Interest rates are rallying after the market heard news that Ireland's Prime Minister Brian Cowen had asked for and will receive financial assistance from the EU and IMF.

“The details of the package still have to be hammered out, but reports put the size of the bailout at €80-to-€95 billion,” said economists at BMO Capital Markets. “It will be 3-year loan, and the details should be fleshed out by the end of November.”

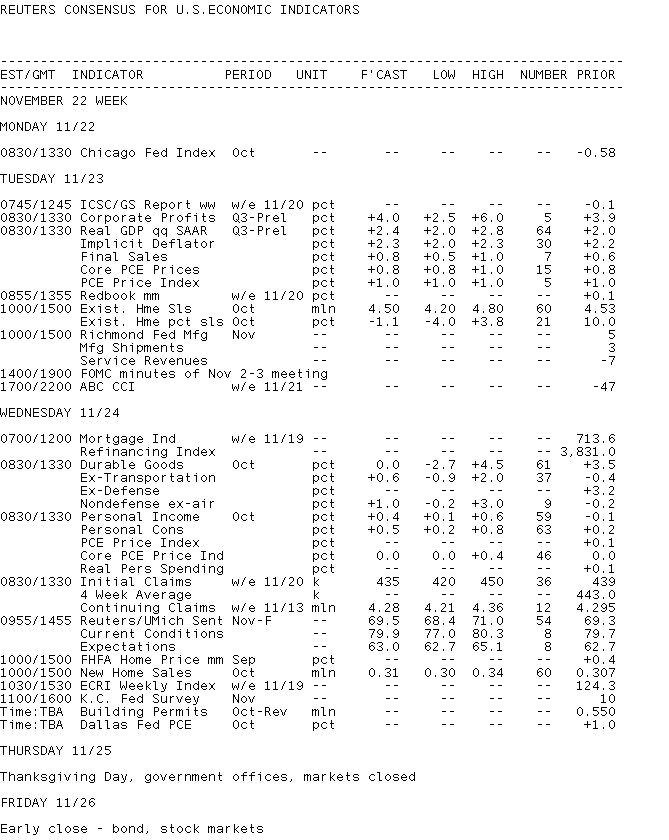

The holiday-shortened week ahead begins on a light note but is chalk full of data on Tuesday and Wednesday.

Economists at IHS Global Insight predict the overall tone of data will be positive on balance, “with third quarter real GDP expected to be revised up, real consumption spending expected to pick up in October and consumer sentiment slated to improve in November.”

Housing continues to be a laggard in the economy. Existing home sales are expected to fall slightly this week, while new home sales are only set to increase marginally.

Key Events This Week:

Monday:

No significant data.

1:30 ― Narayana Kocherlakota, president of the Minnesota Fed, delivers a luncheon speech to business leaders in Sioux Falls, South Dakota.

Treasury Auctions:

- 11:30 ― 3-Month Bills

- 11:30 ― 6-Month Bills

- 1:00 ― 2-Year Notes

Tuesday:

8:30 ― Revisions to third-quarter GDP are expected to boost the measure to an annualized rate of 2.4%, up from the original projection of 2%. Estimates from the 64 economists polled by Thomson Reuters range from 2% to 2.8%.

“Recent economic indicators such as business and wholesale inventories, new residential construction and net external demand point to a stronger economic activity in 3Q10 than previously estimated,” said economists at BBVA.

Forecasters at IHS Global Insight say inventory accumulation should provide a bigger boost than original estimates, while foreign trade should be less of a drag. However, private nonresidential construction should see large downward revision.

Projecting into the current quarter, IHS says to expect 2.5% growth.

10:00 ― Existing Home Sales are expected to take a slight hit in October. Forecasters expect to see an annualized pace of 4.50 million sales, down from 4.53 million in September. Estimates from 60 economists range from 4.20 to 4.80 million. The pessimism largely stems from the 1.8% drop in September’s pending home sales index, versus the consensus call for a 3% gain. The PHSI tracks contract signings, thereby anticipating secondary market sales by a month or two.

Against the consensus, economists at Nomura Global Economics look for a 1.5% increase to 4.60 million sales.

“Despite rapid growth over the past two months, the level of existing home sales remains a bit low compared to pre-federal tax credit levels,” they wrote. “We therefore think sales could rise further this month, despite the weakness in the pending home sales index (a leading indicator of existing home sales).”

On the lower end of the spectrum, economists at IHS Global Insight expect a 6% tumble.

“The Pending Home Sales Index slipped 1.8% in September, and mortgage applications to buy homes fell during October, according to the Mortgage Bankers Association,” they wrote. “The foreclosures mess which led to halts in foreclosures from some mortgage lenders contributed to the expected decline in sales.

2:00 ― Given the unprecedented attacks on the Federal Reserve in recent weeks, there should be lost of appetite to read the FOMC Minutes of the Nov. 2-3 policy meeting. The resulting communique detailed the central bank’s plan to renew quantitative easing efforts with $600 billion of new asset purchases. The minutes should detail how much support chairman Ben Bernanke had in launching the program.

