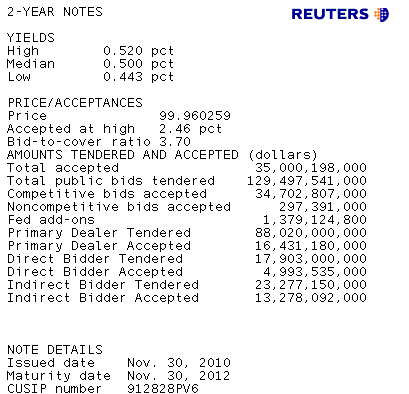

Treasury just auctioned $35 billion 2s.

After peaking at $44 billion and staying there for seven straight auctions, Treasury has slowly reduced the size of its 2-year note fundraisers starting on May 25, 2010. Since then 2-year issues have steadily fallen. This is the 2nd consecutive $35 billion 2-year note offering.

The bid to cover ratio, a measure of auction demand, was 3.70 bids submitted for every 1 accepted by TSY. This well above average BTC ratio illustrates strong demand for the 2-year note.

The high yield, another measure of auction demand, was 0.52%. This is 1.05bps below the 1pm WI yield of 0.531%. The fact that the auction's high yield was lower than the market's pre-auction pricing indication implies bidding was aggressive. This makes sense as 2s were able to build a healthy pre-auction concession vs. the curve and outright. View this is bargain buying.

Primary dealers added $16.4 billion in new inventory or 47.4% of the competitive bid. This is a below average award for dealers who were slightly less aggressive than usual with an 18.7% hit rate.

Directs bid on $17.9bn 2s and were awarded $4.9 billion or 14.4% of the competitive bid and 27.9% of what they bid on. This is an average takedown for directs.

Although indirect buyers failed to match their previous two 2-year note awards, they still took home 38.3% of the competitive bid and 57.0% of what they bid on. The auction award is above average but the hit rate was not indicative of an uber-aggressive strategy.

Plain and Simple: That makes for three slightly less aggressive auction award breakdowns but two strong auction demand metrics (BTC and High Yield). It would appear that all three account categories (the street, directs, and indirects) wanted a chunk of this issue, thus the award was spread out pretty evenly (relative to averages). Although the market was more than willing to let supply cheapen, buyers showed up to cover. For now I see no reason to believe overseas buyers are backing out of our debt

Market Reaction....

The 2s/10s curve is steeper as dealers distribute 2s while the "getting is good". 10s seem to have printed a local high price and are now retesting the price lows of the day. No bid deal though. The 10yr note is currently +11/32 at 98-05+ yielding 2.837%. We hope to see 10s find support around 2.84%-2.85% as this would be another indication that the QEII cleansing process is nearing completion. Production MBS coupons have traded in a tight range all day but we have just touched the intraday lows. The January FNCL 4.0 fell a whopping 3/32 as the auction results flashed (Note sarcasm re: nosedive).

Plain and Simple: the steeper shape of the curve in the minutes after the 2yr auction tells me the AM rally was more a function of auction supply concessions and the Fed's QEII purchases, which were focused in the 10yr sector. This would explain why the long end is underperforming in the aftermath of the auction. That trade was tactical and is being unwound as 2yr supply is distributed by the street. However, in the spirit of the QEII cleansing process, we hope to see some bargain buying if 10s retest 2.84/85. (124-26 in TY)

We'll have an update out soon with charts. For now we're on the defensive as the potential for chopatility in yields remains high.