Tic Toc Tic Toc...

Are we there yet? When does this class end?? What time is it??? It's not 2:15 yet???? The countdown continues...

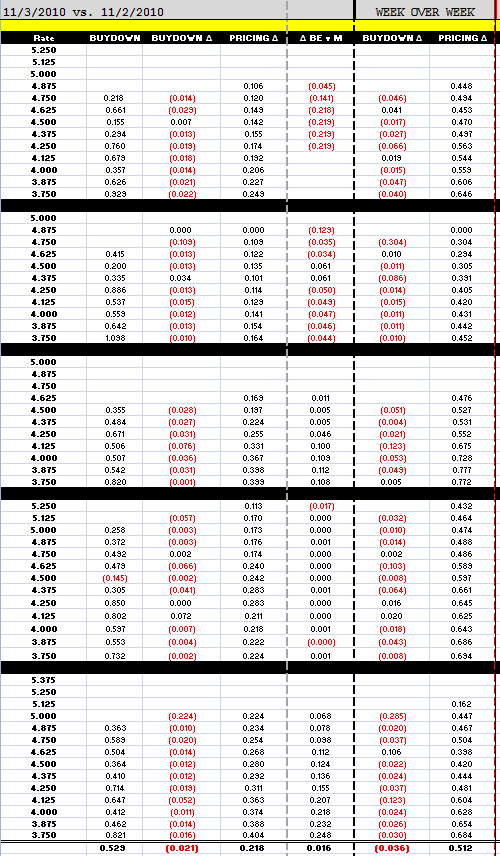

Lenders improved loan pricing this morning. On average rebate is 21.8bps better with the largest improvements seen in note rates at or below 4.25%. Add that to the 20bp reprice you received yesterday and 3.875% is above par on rate sheets again, but closing costs/floatdowns are slightly more expensive (see red buydown Δ). Week over week, rebate is 51bps better.

EXPLANATION OF LOAN PRICING COMPARISON

Buydowns are the

cost of floating down to the next lowest note rate. Buydown costs are

matched to the note rate in the same row. For example, the first number

in the buydown column is 0.218%, this is the cost to float down from

4.875% to 4.75%, as a percentage of the loan amount. This is important

because it helps an originator determine the best execution rate/points

combination for a borrower who has a good idea of how long they intend

to live in their home (breakeven on points paid vs. monthly payment

savings). In the Buydown Delta column, red is cheaper. Black is more

expensive.

The pricing change column is a direct rebate comparison of pricing today vs. pricing yesterday. Red is worse. Black is better.

The BE v M column shows you how margin is changing. RED means more margin. Black means less bps are baked into pricing.

I

do not show the actual price lenders are paying for loans. This is too

much info. I would get angry emails from lock desks and production

managers. I will tell you this though, the comparison is based on raw

pricing. There isn't another markup built into my model.

To be sure everybody is up to date on what we should be expecting, I've pulled a few more comments from Ben's Jackson Hole speech. The comments below are his words, not mine, I've just arranged them in a manner that makes it easier to understand the Fed's thought process.

Policy Options for Further Easing

Notwithstanding the fact that the policy rate is near its zero lower bound, the Federal Reserve retains a number of tools and strategies for providing additional stimulus...

- Conducting additional purchases of longer-term securities: I believe that additional purchases of longer-term securities, should the FOMC choose to undertake them, would be effective in further easing financial conditions. However, the expected benefits of additional stimulus from further expanding the Fed's balance sheet would have to be weighed against potential risks and costs. Another concern associated with additional securities purchases is that substantial further expansions of the balance sheet could reduce public confidence in the Fed's ability to execute a smooth exit from its accommodative policies at the appropriate time. Even if unjustified, such a reduction in confidence might lead to an undesired increase in inflation expectations. (Of course, if inflation expectations were too low, or even negative, an increase in inflation expectations could become a benefit.)

- Modifying the Committee's communication: A second policy option for the FOMC would be to ease financial conditions through its communication, for example, by modifying its post-meeting statement. As I noted, the statement currently reflects the FOMC's anticipation that exceptionally low rates will be warranted "for an extended period," contingent on economic conditions. A step the Committee could consider, if conditions called for it, would be to modify the language in the statement to communicate to investors that it anticipates keeping the target for the federal funds rate low for a longer period than is currently priced in markets. Such a change would presumably lower longer-term rates by an amount related to the revision in policy expectations.

- Reducing the interest paid on excess reserves: A third option for further monetary policy easing is to lower the rate of interest that the Fed pays banks on the reserves they hold with the Federal Reserve System. Inside the Fed this rate is known as the IOER rate, the "interest on excess reserves" rate. The IOER rate, currently set at 25 basis points, could be reduced to, say, 10 basis points or even to zero. On the margin, a reduction in the IOER rate would provide banks with an incentive to increase their lending to nonfinancial borrowers or to participants in short-term money markets, reducing short-term interest rates further and possibly leading to some expansion in money and credit aggregates. However, under current circumstances, the effect of reducing the IOER rate on financial conditions in isolation would likely be relatively small. The federal funds rate is currently averaging between 15 and 20 basis points and would almost certainly remain positive after the reduction in the IOER rate. Cutting the IOER rate even to zero would be unlikely therefore to reduce the federal funds rate by more than 10 to 15 basis points. The effect on longer-term rates would probably be even less, although that effect would depend in part on the signal that market participants took from the action about the likely future course of policy.

- The FOMC increases its inflation goals: A rather different type of policy option, which has been proposed by a number of economists, would have the Committee increase its medium-term inflation goals above levels consistent with price stability. I see no support for this option on the FOMC. Conceivably, such a step might make sense in a situation in which a prolonged period of deflation had greatly weakened the confidence of the public in the ability of the central bank to achieve price stability, so that drastic measures were required to shift expectations. Also, in such a situation, higher inflation for a time, by compensating for the prior period of deflation, could help return the price level to what was expected by people who signed long-term contracts, such as debt contracts, before the deflation began.

Plain and Simple: I'd expect to see strategies 1 and 2 in the FOMC statement at 2:15. The Fed will likely set aside at least $500bn to conduct open market operations, which will occur in unquantified waves as needed. Tools 3 and 4 are much less likely but the Fed should lower its inflation and employment outlooks with a formal update to follow in the "Summary of Economic Projections", which will be released with the FOMC Minutes of this meeting on November 24.

As for the market, remember this is a trader's world, we're just living in it. From that perspective....

If you're really that nervous about the outcome of the FOMC meeting, you could always lock in a few floaters with investors who allow float downs. That's about as panicky as I'd get though. Locking immediately after the FOMC statement is released based on the market's knee jerk reaction is not a good idea, that is unless the Fed says "No QEII for You", in that case feel free to pull the chute and panic lock. I'll be sure to sound the alarm bells if that occurs, otherwise be patient. The Fed will have their way with the market, it's quantitative easing and the Fed is WELL AWARE of how important it is to keep the markets happy.