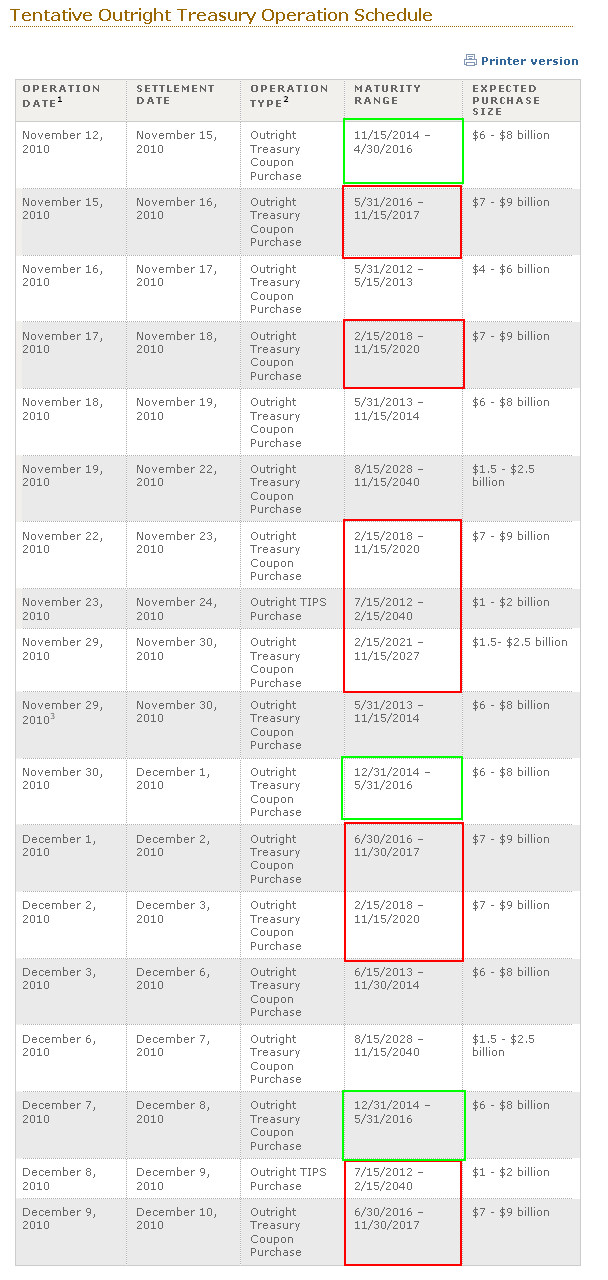

The QEII asset purchase schedule has been released by the FRBNY Trading Desk.

Reuters Quick Recap...

RTRS-FED TO BUY ABOUT $105 BLN TREASURIES AND TIPS IN 18 OPERATIONS FROM NOV 12 THROUGH DEC 9 - NY FED

RTRS-FED BUYING REPRESENTS $75 BLN FROM $600 BLN NEW PURCHASE PROGRAM, $30 BLN FROM MATURING AGENCY/MBS

RTRS-FED OPERATION SIZE ESTIMATES RANGE FROM $1 BLN TO $9 BLN

RTRS-FED TO ANNOUNCE NEXT SERIES OF PURCHASES AT 2 PM EST ON DEC 10 - NY FED

Across all operations in the schedule listed below, the Desk plans to purchase approximately $105 billion. This represents $75 billion in purchases of the announced $600 billion purchase program and $30 billion of principal payments from agency debt and agency MBS expected to be received between mid-November and mid-December.

The next release of the approximate purchase amount and tentative outright Treasury operation schedule will be at 2 p.m. on December 10, 2010. This release will also include information on prices paid for securities included in the operations listed above.

PLAIN AND SIMPLE: The Fed will conduct 18 open market asset purchases over the next 19 trading sessions. They will spend about $105 billion which works out to around $5.8 billion per operation. 9 of those operations will have a direct influence over "rate sheet influential" MBS coupons (red), with at least $45 billion allocated toward the belly of the curve. If you add in purchases that include the 5yr sector (green), which is a benchmark for many MBS hedgers, this total rises to 12 of the 18 operations and at least $63 billion with a max potential for $84 billion focused on our rate sheet influential benchmarks. This is great news for mortgage rates.

QEII starts on Friday with $6-8 billion focused on 2014-2016 maturities....

MARKET REACTION...

10yr TSY futures are testing their session highs but finding it difficult to break black box day trader resistance. In cash, the 10yr note is -6/32 at 99-15+ yielding 2.686% (+2.3bps). Well off the price low of 98-20 and the yield high of 2.78%. The 5yr note is -2/32 at 99-31 yielding 1.257%. Off its price low of 99-16 and yield high of 1.353%. The 7yr note is +3/32 at 100-00 yielding 1.875% (-1.7bps). Off its price low of 99-11 and yield high of 1.974%. The 2s/10s curve gaped out as far as 229bps wide and is now only 2bps steeper on the day at 224bps wide.

2.67% is resistance...

The Janaury FNCL 4.0 is -1/32 at 102-09, well off its low of 101-28. Not a huge rally but it's positive progress. 10s got break 2.67% resistance. FNCL 4.0s got push through the 102-10 pivot.