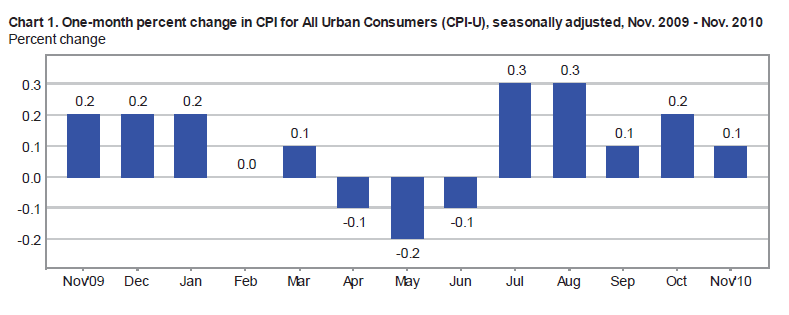

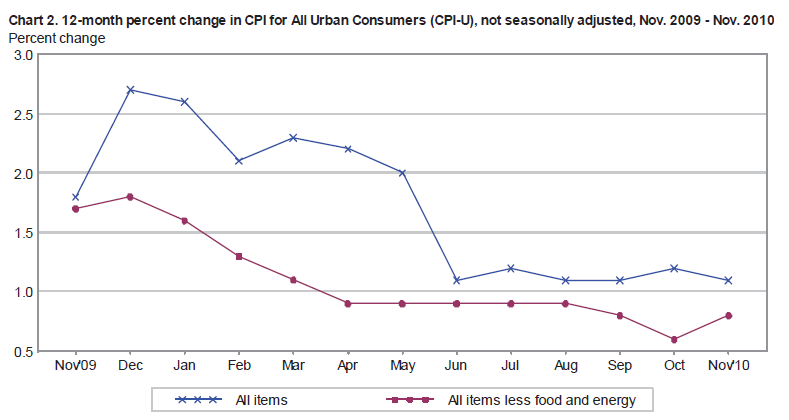

Consumer level inflation data has been released. Month over month headline CPI rose by 0.1% vs. estimates for a 0.2% jump. Core CPI, which excludes the volatile food and energy indexes, was on the screws with a 0.1% increase. YoY unadjusted headline CPI, the digit used to determine real TSY yields and thus breakeven inflation rates, ticked up by a modest 1.1% (consistently this low all year).

Reuters Quick Recap...

08:30 15Dec10 RTRS-U.S. NOV CPI +0.1 PCT (+0.1220; CONSENSUS +0.2 PCT), EXFOOD/ENERGY +0.1 PCT (+0.0979; CONS +0.1 PCT)

08:30 15Dec10 RTRS-U.S. NOV CPI YEAR-OVER-YEAR +1.1 PCT (CONS +1.1 PCT), EXFOOD/ENERGY +0.8 PCT (CONS +0.6 PCT)

08:30 15Dec10 RTRS-U.S. NOV UNADJUSTED CPI INDEX 218.803 (CONS 218.600) VS OCT 218.711

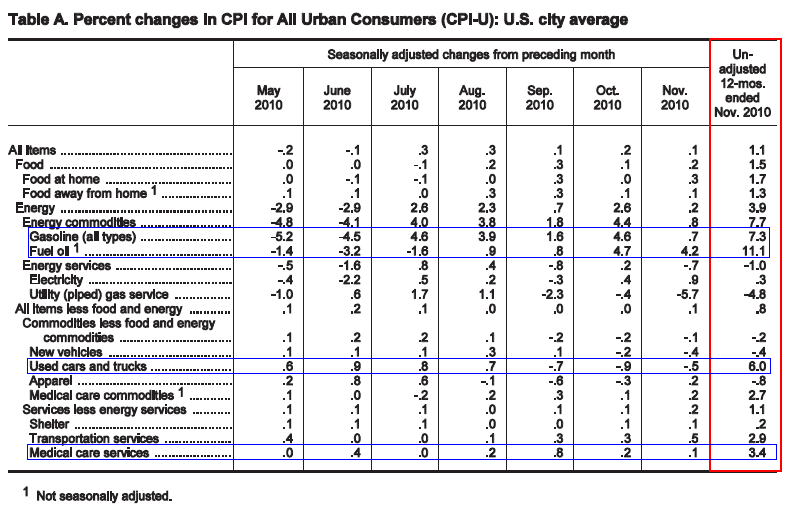

08:30 15Dec10 RTRS-U.S. NOV CPI ENERGY +0.2 PCT, GASOLINE +0.7 PCT, NEW VEHICLES -0.4 PCT

08:30 15Dec10 RTRS-U.S. NOV CPI FOOD +0.2 PCT, HOUSING UNCH, OWNERS' EQUIVALENT RENT OF PRIMARY RESIDENCE +0.1 PCT

08:30 15Dec10 RTRS-U.S. NOV CORE CPI SEASONALLY ADJUSTED INDEX 221.982 VS OCT 221.765

08:30 15Dec10 RTRS-U.S. NOV REAL EARNINGS ALL PRIVATE WORKERS -0.1 PCT (CONS -0.1 PCT) VS OCT +0.3 PCT (PREV +0.3 PCT)

The indexes for food, energy, and all items less food and energy all

increased slightly in November. The index for food at home rose in

November after being unchanged in October, with the indexes for eggs

and

nonalcoholic beverages both rising notably. Although the index for

gasoline rose, the index for household energy declined and the increase

in the energy index was the smallest in five months.

