The bond market note got gappy after the Fed completed their latest QEII POMO at 11am. The move has not been originator friendly.

Benchmark 10s have given back almost all of their morning price appreciations and are currently +1/32 at 92-31 yielding 3.467% after hitting an intraday yield low of 3.403%.

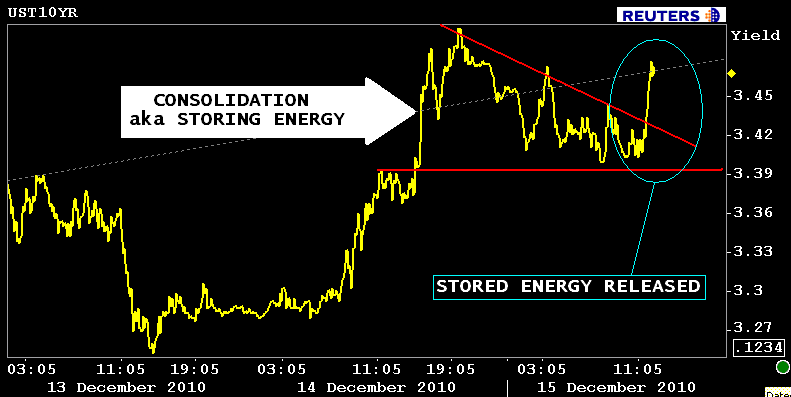

Note the consolidation pattern followed by the release of stored energy. That = short selling in the futures market after 10s failed to breach a technical inflection point.

Rising benchmark yields have pressured MBS prices lower. Blah. The FNCL 4.0 is -2/32nds at 97-31+ vs. the intraday high of 98-16. The FNCL 4.5 is -2/32 at 100-29 vs. the intraday high of 101-07.

These MBS retracements are large enough to warrant reprices for the worse.

WHY: Short covering and a modest real$ bid drove the early AM rate improvements. However once the Fed had finished their latest QEII POMO around 11am flows began to turn on fast$ profit taking and prices began to inch lower, and then all of a sudden the floodgates opened in the futures market. This is where we witnessed the gappy price declines. Open interest and volume are both increasing into the downtrade. This price action is indicative of new short selling which should serve as a reminder of how the market behaves around year-end when liquidity is lacking.Strategic buyers are still sitting on the sidelines.

Bid wanted....