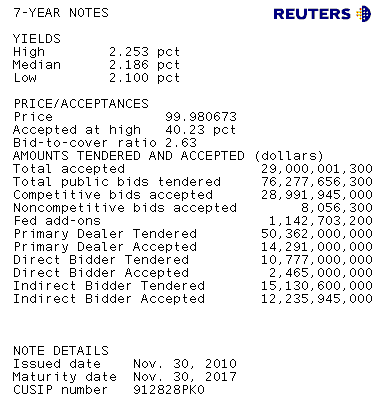

Treasury just auctioned $29 billion 7-year notes at a high yield of 2.253%. This was 1.1bps above the 1pm "When Issued" yield.

The bid to cover ratio, a measure of auction demand, came in at a nine auction low, below average 2.63 bids submitted for every 1 accepted by Treasury. 40.2% of those bids were accepted at the high yield while 50% were awarded at or below the median yield of 2.186%. 5% were awarded at or below 2.10%.

Primary dealers took down $14.3bn or 49.3% of the competitive bid. This is well above average for the street vs. recent 7-year note auctions. Dealers were also awarded an above average 28.4% of the supply they bid on. Remember we don't want dealers getting their hands on too much supply.

Direct bidders added $2.5billion or 8.5% of total competitive tenders. Direct bidders were awarded 22.9% of what they bid on though, this is a below average hit rate.

Indirects took home $12.2billion in new 7-year inventory or 42.2% of the competitive bid. This is well below average and their lowest award in the last eight auctions but their hit rate registered a huge 80.9% of what they bid on.

Plain and Simple: Sloppy auction all around. Low bid to cover, a sizable tail vs. the market's forward pricing mechanism (WI), poor bidder performance vs. recent averages. Blah. It's done. Let's move on.

Market Reaction...

10s and 30s down over a full point in price now. 10s yielding 2.905%. 2s/10s curve back over 236 pivot at 238bps wide. Cash FNCL 4.0s -21/32 at 101-04. We're off the session low print/spread wides but still a ways away from the session highs. Most of this news is not originator friendly, but on the bright side the bleeding seems to have stopped. For now...

The bleeding seems to have stopped for now. READ THIS POST for more info on what I mean by that.