The index for all items less food and energy rose in November after being unchanged the previous three months. Increases in the indexes for shelter and airline fares accounted for most of the rise, while the indexes for new vehicles, used cars and trucks, and household furnishings and operations all declined.

Over the last 12 months, the index for all items less food and energy has risen 0.8 percent. Before season adjustment, the all items index increased 1.1 percent.The energy index has risen 3.9 percent over that span with the gasoline index up 7.3 percent but the household energy index down 0.2 percent. The food index has risen 1.5 percent, with the food at home index up 1.7 percent.

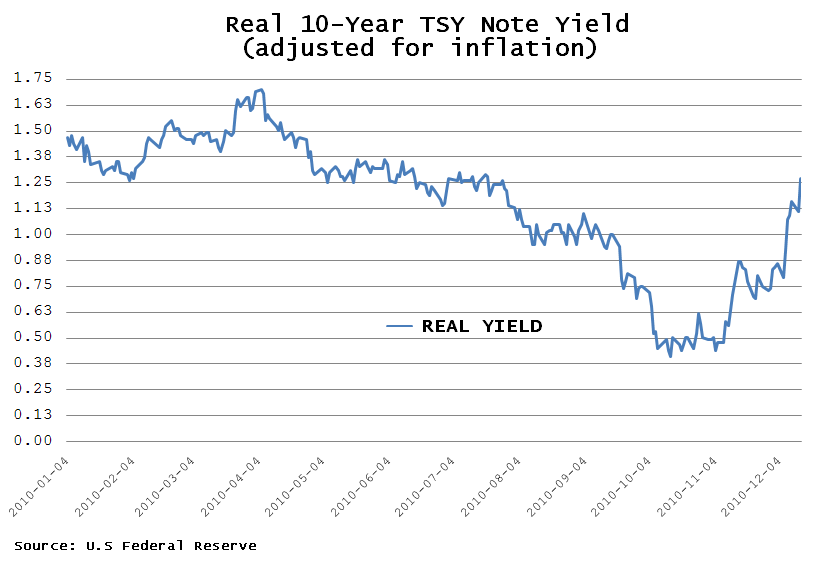

Plain and Simple: Inflation hawks really don't have a crutch to lean on if they're looking to explain the recent run up in rates as a factor of increasing inflationary expectations. CPI data is stale at very low levels. UoM Consumer Sentiment Survey inflation expectations are well grounded. The most recent Philly Fed Survey of Economic Forecasters indicated professional predictors see an average inflation rate of 2.2% over the next 10yrs (vs. previous 2.3%). TIPS breakeven rates have been moving up lately but remain well below their 2010 highs and long run averages (2.22% right now). So in the end, from a quantitative point of view, real yields are rising fast and that paints a compelling picture for bargain buyers who are waiting in the wings. Just another indication that the spike in interest rates has been exaggerated by a lack of trading liquidity and an exhausted group of outright real$ buyers.

Nonetheless, eggs, milk, and gas are getting more expensive and consumers, including myself, are not happy about it. Unfortunately there isn't much the Fed can do to control commodity day trading (herding and momentum), so we have to deal with less disposable income. I guess we won't be upgrading that 42 inch plasma to a 50 inch this year.

Market Reaction...

Yields initially moved higher on the news thanks to a better than expected Empire State Manufacturing Index (+10.57 vs. +5.00) rates have inched lower, back to the best levels of the overnight session. 5s are +10/32 at 97-02 yielding 2.001%. 10s are currently +18/32 at 93-16 yielding 3.403%. The 2s/10s curve is 5bps flatter at 278wide. FNCL 4.0s are +9/32 at 98-11. FNCL 4.5s are +4/32 at 101-12. I've got the current coupon marked at 4.241%. Production MBS coupon yield spreads are wider into the bull flattener. Loan pricing should be better on the open...

It's a segmented recovery. Industrial Production will continue to improve. Businesses will keep investing in technology to enhance productivity. Our trade deficit will hopefully continue to balance out. And Wall Street will surely find a way to profit no matter the environment. That just leaves Main Street to play catch up. Argh. You remember Main Street right? Businesses are investing in technology to replace humans on the assembly line. The household survey portion of the Employment Situation Report is about to get a lot of attention....