Good Morning. I hope your weekend allowed for much needed R&R. If you're anything like me...it didn't.

I've made a list. I've checked it twice. And yep. Confirmation! I have not finished my holiday shopping yet! Nor am I ready to welcome the holiday spirit into my life. That all changes in the day's ahead though. I will finish my shopping today or tomorrow. After that will be the gift wrapping/card writing party (with a bottle of Gnarley Head Cab)...and then, once all the items on my honey do list are crossed off, I will allocate all my time to what matters most...family and good friends.

These sidetracked sentiments will be illustrated by the market's behavior over the next 10-15 days. Trading volumes will decline. Liquidity will be lacking. And attention rediverted. That means, more than ever, we cannot attempt to rationalize the random, often times contradictory conduct of our benchmark guidance givers and directional dictators.

Unless of course "rationalize" = rally. And then we will be happy to tie some logic to the fact that bonds sold way too far way too fast and a rebound is more than justified. But if we go the other way...let's just blame the lack of liquidity and call it a week. Fair?

HAHA. Note sarcasm please. Just trying to spruce up our stance before we totally disconnect our minds from the movements of mortgage rates.

With everyone now operating under the same assumption....bonds have extended their two day rally into THREE DAYS!!! (the first one was made of straw. the second sticks. the third bricks? Kermit better protect us from the big bad wolf/short sellers!)

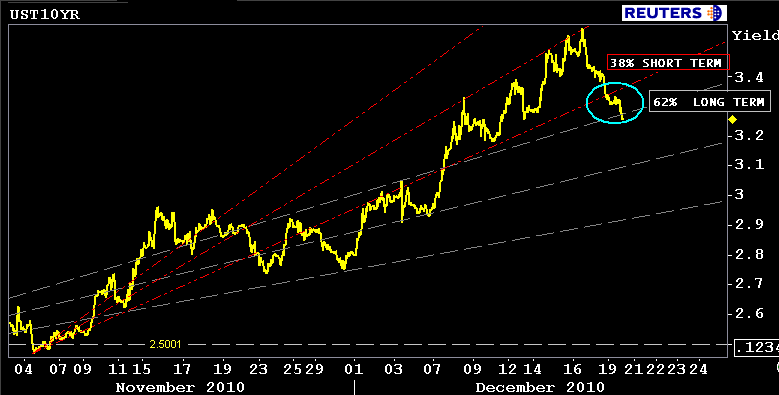

The 10 year note has broken through 3.27/28% resistance and yields continue to trend lower. The 2.625% coupon bearing 10 year TSY note is currently +19/32 at 94-22 yielding 3.265% (-7.4bps). MG and I watch different charts. He likes internal trendlines and trend channels, whereas I prefer to overlay fibonacci fans to project the path of rates. As you can see in the chart below, we've broken the 62% short term retracement and are now testing the 38% long term retracement. Look a little lower and you'll notice 3.00% is the line in the sand we must break to reconsider mortgage rates at 4.25% again. That is where the 62% long term retracement line is located.

We'd love to chase 3.00% into year-end....

The MBS production coupon title belt holder, the FNCL 4.5, has ticked back into the 102 handle after falling as far as 100-07 last Thursday. MBS bargain buyers were seen in the market on Friday (prices higher.spreads tighter) as the yield curve bull flattened and vol lost its bid. This is a positive sign that stored demand is just waiting to be released...but again...the year-end lack of liquidity is playing a role in these moves. I'm paying extra close attention to the MBS options market for further signs of bargain hunting strategery (compelling valuations seen in longer lived MBS coupons after the curve extended)

The FNCL 4.5 is currently +12/32 at 102-12 yielding 4.081% (10 CPR is slow but refi market is dead right now). Here is a screen shot of MBS on MND...

Also in the headlines....

N.Korea says "not worth reacting" to South drill: North Korea's military said on Monday it "was not worth reacting" to South Korea's military drill on the disputed island of Yeonpyeong, the North's state news agency KCNA reported.

Euro at 2-week low vs. dollar: The euro fell broadly on Monday, hitting a record low against the Swiss franc, with more losses likely as investors fretted over euro zone debt problems. The euro also declined to a two-week low versus the U.S. currency and a record low against the Australian dollar as traders still reacted to Moody's multi-notch downgrade of Ireland's credit rating last week.

60 Minutes and Meredith Whitney put municipal bonds back on the front page: Is the US following the EU down the path of scattered defaults? Just like the EU's member "states", U.S. states are having major budget issues. This is a systematic risk to our sovereign debt rating. Then again we can also print money and reflate our way to prosperity if needed. Perhaps QEIII = Muni bonds and BABs? U.S. state and local governments faced the realization on Friday that in just 14 days they will no longer be able to sell taxable Build America Bonds, the federally subsidized debt created in the economic stimulus plan to fund infrastructure projects and create jobs. FULL STORY

If I were a bond vigilante that last story would be my biggest focus in the year ahead. That is of course assuming the EU crisis will be met with a broad-based solution. We haven't seen that yet so it seems easier to focus shorts on the sloppy piecemeal approach being taken by EU leaders to solve their solvency issues...leaving U.S. debt to be a beneficiary of flights to safety.

Plain and Simple: Whether it be made of straw, sticks or bricks, the big bad wolf has yet to blow our house down.