"Rate sheet influential" interest rates are marginally lower this morning ahead of an important week of fresh economic data. The schedule includes key manufacturing and construction surveys, consumer confidence and home prices indexes, and concludes with Friday’s Employment Situation Report. Scattered in between we'll get four QEII open market operations, two MBS reinvestment TSY buybacks, and plenty of political debate.

Just over one hour before the opening bell sounds on the street, S&P 500 futures are -0.50 at 1,182.75 and Dow futures are flat at 11,030. Since Nov. 1, the S&P has gained 0.52% and the Dow has shed 0.24%.

The 10 year Treasury note is leading the interest rate rally with a 4bp yield decline and 11/32 price jump. The 10yr note is currently yielding 2.831%. The January delivery FNCL 4.0 is +4/32 at 100-31. The current coupon is 2bps lower at 3.779%. Yield spreads are wider vs. benchmarks.

The news driving markets this morning is the $85 billion Irish bailout plan from the EU/IMF. But overseas, at least, BMO Capital Markets notes the reaction was not as positive as one would have hoped for.

“European bourses are down about 1%, on average,” they wrote. “Ten-year government bond yields in Spain and Italy are up over 10 bps, although Greece and Irish yields have dropped 26 bps and 4 bps, respectively. According to Markit, Portuguese credit default swaps are at 545 bps this morning, and Spain’s are at 350 bps, both a record high.”

Global debt markets seem to believe there are more bailouts to come: FULL STORY

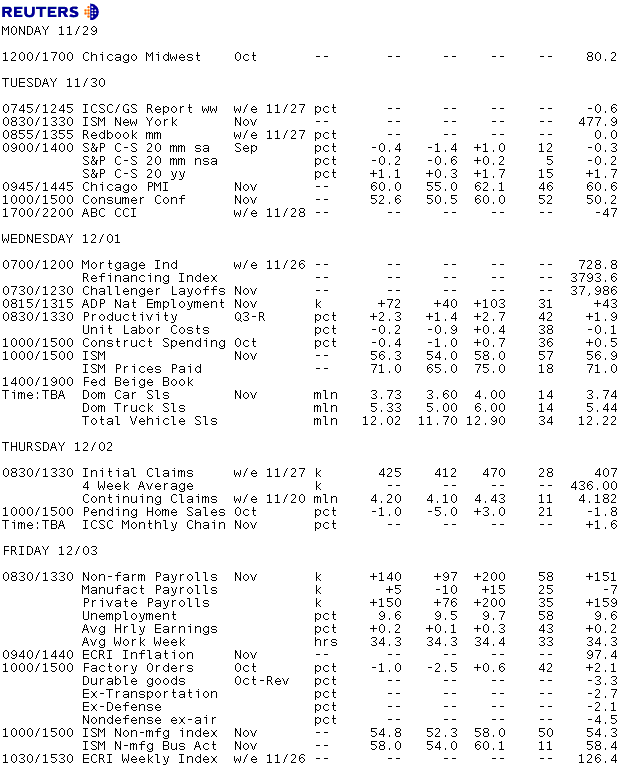

Key Events This Week:

Monday:

Congress holds a session to debate whether to extend Bush-era tax cuts.

10:15am ― QEII TSY Purchases. The Federal Reserve buys $1.5 to $2.5 billion in TSY coupons maturing between 2/15/2021 and 11/15/2027. The desk will also lift $6-8 billion in TSY coupons maturing between 5/31/2013 and 11/15/2014

5:30pm ― James Bullard, president of the St. Louis Federal Reserve, delivers welcoming remarks at the Bank's Regulatory Reform discussion.

Treasury Auctions:

- 11:30 ― 3-Month Bills

- 11:30 ― 6-Month Bills

Tuesday:

The debate on extending the Bush tax cuts continues with President Obama meeting with congressional leaders in the White House. Thomson Reuters says Obama only wants tax cuts for the middle class extended, while Republicans, and some Democrats, want them all extended permanently.

9:00 ― The S&P Case-Shiller Home Price Index, a measure of prices in 20 metropolitan areas across the country, is expected to show prices fall by a seasonally-adjusted 0.4% in September. In the August report, when prices fell 0.3%, the annual change declined from +3.2% to +1.7%; the annual change is now expected to fall to +1.1% in September. The slight fall in prices in August followed four straight increases, but it was expected given the drop in sales after the June expiration of the homebuyers' tax credit.

“House prices look to have softened in September, based on already-reported figures, and we therefore expect another step down in the Case-Shiller index,” said economists at Nomura Global Economics, who look for a 1% monthly drop in prices. “The Loan Performance house price index ― which tends to track the Case-Shiller, but is released a week or so earlier ― fell by 1.8% during the month and stands at -2.8% y-o-y. Weak home sales and ongoing foreclosures point to further weakness going forward.”

