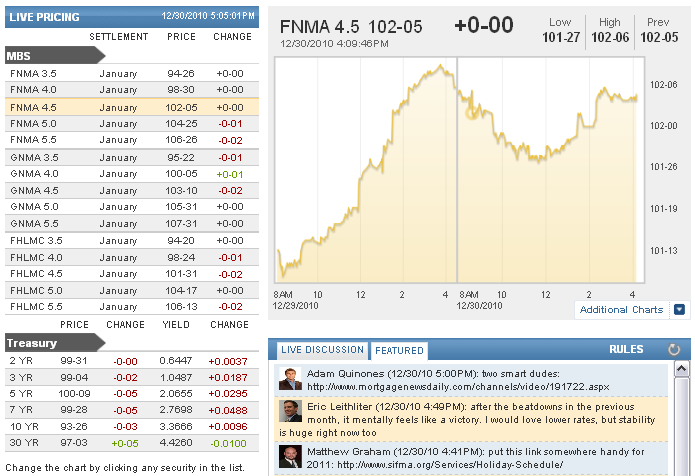

Hooray... The day-over-day change columns for 4.5's and 4.0's now reads +0-00 at the end of the day. But note the absence of an exclamation point on "hooray." This was not some triumphant day where bonds rallied back with a vengeance.

No... Rather, it was a bouncy sort of day with multiple motivations in the market vying for their agenda here on the last full trading day of the year. Don't get me wrong, the net effect sits just fine with me as we're effectively confirming yesterday's gains, just not definitively enough to have much of an opinion about tomorrow. In fact, it's hard not to believe investors will duck away into the hibernatory cave until Jan 7th's employment situation report.

A look at MBS yesterday and today....

When you start seeing flatter movements in the line, such as the one spanning across 2pm, it's often a sign of low volumes and/or lack of liquidity. Indeed MBS didn't make it over 50% of their recent average volume. But with the help of modest month end index extension buying and position squaring, MBS managed to carve out a nice valley, leaving us at break-even on the day. Index buying could have helped more, but whereas it normally arrives on the last day of the month, yesterday's rally coupled with tomorrow's early close deterring the normally late day buying tomorrow, it was instead spread out over today and yesterday.

Treasuries didn't really carve out as distinct a "valley" as MBS though (again, due to widening in the AM and tightening in the PM, MBS are more U-shaped) as the volatility there was seen again and again throughout the day. But in the end, yesterday's post 7-year note auction rally remains largely in place. All in all, volume in treasuries was fairly healthy when compared to the last two weeks, so we'll be content with the 3.367 closing yield (just a few bps above 5pm yesterday. Same as 3pm close).

Remember that tomorrow is a 2pm early close and devoid of econ data, so year-end position adjustments, whatever they might be, will dictate what will likely be a lower volume day. The benefit of yesterday's boomy 7yr auction is that it has probably helped coax a few cards out of the bond market's hand a few days earlier than planned, HOPEFULLY leaving tomorrow to be either a sideways day with moderate volume, or an inconsequential day (even if it does chop around) due to low volume.