I just finished writing on the December FOMC Minutes. We took a few things from those minutes...

- Look for markets to trade tactically around influential data releases. This means we should see more "buy the rumor, sell the news" frontrunning market behavior around important economic events such as the Employment Situation Report

- Even if economic data continues to improve (segmented), the labor and housing markets are in need of major structural repairs, thus it makes sense that some members have indicated a "fairly high threshold" aka willingness to let QEII run its course as planned.

#1 seems to dictate #2.

One of those "important events" is just ahead. The December Employment Situation Report (ESR) prints on Friday. This data has been our focus for the last three weeks. Why?

The December Employment Situation Report is basically jamming two months of data into one release. Not literally though. Figuratively. If you recall, the November NFRP print was well below even the lowest of economist estimates.(By the way we will also refer to the Employment Situation Report as NFP. NFP = Non Farm Payrolls)

Here is the Reuters quick recap of November NFP data...

RTRS-U.S. NOV NONFARM PAYROLLS +39,000 (CONSENSUS +140,000) VS OCT +172,000 (PREV +151,000), SEPT -24,000 (PREV -41,000)

RTRS-US NOV PRIVATE SECTOR JOBS +50,000 (CONS +152,000), OCT +160,000 (PREV +159,000)

Plain and Simple: The November Employment Situation Report caught the entire market off-guard! And because the market is always right, the market shrugged off the November report as an outlier. It viewed the data as flawed and immediately looked ahead to the December report (released this Friday) to confirm or correct the mistake. Thus the December Employment Situation Report is viewed as a doubly whammy...

We got preview of that data this morning from the ADP National Employment Report. Although this survey only covers private sector hiring, it still serves as a labor market sentiment gauge....and the results were much much better than anticipated.

Here is the Reuters Quick Recap...

RTRS-ADP NATIONAL EMPLOYMENT REPORT SHOWS U.S. EMPLOYMENT INCREASED BY 297,000 PRIVATE SECTOR JOBS IN DECEMBER

RTRS-REUTERS CONSENSUS FORECAST FOR ADP PAYROLL CHANGE FOR DEC WAS FOR INCREASE OF 100,000 JOBS

RTRS-US ADP NOVEMBER PAYROLL CHANGE REVISED TO 92,000 FROM 93,000

RTRS-US ADP DECEMBER PRIVATE-SECTOR PAYROLL ADDITIONS LARGEST SINCE AT LEAST 2001

Excerpts from the Release...

Private-sector employment increased by 297,000 from November to December on a seasonally adjusted basis, according to the latest ADP National Employment Report® released today. The estimated change of employment from October to November was revised down, but only slightly, from the previously reported increase of 93,000 to an increase of 92,000.

This month’s ADP National Employment Report suggests nonfarm private employment grew very strongly in December, at a pace well above what is usually associated with a declining unemployment rate. After a mid-year pause, employment seems to have accelerated as indicated by September’s employment gain of 29,000, October’s gain of 79,000, November’s gain of 92,000 and December’s gain of 297,000.

Strength was also evident within all major industries and every size business tracked in the ADP Report.

According to the ADP Report, employment in the service-providing sector rose by 270,000 in December, the eleventh consecutive monthly gain and the largest monthly increase in the history of the report. Employment in the goods-producing sector rose 27,000, the second consecutive monthly gain and the largest since February 2006. Manufacturing employment rose 23,000, also the second consecutive monthly gain.

Employment among large businesses, defined as those with 500 or more workers, increased by 36,000 while employment among medium-size businesses, defined as those with between 50 and 499 workers, increased by 144,000. Employment among small-size businesses, defined as those with fewer than 50 workers, increased by 117,000.

Construction employment was unchanged in December, ending continuous monthly declines since June 2007. The decline in Construction employment, since its peak in January 2007, is 2,306,000. Employment in the financial services sector declined 8,000 in December.

PLAIN AND SIMPLE: First of all, November ADP data saw very small revisions. I don't know what that means about potential revisions to the November Employment Situation Report, but if we don't see some sort of upward amendment to that release, we are due some leeway from bond traders because the market totally ignored the extremely disappointing November report. Second, HOLY COW...December ADP data was strong. Gains were noted across the board, at least in the services sector. The same cannot be said about the goods producing sector though, which does not paint a positive picture for our unskilled labor force who continues to collect unemployment benefits. Still...we are seeing job creation in private industry...and if the ADP Report has any correlation to the official NFP print...we're due a blowout number on Friday morning. Speaking of correlations, over the last six months the ADP report has understated official private payroll growth (ESR) by an average of 55,000 heads. That implies the private payrolls number in the official ESR data should register a read near +350,000 which is WAY ABOVE current calls for +145,000.

The bond market's reaction to outlier ADP data reflects that sentiment...