9:45 ― The Chicago Business Barometer, a Midwest measure of the manufacturing and services industries, is expected to continue soaring at 60.0 in November. A score above 50 indicates general growth, and clearing this margin by a full ten points indicates rapid recovery. The October level was 60.6, the best score since April. That advance was led by Production jumping more than 5 points to 69.8, while New Orders climbed 4 points to 65.0 and Employment moved up to 54.6.

Economists at Nomura said the regional measure is “quite high” compared to the ISM manufacturing index, which itself is quite healthy. “The pattern is the norm historically: the Chicago index tends to exceed the level of the ISM during expansions,” they wrote. “Given the solid Philadelphia Fed survey, we forecast that the Chicago index will be about unchanged at 60.0 in November. The weakness in the Empire State index suggests some downside risks.”

10:00 ― Economists are forecasting a nice gain in the Conference Board’s measure of Consumer Confidence this month. The consensus prediction from 52 analysts surveyed by Thomson Reuters is 52.6, up from 50.2 in October. Given the recent decline in jobless claims and improvement in the economy, a gain is widely anticipated, but don’t get too optimistic ― BMO Capital Markets points out that “confidence is no higher today than it was at the turn of the year and is stuck at levels normally reserved for recession.”

Analysts at BBVA point out that Consumer Confidence Index has remained virtually flat, since May 2009, but they say fewer jobless claims should have an impact on on current and future conditions.

“In fact, the 4-week moving average of jobless claims declined to 436K in the week ending November 2, the lowest reading since August 2008,” they wrote. “We expect the Consumer Confidence Index to increase slightly in November, consistent with our expectation of slow PCE growth in 4Q10.”

10:15am ― QEII TSY Purchases. The Federal Reserve buys $6 to $8 billion in TSY coupons maturing between 12/31/2014 and 5/31/2016.

5:30pm ―Narayana Kocherlakota, president of the Minnesota Fed, speaks on monetary and fiscal policy substitutes to a symposium on international business and economics in St. Paul.

8pm ― Ben Bernanke, chairman of the Fed, and Sandra Pianalto, president of the Cleveland Fed, discuss the economy with global, regional and local business leaders.

Treasury Auctions:

- 11:30 ― 4-Week Bills

Wednesday:

The Senate Banking Committee holds a hearing on problems in mortgage servicing. Panelists include FDIC Chairman Sheila Bair and Federal Reserve Governor Daniel Tarullo.

7:00 ― The MBA Mortgage Applications, a weekly measure of loan application volume, saw dramatic movement in the week ending Nov. 19, when purchases jumped 14.4%. MBA said the index suggested that consumers were feeling “somewhat more confident with their financial situation” but noted the increase was probably magnified by the comparison to the holiday week before. Still, the number of purchase applications was, on a seasonally adjusted basis, at its highest level since the expiration of the homebuyer tax credit in late June.

“The index of mortgage purchase applications has been languishing at low levels for a few months,” said economists at Nomura. “Unfortunately, this looks to have proven a good leading signal for the recent weakness in home sales. We therefore will be watching the purchase index closely for any signs of improvement, which we think would lead a pickup in new and existing home sales.”

8:15 ― The ADP Employment Report, a measure of private job growth released two days before the Bureau of Labor Statistics’ jobs report, is forecast to show 72,000 new jobs in November, up from 43,000 a month before. Predictions from 32 economists range from 40k to 103k, while economists at Nomura remind us that ADP “has over-predicted the BLS count of private nonfarm payroll employment by an average of 60,000 per month” over the last six months.

“Our model suggests the report will show private payrolls rising about 70k, but it tends to overshoot in November, so we look for a 125k jump,” said Ian Shepherdson at High Frequency Economics.

8:30 ― Productivity & Costs, a Bureau of Labor Statistics measure, looks at productivity by looking at output divided by hours worked. In the third quarter, preliminary results showed productivity rising 1.9% and unit labor costs falling 0.1%. Thanks to revisions showing output in the nonfarm business sector climbing, revised results are anticipated to show productivity at +2.3%, which translates into labor costs falling 0.2%.

“GDP growth in 3Q suggests positive readings for labor productivity,” said economists at BBVA. “Output per hour increased substantially in 2009 as firms sought to become more efficient in order to protect their margins. However, as the labor market recovers, productivity growth is likely to moderate in the coming quarters.”

10:00 ― The ISM Manufacturing Index, an influential measure of nationwide manufacturing, has been above the 50-level indicating expansion for 15 consecutive months, averaging 56.1 according to BBVA. In October the index climbed 2.5 points to 56.9; in November it is expected to decline modestly to 56.3. Regional indexes have been mixed -- the Philadelphia Fed index jumped 21.5 points to +22.5, but New York’s Empire State index weakened.

“The summer lull is breaking up,” said economists at IHS Global Insight. “In regional evidence so far, readings from Philadelphia, Richmond, and Kansas City all showed improvement, although the (less reliable) New York Empire score collapsed, suggesting that all is not peaches and cream, but we expect the national survey to show an improving picture. A key to watch is if strength continues in the export reading.”