“The QE2 decision is under attack from many quarters ― including from some members of the committee ― and markets have reacted violently since the meeting,” said economists at Nomura. “There is a clear need for formal communication on the latest policy action from the Fed. Indeed, the minutes of the last FOMC meeting specifically noted that the committee itself regards this document as ‘an important channel for communicating participants' views about monetary policy.’”

The minutes will also provide the Fed’s first updates on GDP, unemployment and inflation since the late June meeting.

“We expect major downward revisions to the Fed's forecasts for growth and core inflation, and an upward revision to forecasts for unemployment,” said Nomura.

Treasury Auctions:

- 11:30 ― 4-Week Bills

- 1:00 ― 5-Year Notes

Wednesday:

7:00 ― In the latest MBA Mortgage Applications survey for the week ending Nov. 12, mortgage loan application volume fell a precipitous 14.4%. Refinancings declined 16.5% to their lowest level since July; purchases fell 5%, ending a three week uptrend.

One reason for the sharp drop was a rise in interest rates. The average contract for a 30-year fixed-rate mortgage moved up to 4.46% from 4.28%.

“Rates increased sharply last week due to stronger economic data and lingering uncertainty regarding the structure and impact of the Fed’s QE2 program,” said the MBA. “Mortgage applications, particularly for refinances, dropped in response.”

Economists at Nomura note that purchase applications, despite three weeks of gain before last week’s fall, continue to languish at low levels. “This may indicate downside risks to our home sales forecasts for the next few months,” they added.

8:30 ― Durable Goods are expected to be flat in October following a 3.5% advance one month before. Forecasts are all over the place however, ranging from -2.7% to +4.5%. Not all news is bad though; the core index, defined as non-defense spending excluding aircraft, is anticipated to rise 1% after falling 0.2% in September. The discrepancy arises from September’s 105% monthly climb in non-defense aircraft parts.

Economists at Nomura, looking for a 0.5% increase overall, said October’s industrial production report signaled “very strong growth in business equipment output” and suggests a healthy underlying trend in capital expenditure ― “and therefore core durable goods orders.”

8:30 ― The October Personal Income & Outlays report is anticipated to show wages and consumption rising amid flat inflation. Economists predict income will rise 0.4%, following a 0.1% cut one month before, while consumption will pick up 0.5% after rising 0.2%. Core inflation, which excludes volatile energy and food prices, is set to be unchanged for the second month, providing the Federal Reserve with a defense of its reflationary QE2 measures.

Economists at BMTU note that year-to-year personal income began expanding in December 2009 following eleven months of decline. The growth rate was 3.1% in September.

“While that’s the best growth rate in income since late 2008, it is still about half of the historical average,” BTMU says. “Wages were up +1.7% year-over-year in September, which is the third consecutive month they’ve outpaced inflation since the recession began in December 2007.”

Forecasters at IHS Global Insight look for wages and salaries – which they call “the best guide to underlying trends” – to rise 0.5% in October.

“Higher employment, a longer working week, and increased hourly earnings all drove wages and salaries higher in October,” they said.

8:30 ― Many will be watching the Initial Jobless Claims report to see if the trend in claimants continues to fall. There were 439k and 437k new claims in the weeks ending Nov. 13 and Nov. 6, respectively, which drove the 4-week average to the lowest level since September 2008. A sustained number below 450k is generally indicative of private job growth in the US economy.

“Recent claims reports have increased our optimism about the state of the US labor market,” said economists at Nomura. “If we see another good report this week we will likely push up our forecasts for nonfarm payroll employment growth.”

10:00 ― The Reuters / U of Michigan Consumer Sentiment report bumped up 1.6 points in mid-November to 69.3. The current economic conditions index climbed 3.1 points to 79.7 and the expectations component moved up less than one point to 62.7. Revisions are expected to be minor, with analysts forecasting a 0.2 point gain to 69.5.

“The index of consumer sentiment remains quite low despite higher stock prices and improving economic conditions,” said economists at Nomura. “Given that the index was as high as 76.0 in June, we think further increases from 69.3 are quite plausible. The inflation expectation components of this report signal little risk of deflation.”

10:00 ― New Home Sales, the final bit of new data for the holiday-shortened week, is expected to show the annual pace of sales rise to 310,000 in October, from 307,000 one month before. Last month’s positive employment report provides the hope for more sales in the final quarter of 2010. Extremely low mortgage rates are also a nice incentive.

Analysts at Nomura look for the index to jump 4.2% to 320,000.

“The post-tax credit bust in new home sales looks to have ended, and building sentiment has started to pick up (albeit slowly and from a very low level),” they noted. “Given that new home sales remain quite low, we see room for further increases.”

Treasury Auctions:

- 1:00 ― 7-Year Notes

Thursday:

Happy Thanksgiving! Markets closed.

Friday:

No significant data. Markets are closing early.