Our tension level remains high this morning as tactical day traders squeeze out every last drop of short seller profit in the belly of the curve all the way through the ultra long end. Spec long bond shorts and bear steepeners vs. 30s aren't expected to be unwound anytime soon but the 2s/10s portion of the curve is about to be injected with a QEII shot in the gut. This steady wave of buying will be difficult to overcome as new issuance will essentially be absorbed by the Fed's balance sheet.

The overnight session provided some encouraging price action toward our much needed recovery rally but that originator friendly directionality has since reversed course and we're now retesting the corrective move that took place when the Fed announced QEII details on Wednesday afternoon. I say encouraging because many folks are concerned about overseas accounts losing interest in U.S. debt as their currency appreciates against the dollar. This doesn't appear to be the case so far, bargain buying from foreign real$ accounts has been consistent in both overnight trading sessions and TSY auctions.

My outlook has not changed. It's only a matter of time....for now the street has an opportunity to buy 'em at a cheaper price so they can sell 'em back to the Fed at a higher price in the future. I view it like an auction concession....

The preliminary read on November Consumer Sentiment has been released.

Here is the Reuters quick recap...

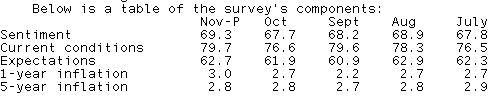

RTRS-THOMSON REUTERS/U. OF MICH US CONSUMER SENTIMENT PRELIM NOV 69.3 (CONSENSUS 69.0) VS FINAL OCT 67.7

RTRS-THOMSON REUTERS/U. OF MICH CURRENT CONDITIONS INDEX PRELIM NOV 79.7 (CONSENSUS 77.0) VS FINAL OCT 76.6

RTRS-THOMSON REUTERS/U. OF MICH CONSUMER EXPECTATIONS INDEX PRELIM NOV 62.7 (CONSENSUS 63.5) VS FINAL OCT 61.9

RTRS-THOMSON REUTERS/U. OF MICH 12-MONTH ECONOMIC OUTLOOK INDEX PRELIM NOV 70 VS FINAL OCT 67

RTRS-THOMSON REUTERS/U. OF MICH 1-YEAR INFLATION OUTLOOK PRELIM NOV 3.0 PCT VS FINAL OCT 2.7 PCT

RTRS-THOMSON REUTERS/U. OF MICH 5-YEAR INFLATION OUTLOOK PRELIM NOV 2.8 PCT VS FINAL OCT 2.8 PCT

RTRS-THOMSON REUTERS/U. OF MICH CONSUMER SENTIMENT, CURRENT CONDITIONS INDEXES HIGHEST SINCE JUNE

RTRS-THOMSON REUTERS/U. OF MICH 1-YEAR INFLATION OUTLOOK HIGHEST SINCE MAY

RTRS-TABLE-Reuters/U Mich Nov. prelim sentiment index 69.3

It looks like rising equity indexes and a run of better than expected econ data combined with a more balanced Congress and Fed asset purchases are helping to improve consumer sentiment. Also note the uptick in inflationary expectations. QEII is already working. If you don't believe that just listen to the moaning coming out of countries who've pegged their currency to the dollar. Remember a weak US dollar makes foreign imports more expensive and leads Americans to purchase more American made goods. The weaker dollar also gives foreign demand the opportunity to purchase American made goods at a lower price, thus increasing demand for US goods and services x 2.

Plain and Simple: Here's to hoping a weaker U.S. dollar combines with cost-push inflaiton to force wage growth and increase consumer spending. Pipe down emerging economies, you will go no where without the U.S....give the Fed's plan a chance to work. No one else offered up a better one.

Market Reaction...

10s touched 2.60% before London opened. Since then 10s have backed up as far as 2.713%. 10s are currently -10/32 at 99-16 yielding 2.682% (+3.4bps). The 5 year note is -9/32 at 99-29 yielding 1.27%, this is a key inflection point in 5s. 7s are -15/32 at 99-25+ yielding 1.906%.

10s are running into a mess of technical resistance which is one reason why CTA/black box/quant/ day traders are making our life miserable.

You might have noticed that I've been covering 5s and 7s a bit more than usual. 5s and 7s are used by the street as an MBS hedging instrument. I have generally focused my efforts on 10s from a pipeline managers/loan pricing sensitivity point of view because their duration matches up better to the current coupon IMO, but it's time to broaden our horizon, especially with the Fed focusing their coupon passes in the belly of the curve.

Rate sheet influential MBS coupons valuations are under some pressure as implied volatility catches a bid, but on the spot we're pacing the curve/are slightly tighter. I gotta assume lock desks are buying back hedges and real money is buying MBS outright at the perceived price lows.

The December FNCL 3.5 is -8/32 at 99-14 and the FNCL 4.0 is -7/32 at 102-05. We just bouncing around near the intraday lows...

The Fed had to delay their first QEII coupon pass but we should be seeing results shortly after 1130.

Personal Note...

My grandmother passed away this morning. Please say a prayer for her and my family.