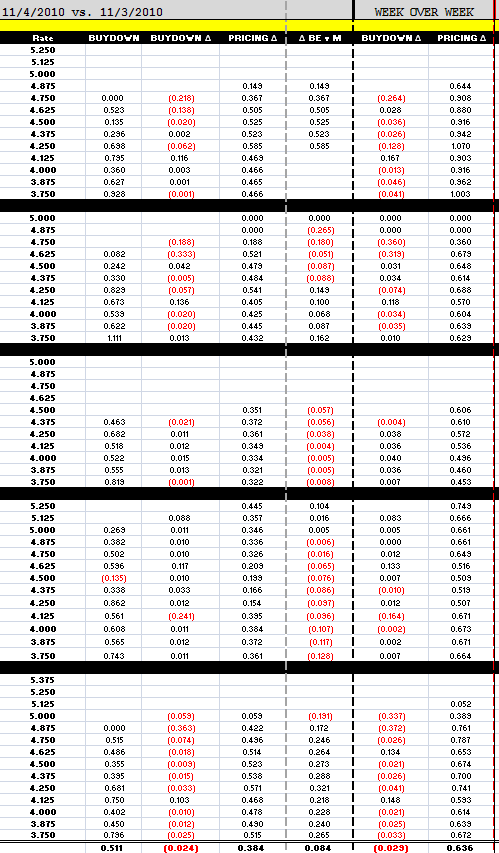

I have some good news to share. Lenders aren't holding back bps. The majors are going for it.

Loan pricing is QEII-tastic today....

On average, rebate is 38.4bps better this morning with the largest pricing improvements seen in note rates at or below 4.25%. When I say "lenders are going for it", that is obvious via tighter primary/secondary loan pricing spreads. See the BE v M column, it shows you how margins are changing. RED means more margin. BLACK means less bps are baked into pricing. Three of the five majors have reduced how much juice they've got baked into rate sheets. Like I said...they're going for it!

Par mortgage rates below 4.00% are definitely on the board in the broker and direct banker market. Retail lenders are all over the place. Keep in mind that their pricing strategies are largely a function of capacity constraints. That means if you write loans for a retailer, be extra cautious about your rate quotes. If your desk gets aggressive and fills their pipeline, they will hit pricing to slow production. This is news to nobody working for a retailer, it's a daily occurrence.

DISCLAIMER: Not all lenders will be this friendly. Some will be hesitant to get "QEII-tastic" until the bond market settles into a range. Others are still dealing with long turn times and have no incentive to overburden their staff with more files. This includes the mid-majors and regionals. However, as long as MBS prices continue to hover near record price highs, the primary market will remain competitive.

EXPLANATION OF LOAN PRICING COMPARISON

Buydowns are the cost of floating down to the next lowest note rate. Buydown costs are matched to the note rate in the same row. For example, the second number in the buydown column is 0.523%, this is the cost to float down from 4.75% to 4.625%, as a percentage of the loan amount. This is important because it helps an originator determine the best execution rate/points combination for a borrower who has a good idea of how long they intend to keep their mortgage (breakeven on points paid vs. monthly payment savings). In the Buydown Delta column, red is cheaper. Black is more expensive.

The pricing change column is a direct rebate comparison of pricing today vs. pricing yesterday. Red is worse. Black is better.

The BE v M column shows you how margin is changing. Red means more margin. Black means less bps are baked into pricing.

I do not show the actual price lenders are paying for loans. This is too much info. I would get angry emails from lock desks and production managers. I will tell you this though, the comparison is based on raw pricing. There isn't another markup built into my model.

-------------------------------

Uber-aggressive loan pricing has been made possible by QEII. This is the reaction we were expecting in the bond market. Both rate sheet influential MBS coupons and benchmark Treasuries have rallied all morning. Cash market TBAs are bid at record high prices and the 2s/10s yield curve is sharply flatter. I hope you didn't panic and pull the trigger prematurely..

Clearly the belly of the curve is the top performer. The 5yr note is +14/32 at 101-02+ yielding 1.028% (-8.8bps). 7s are +26/32 at 101-04 yielding 1.702% (-12.4bps). 10s are +27/32 at 101-07+ yielding 2.482% (-9.7bps). The long bond is +0-06 at 97-04+ yielding 4.041% (-1.0bp).

The 10 yr note has run into resistance. Remember yields below 2.466% are considered QEII "sugar high" territory. Thus we should be expecting the market to push back a bit here, especially when looking at how many times 2.466% has already been rejected. This doesn't mean 2.466% won't be broken though, we just need to give the market more time to find its preferred range.

As mentioned, cash market TBA prices have hit new record highs. This will surely create some resistance as fears of faster prepays set in and negative convexity takes over, which is obvious in back month coupons (what your loan pricing is based on).

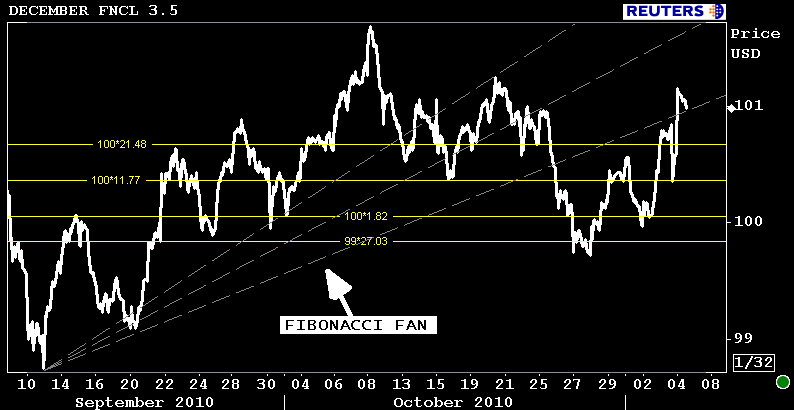

The December delivery FNCL 3.5 is +14/32 at 101-01. The December FNCL 4.0 is +12/32 at 103-15. Based on my model, the secondary market current coupon is 3.387%. Yield spreads are 7bps wider on the spot as fast money accounts take profits on the basis and originators hedge their pipelines by selling loan supply forward. Plus TSYs are rallying and 10yr swap spreads are at 10 month wides. I'd avoid 4.5s, that's where real negative convexity will be found (prepays print tonight).

I added a fibonacci fan to my 3.5 chart and removed the internal trendlines we've watched for so long. MBS prices could move higher but TSYs will have to extend their rally and MBS will probably lag. Still there is room to run higher...

If your lender was a bit hesitant with loan pricing this AM, you are due a reprice for the better.

LOCK OR FLOAT?

There is still room to rally but mortgages are now looking expensive vs. benchmarks, that means "rate sheet influential" MBS coupons will likely lag into an extended TSY rally. Then again the chase for yield is on and bond investors will take every opportunity to buy on any price dips. We're taking a breather at the moment. Let's see how this plays out before making any rash decisions.

I will say this though. If you can pull the trigger on a mortgage rate below 4.00% without pushing the borrower's breakeven on closing costs out past 5 years, I would have a very hard time passing on that deal. The lowest I think we'll go is 3.75%. I will alert if 3.0 coupons (30yr paper) get some attention though...