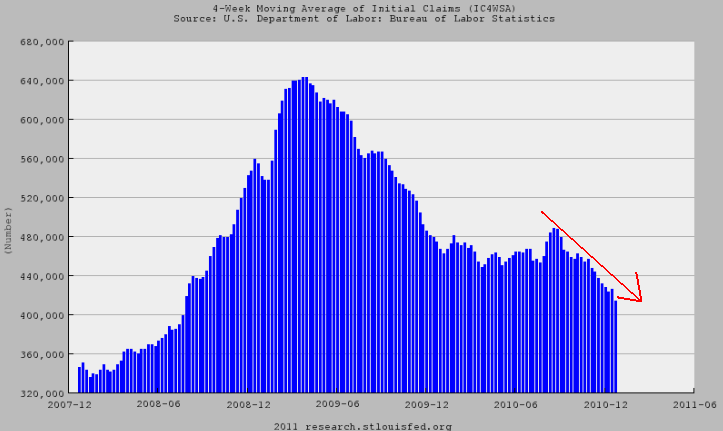

Speaking of the employment situation, initial jobless claims data printed this morning. It is the only piece of major U.S. data to hit the markets today.

The four-week average for Initial Jobless Claims fell 12.5k in

the week ending Dec. 25 to 414k ― the lowest level since July of 2008.

Weekly claims fell 34k to 388k, well below the consensus forecast of

415k. Pleasant as those numbers are, economists promptly called the

surprise report unreliable given the distortions from a four-day

workweek, the holiday season, and so on. (The Labor Department

maintained this was a ‘clean’ report, however.)

For the final

week of the year, economists expected to see a seasonally-adjusted 412k

claims. Many point out that this week too will be dubious, and suggest

we won’t have a reliable figure until mid-January.

“The fact that claims appear to be breaking out of the range held for much of the year ― roughly

450k to 485k ― leads us to believe that the labor market is building

momentum,” said economists at Deutsche Bank, who called the downtrend a

significant development for the economy.

“That being said, we

are somewhat concerned that there could be a measurable weather impact

on the claims and payroll figures as a result of the recent blizzards in

the upper Midwest and Northeast,” they added.

The data was released at 830am, here is an excerpt from the release....

"In the week ending Jan. 1, the advance figure for seasonally adjusted initial claims was 409,000, an increase of 18,000 from the previous week's revised figure of 391,000. The 4-week moving average was 410,750, a decrease of 3,500 from the previous week's revised average of 414,250."

This was largely in line with expecations, but we do note the general downtrend in jobless claims as a positive for the economy overall.

Looking closer, seasonal adjustments appear to be in play again. Here is another excerpt from the release...

"The advance number of actual initial claims under state programs, unadjusted, totaled 577,279 in the week ending Jan. 1, an increase of 52,038 from the previous week. There were 645,446 initial claims in the comparable week in 2010. "

So seasonally adjusted claims rose by 18,000 while unadjusted claims rse by 52,038.

MND's Adam Quinones adds, "We've been seeing much seasonal distortion in the data lately. This forces the street to approach each report from a smoothed out approach, meaning economists and traders are taking each report in context of the recent trend and discounting any outliers as heavily influenced by statistical adjustments. The trend is pretty clear in jobless claims though, they're improving. Only time will tell but at least we're heading in the right direction. In the mean time, we are likely to see counterintuitive behavior while investors examine the accuracy of new reports and reset tactical trades"

That seems to be the case today as equity futures declined sharply as the data flashed across screens eventhough the data was essentially on the screws. The S&P 500 is now 0.07% lower on the day at 1275.70 while the Dow is down 2 points at 11,721. The Dow has risen for three consecutive days this week for a total gain of 1.26% prior to today’s open.

In the bond market we're seeing a modest continuation of yesterday's late afternoon bargain hunting from real money accounts. The 10 year note is +3/32 at 93-05 yielding 3.45%. The FNMA 4.5 MBS coupon is -1/32 at 101-28. Current Coupon MBS spreads are wider vs. benchmarks.

Key Events Today:

No more data.

10:15 - The Fed will purchase an estimated $6-8 billion in Treasury coupons maturing between 1/31/2015 and 6/30/2016

11:00 ― Treasury announces the terms of debt supply to be auctioned in the week ending January 14. 3s, 10s, and 30s will be offered by Treasury.

The December MBS prepayment report will be released this afternoon.