10:00 ― Construction Spending, a Census Bureau measure of residential and non-residential construction in the private sector, plus state and federal spending on construction at the public level, is forecast to fall 0.4% in October after rising 0.5% a month before. The previous gain was surprising and reflected a jump in multi-family residential construction and home improvements, according to Nomura, who called the gains temporary.

“The October construction numbers should be a mixed bag,” said economists at IHS Global Insight. “Nonresidential construction and single-family home construction are expected to be down by more than 1%. But increased infrastructure spending should offset these declines, leaving overall construction spending unchanged.”

10:15am ― QEII TSY Purchases. The Federal Reserve buys $7 to $9 billion in TSY coupons maturing between 2/15/2018 - 11/15/2020.

2:00 ― The Beige Book, an anecdotal summary of economic conditions from each of the 12 Federal Reserve districts, is likely to remain dour this month. Last week’s FOMC Minutes report showed the Fed had revised its 2010-2012 outlook downward. Members cited weak indicators of household wealth, tight credit conditions and continued household deleveraging, while real estate investment, jobs, and manufacturing and trade indicators advanced more slowly than anticipated this year.

However, economists at Nomura believe the description could be considerably better this month.

“Auto sales, non-auto retail sales, manufacturing surveys and employment trends have all improved since the last survey,” they noted. “Although the there is little chance the report will indicate a rapid expansion, these signs suggests it could note an improvement relative to the early sluggish pace. Also notable in the report will be the discussion of commodity price developments. We suspect that respondents will note higher input costs, but indicate that they have not passed those costs on to final consumers.”

Thomson Reuters also noted: “The deadline for the Fed to release details of emergency lending during financial crisis under new Dodd-Frank financial regulation falls next week. It’s not clear how much markets are watching for these reports, but they may get a kick out of the Fed’s Beige Book on economic conditions.”

2:10 ― Janet Yellen, vice chairman of the San Francisco Fed, speaks to the Committee for Economic Development on “Fiscal Responsibility and Global Rebalancing” in New York

Thursday:

8:30 ― Everyone will be looking at Jobless Claims this week. The last survey for the week ending Nov. 20 showed just 407,000 first-time claims for unemployment benefits, the lowest level since July 2008 ― a few months before the crash of Lehman Brothers. The 4-week average fell to 436,000, as three of the five lowest readings for 2010 were recorded in the last four weeks. Now, the forecast is to see 425k claims, with estimates ranging from 412k to to 470k.

“Jobless claims have definitively broken out of the range to the downside,” said Ian Shepherdson at High Frequency Economics. “Last week’s drop to 407k may have overdone the extent of the dip in the trend ― and we cannot be sure the Labor Department is right to say not special factors affected the data ― but this has been brewing for a while. … If sustained for a whole month, every 10k drop in weekly claims boosts payroll growth by about 25k.”

Economists at BTMU say a sustained figure below 450k suggests job growth at the national level.

10:00 ― The Pending Home Sales Index, which looks at contracts that have been signed but not finalized, is set to fall 1% in October. The September index fell 1.8%, accurately anticipating the 2.2% drop in existing home sales, which showed sales at a 4.43-million-unit annual rate. The National Association of Realtors blamed tight credit for hurting sales, and that’s unlikely to change soon.

“The index of pending home sales proved prescient last month in signaling the deterioration in existing home sales,” said economists at Nomura. “We think the index will remain quite for the time being, given the lack of growth in mortgage purchase applications.”

Friday:

8:30 ― The October employment report showed Nonfarm Payrolls rise 151,000 in the month, a number that solidly beat expectations as the index climbed for the first time in five months. Private job growth was 159,000, the largest gain in six months and the 10th straight gain. In November, another 140k jobs are to be added to the economy, including 150k private jobs and 5k manufacturing jobs.

“Available indicators suggest the November Employment Report should extend the improving trend evident in last month's release, including revised GDP, retail sales and manufacturing industrial production,” said economists at Nomura. They cited the jobs components of the Philly Fed and Empire State manufacturing surveys, which remained well-above their break-even levels. Of course, the four-week average of initial jobless claims is also extremely encouraging.

“We think the bulk of job gains will come from service-providing sectors, including retail trade, transportation, professional and business services, and health and education,” they added.

Economists at BBVA note that these gains are not big enough to reduce the Unemployment Rate, which is stuck at 9.6%.

10:00 ― The influence of the ISM Non-Manufacturing Index will be limited this month given that it follows the employment report. The index covers the services, financial, and construction industries, and is expected to grow at 54.8 in November, half a point better than a month before.

“Freight volumes continued to increase, consumer spending trends are improving, and manufacturing activity indicators overall continue to be constructive,” said economists at IHS Global Insight. “We expect less of a positive push from the financial sector, and the growth of new orders could also fall back by a couple of notches, so those headwinds should restrain the gain to about a point.”