Rate sheet influential MBS prices are trading higher this morning and lenders have passed along some love.

On average, rebate is 12.9bps better with fuller note rates leading the improvements. Lock desks remain hesitant to get too aggressive with pricing on the note rates used to fill 3.5 trade buckets. This is obvious via a lack of hedging in 3.5 30 year coupons lately. I too have adjusted my current coupon model to reflect a heavier weighting on the FNCL 4.0 MBS coupon. My current weighting in 90/10...again this is a factor of a lack of liquidity in 3.5 coupons. If mortgage rates are to move back below 4.25%, the first hint of it happening will be an increase in 3.5 MBS hedging by originators. Last week the opposite occurred, there was more buying back of 3.5 hedges than selling forward. This is part of the QEII cleansing process as well.

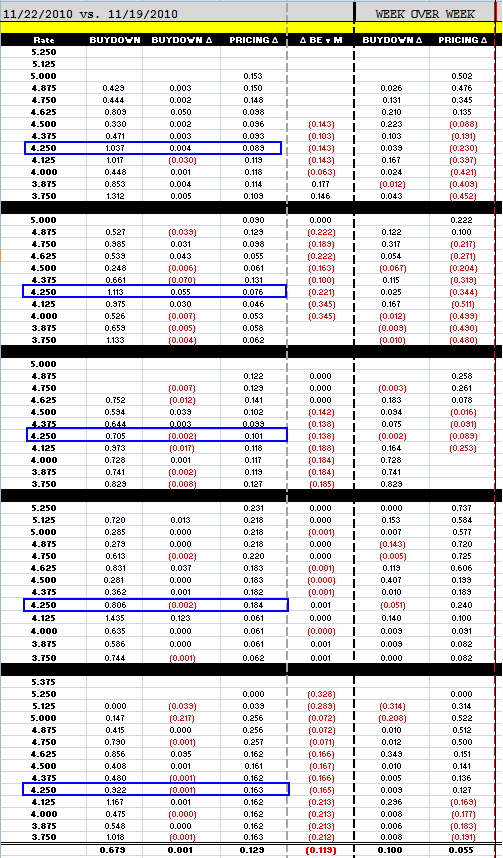

Buydowns are largely unchanged vs. what was offered on Friday but more expensive when you compare on a week over week basis, 10bps on average. Unfortunately a permanent buydown on 4.25 notes remains very expensive and probably not worth the extra closing costs.

EXPLANATION OF LOAN PRICING COMPARISON

Buydowns are the cost of floating down to the next lowest note rate. Buydown costs are matched to the note rate in the same row. For example, the first number in the buydown column is 0.429%, this is the cost to float down from 5.000% to 4.750%, as a percentage of the loan amount (bc they are priced the same!). This is important because it helps an originator determine the best execution rate/points combination for a borrower who has a good idea of how long they intend to keep their mortgage (breakeven on points paid vs. monthly payment savings). In the Buydown Delta column, red is cheaper. Black is more expensive.

The pricing change column is a direct rebate comparison of pricing today vs. pricing yesterday. Red is worse. Black is better.

The BE v M column shows you how margin is changing. Red means more margin. Black means less bps are baked into pricing.

--------------------------------------------------------------------------

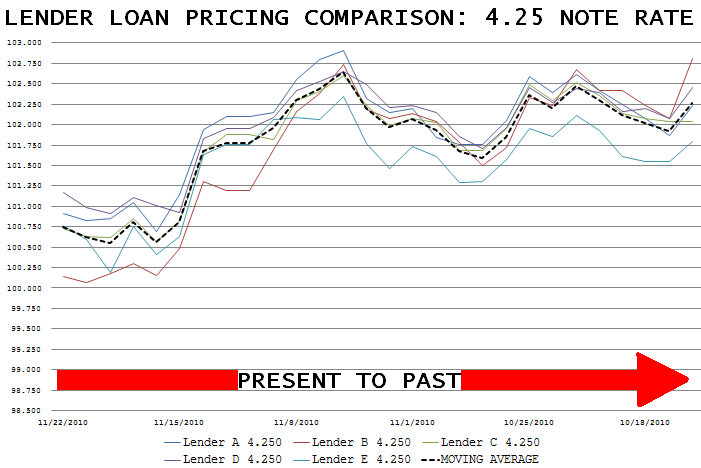

Here is a one month snapshot of pricing on 4.25% note rates. The black dotted line is a moving average. Two of the five major lenders are quoting above average rebate. As you can see, pricing improvements in 4.25 notes today wasn't huge but every lender (besides lender B) are above recent lows.

Remember: read the chart left to right

Treasury is set to release the results of their $35 billion 2-year note fundraiser. 2s are UNCH on the run at 0.509% and the WI is at 0.531%. The 2s/10s curve is 5bps flatter at 231bps wide. Clearly the market has built in a pre-auction concession, both outright and vs. the curve.