The last two economic reports of the year have been released.

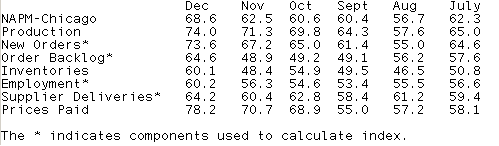

Chicago PMI was much better than expected. Actually that is an understatement. Chicago PMI was way more awesome than anticipated, beating even the most optimistic of forecasts (Reuters high was 66.0). Every component of the index jumped by several points, including prices paid (coughMARGINPRESSUREcough). The overall index hasn't been this high since Reagan was in office and I was 5 years old.

The Pending Home Sales print was also better than expected but my initial reaction to any "better than expected housing data is always "eh". The PHS Index is really just bouncing around near record low levels of activity. Call me when GSE reform is done. Call me when we figure out how in the hell we're gonna deal with excessive excess inventory. Call me when common sense makes it way back into underwriting guidelines and lenders stop overlaying already overdone overlays. Call me when the CFPB is finally set up or when the GFE and TIL are successfully combined.

Here is the Reuters Quick Recap for both reports...

09:45 30Dec10 RTRS-CHICAGO PURCHASING MANAGEMENT INDEX 68.6 IN DECEMBER (CONSENSUS 61.0) VS 62.5 IN NOVEMBER

09:45 30Dec10 RTRS-CHICAGO PURCHASING MGMT NEW ORDERS INDEX 73.6 IN DECEMBER VS 67.2 IN NOVEMBER

09:45 30Dec10 RTRS-CHICAGO PURCHASING MANAGEMENT PRICES PAID INDEX 78.2 IN DECEMBER VS 70.7 IN NOVEMBER

09:45 30Dec10 RTRS-CHICAGO PMI EMPLOYMENT INDEX 60.2 IN DECEMBER VS 56.3 IN NOVEMBER

09:45 30Dec10 RTRS-CHICAGO PURCHASING MANAGEMENT PRODUCTION INDEX 74.0 IN DECEMBER VS 71.3 IN NOVEMBER

09:48 30Dec10 RTRS-CHICAGO PURCHASING MANAGEMENT INDEX HIGHEST SINCE JULY 1988

09:52 30Dec10 RTRS-TABLE-Chicago PMI index 68.6 in Dec vs 62.5 in Nov

10:00 30Dec10 RTRS-U.S. NOVEMBER PENDING HOME SALES INDEX +3.5 PCT (CONSENSUS +2.0 PCT) TO 92.2 - REALTORS

10:00 30Dec10 RTRS-U.S. NOVEMBER PENDING HOME SALES -5.0 PCT FROM NOVEMBER 2009

10:00 30Dec10 RTRS-TABLE-U.S. November pending home sales rose 3.5 pct

Bond Market Reaction....

Not too too bad considering we just had three better than expected economic reports. Rates are still higher but we're generally sideways in a light volume trading environment within the recent range. This behavior is basically par for the course when we look back at the week though. We saw bonds ignore double-dippish home price data and a less confident consumer in favor of auction concessions. And now the bond market is shrugging off a very strong Chicago PMI print, a questionable, but improved read on jobless claims, and a better than forecast ("eh") Pending Home Sales number in favor of month-end index extension buying and year-end position squaring. No better time to remind you of the dominant force behind all price action...

It's a trader's world. We're just living in it.

Muted reaction or not, the curve is slightly steeper, benchmark TSY yields are up, production MBS coupon prices are in the red and yield spreads are wider. (lower and wider = localized weakness in MBS = profit taking)

Unless your lender was lite on the reprices for the better yesterday, rebate will be reduced today. If you gotta lock before January 7th...4.75 is your C30 target. 4.625 on FHA 30 year paper. You be the judge based on your individual scenario. We expect this back and forth behavior to continue until January 7th. Risks are def. skewed toward higher rates today though.