Interest rates are trading lower Monday morning after Federal Reserve chairman Ben Bernanke appeared on “60 Minutes” Sunday night.

Bernanke said 2.5% GDP growth is needed to keep unemployment stable and it could take up to five years for the rate to fall under 6%. He not only defended the second round of quantitative easing, the program in which the Fed is injecting $600 billion into the economy ― he said a third round was “certainly possible.”

“Inflation is very, very low, which you think is a good thing and normally is a good thing,” he said. “But we're getting awfully close to the range where prices would actually start falling … That's deflation and that's what happened in the Great Depression.”

The week ahead is pretty light on fresh data until Friday brings in the latest trade balance and consumer sentiment figures. This leaves the broader market to trade in whatever direction momentum takes it based on new information presented on the debt crisis in Europe as well as central bank meetings in Australia

(Tuesday), Canada (Tuesday), New Zealand (Thursday) and the UK

(Thursday). Also influential in the week ahead will be Treasury's next round of debt auctions. Treasury coupon supply totals $66 billion this week consisting of $32 billion 3s on Tuesday, $21 billion 10s on Wednesday, and $13 billion 30s on Thursday.

The stock lever has been exerting pressure on interest rates lately. The S&P 500 moved up 2.42% in the first three days of December, contributing to the 16.7% climb seen since Aug. 31. Stocks even moved up Friday despite nonfarm payrolls posting a minor increase and the unemployment rate ticking up to 9.8%. To some, the advance was a sign that investors are less panicky about the European debt crisis, to others the move is being driven by last minute portfolio reallocations in an effort to enhance year-end performance metrics.

“The stock market took last week’s jobs report in stride, a remarkably mature and grounded response in a market more known for panicked reactions to just about everything,” said Thomson Reuters, noting the index has broken out of a trading range of 1,174-1,200. “Stocks are on the verge of a break above the 62% retracement of the bear market losses and the increased number of new highs reached shows a broadening, and therefore institutional buying.”

Also, the 10 year Treasury yield breached the 3.00% threshold for the first time since July 27 on Friday, however, that move has since retraced about 7 basis points and fallen to 2.94%.

Key Events in the Week Ahead...

Monday:

Dominique Strauss-Kahn, chief of the International Monetary Fund, will present a report on the euro zone economy at a meeting of finance ministers. European Central Bank President Jean-Claude Trichet will also attend. Reuters says the report advocates a larger rescue fund for the euro zone and recommending more bond purchases by the ECB.

12:30 ― Jeffrey Lacker, president of the Richmond Fed, speaks to the Charlotte, N.C., Chamber of Commerce on the economic outlook.

Treasury Auctions:

- 11:30 ― 3-Month Bills

- 11:30 ― 6-Month Bills

- 3:00 ― Treasury STRIPS (zero-coupon bonds)

Tuesday:

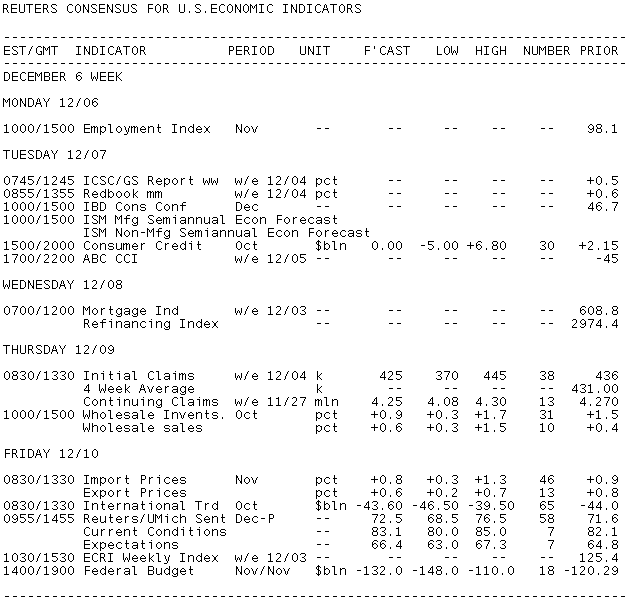

3:00 ― Consumer Credit is expected to be flat in October, following a $2.15 billion increase in outstanding credit a month before ― the first expansion of credit in 2010. Estimates from the 26 economists polled by Thomson Reuters range from a $5 billion contraction to a $6.8 billion increase.

The September report was an anomaly rather than a reversal of underlying trends. Revolving credit ― typically used for daily operations, including credit cards ― fell by $8.3 billion in the month, marking its 25th straight drop, while non-revolving or installment credit grew by $10.4 billion because federal student loans rose $27.0 billion.