Trading flows went sharply negative and volume spiked as ADP Employment Data flashed across screens. This is indicative of not only profit taking but liquidative selling ahead of NFP. We would not be surprised to see frontrunners push 10s as far as 3.50% into Friday morning data as a result of much better than expected ADP data.

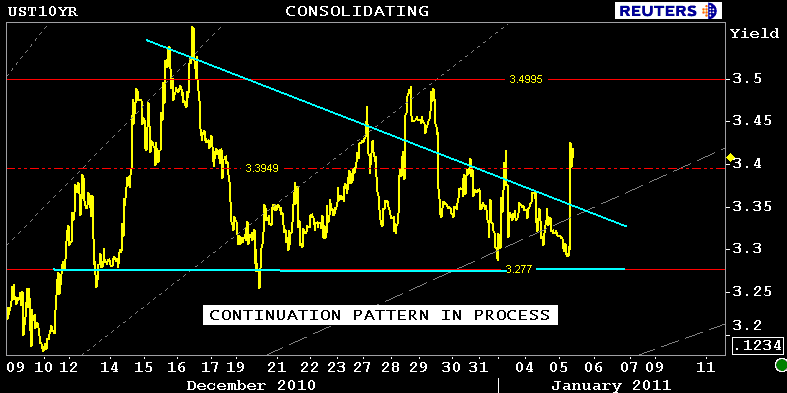

After consolidating in a continuation pattern over the past 4-weeks, stored energy was released after ADP. We have however found support at a highly trafficked, high volume pivot point, one that we've refrenced many times since the post 7-year note auction rally last Wednesday afternoon (RED LINE). A breakdown of this support level gives 10s free run to trade as far as 3.50% without much pushback.

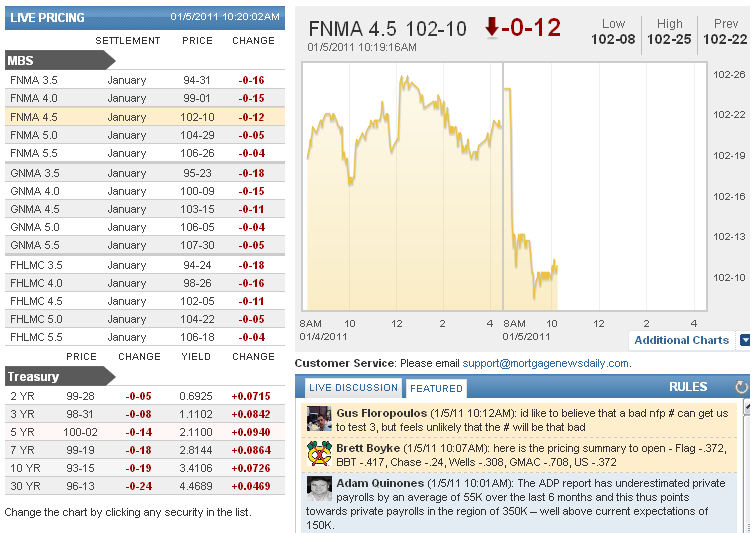

The impact on MBS prices is illustrated on charts via the steep dropoff at 815am. FNCL 4.5 fell from 102-25 to 102-12 in the blink of an eye. Healthy rebate on 4.75 C30 paper was available yesterday. It probably won't be today. If you are basing your lock float decision around the December Employment Situation Report, 4.75% would be a great rate to lock in if you'vel got it. There was a significant increase in lender hedging yesterday which implies lock desks view this Friday's NFP data as a high risk event too (sold forward to lock in potential pipeline profits. Supply still seen in 4.5s)

I've got the secondary market current coupon outperforming on the spot vs. benchmarks but wouldn't be surprised to see further profit taking on the basis as the curve extends (waiting for breakdown of 3.40-42% support in 10s). CC= 4.091% on my book. +68.4bps/10yTSY. +60.5bps/10yIRS. +198.4bps/5yTSY.

It's funny how the bond market ignored an outlier NFP print when it was well below every estimate...but was quick to write a sell ticket on positive outlier ADP data. HERDING AT ITS FINEST! Hey, on the bright side, if 10s trade up to 3.50% it sets the stage for disappointment on Friday morning...which would skew the risk in our favor in terms of the market's reaction. Still, if NFP growth is way above estimates....say hello to 5.00% mortgage rates again.

ADMINISTRATIVE NOTE

We migrated to our new platform over the weekend which caused some problems early Monday morning. We're sorry if you had technical issues.

We understand that some of you tried to register for free trials for our new MBS service, MBSonMND, during this time and your registration was unsuccessful.

We have corrected these issues and free trial registration is open.

Also, thank you to everyone who reported bugs. User feedback is important in helping us identify and correct these bugs.

Thank you for all the positive feedback as well. We love to hear it.