“It is important to note ... that trends in the two main types of consumer credit have diverged,” said economists at Nomura Global Economics. “Revolving consumer credit (credit cards) continues to decline nearly unabated. Non-revolving consumer credit (auto loans, etc) have begun to increase, consistent with the pickup in durable consumption.”

Nomura believes an increase in outstanding credit is unlikely to be repeated in October.

Economists at BBVA added that automobile sales are “trending marginally higher” and add some support to non-revolving consumer credit, but they still expect slashes to revolving credit, “in particular outstanding pools of securitized credit card balances and formerly-securitized credit card pools returned to financial institutions’ balance sheets.”

Treasury Auctions:

- 11:30 ―4-Week Bills

- 1:00 ― 3-Year Notes

Wednesday:

7:00 ― The weekly MBA Mortgage Applications index took a major hit in the week ending Nov. 26 as loan application volume decreased 16.5%. On an unadjusted basis, the index decreased 34.2%. Refinancings were down 21.6% as the average 30-year fixed-rate mortgage climbed six basis points to 4.56%. Purchases advanced 1.1% and reached their highest level since early May, yet still remain generally low ― purchases have advanced 2.7% from last year.

Treasury Auctions:

- 1:00 ― 10-Year Notes

Thursday:

8:30 ― Jobless Claims are anticipated to fall 10k to 426k in the week ending Dec. 4. The previous week saw initial claims rise 26k, well above the consensus call but low enough for the market to remain overconfident for the November jobs report a day after. In light of that disappointing release, many will be watching the initial claims figure.

The four-week average is currently at 431k as initial claims have come in below the 450k mark for four consecutive weeks now, suggesting a growing labor market. Continuing claims ― a tally of those still receiving regular benefits ― are anticipated to fall to 4.25 million from 4.27 million.

Economists at Nomura say the previous week’s rise in claims was greater than anticipated, but reiterate that the trend is still heading downwards.

10:00 ― In the Wholesale Trade report for October, inventories are anticipated to rise 0.9%, following the 1.5% boost in September, while sales are forecast to rise 0.6% after a 0.4% gain a month before. Inventories have been rising at an average of 0.7% for the last nine months, according to BBVA, who look for the trend to slow down in the coming months.

“Over the last three months, wholesale inventories increased by 4.3%, which was the fastest three-month growth rate in the history of the series,” said economists at Nomura. “Why wholesalers have begun stock-building at such a rapid pace remains a puzzle. The gains have been broad-based across categories and look mostly unrelated to commodity price increases. We suspect solid growth in trade volumes may be partly to blame.”

Treasury Auctions:

- 1:00 ― 30-Year Bonds

Friday:

8:30 ― The Trade Balance is expected to show a monthly gap between exports and imports of $43.8 billion in October. September’s $44 billion gap marked a 5% decrease from the prior month as consumer goods and auto parts imports fell sharply. Estimates from economists polled by Thomson Reuters range from $39.5 billion to $46.50 billion.

“We expect import volumes to decline on sharply lower petroleum imports, and on a decline in consumer goods imports as pre-holiday inventory restocking comes to an end,” said economists at IHS Global Insight. “We also expect exports to bounce back after two soft months, with industrial supplies and capital goods leading the surge. Overall, we expect trade to be a strong plus for fourth-quarter growth, after being a big drag in the second and third quarters.”

10:00 ― Consumer Sentiment is expected to inch forward to 72.5 from 71.6 as the holiday shopping season gets underway. The Reuter's/University of Michigan survey moved up 2.3 points last month but remains pessimistic overall ― in July the index read 76.0. Signs of improvement weren’t bad though; the current economic conditions component rose to 82.1, its second highest level since April 2008.

“Consumers are feeling more optimistic due to gains in the stock market and an improving trend in the labor market, despite November's poor employment report,” said forecasters at IHS Global Insight. “But their optimism remains constrained by higher gas prices, a poor outlook on the housing front, and uncertainty over the extension of personal tax cuts and emergency unemployment insurance benefits.”

2:00 ― The Treasury’s Budget Statement is anticipated to show a monthly gap of $131 billion in November, compared with $120 billion in 2009 and the 5-year average November gap of $87.3 billion, according to Bloomberg. Estimates from forecasters polled by Thomson Reuters range from $110 billion to $140 billion.

“We expect that the budget balance was about unchanged from the prior year,” said economists from Nomura. “Although receipts have picked up, daily figures from the Treasury also suggest some growth in expenditures during the month.”