Key Events This Week:

Monday:

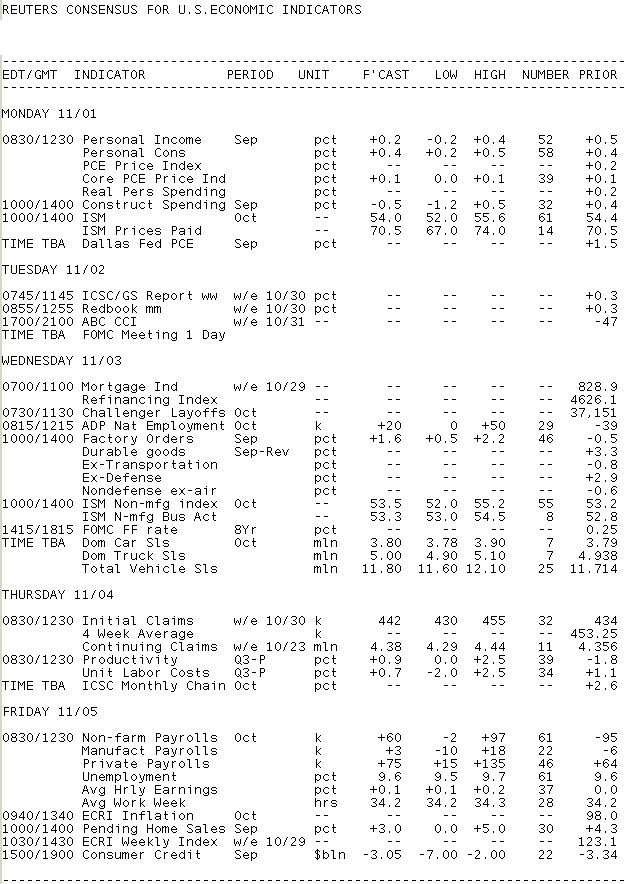

8:30 ― The Personal Income & Outlays report is expected to report that income rose 0.2% in September, compared with +0.5% a month before. Economists note that the big jump in the prior month received a boost owing to the reinstatement of the extended jobless benefits, while September will mark a return to the underlying trend. Meanwhile, personal consumption is anticipated to once again rise 0.4%, and core inflation should repeat its 0.1% climb.

Analysts at BBVA say private sector employment creation and earnings growth should support income growth, but they forecast marginal growth in the final months of the year.

“Consumer spending has been supported by low interest rates, the fiscal stimulus and modest employment gains,” BBVA said. “The latter, however, continues to be weak, thus limiting the consumer spending. We maintain our forecast of slow economic growth for the rest of the year and into 2011.”

10:00 ― The ISM Manufacturing Index, a key barometer for the nation’s growth, is expected to slow down slightly in October to 54.0 from 54.4, or 4 points above the break-even point. That level is consistent with economic recovery, but not of strength. Meantime, the prices paid component, which rose 9 points in September is expected to stay at 70.5, indicating manufacturers continue to be squeezed by higher costs, which have been rising for 15 months.

“This widely watched measure of the manufacturing sector has held up well in recent months despite being buffeted by headwinds from a slowdown in orders momentum and erratic production growth,” said economists at IHS Global Insight. “Little has changed to move the goods portion of the economy to faster growth, but a reading of 54.4 still shows forward progress.”

10:00 ― Construction Spending is expected to decline 0.5% in September, more than erasing the prior month’s 0.4% gain and continuing the 1.4% decrease from July. Aside from the headline, evaluating the public sector versus the private sector will be key. In the last report for August, private expenditure for residential and non-residential construction fell 0.3% and 1.4%, respectively, marking the fourth straight declines, while public spending for construction was up 2.5%.

“August was a good month for public construction,” said economists at IHS Global Insight, noting that infrastructure spending accounted for the headline gains.” We are expecting another strong month for this category in September — with the gains, again, coming from infrastructure spending. But this will be offset by declines in both private nonresidential and residential construction, with total spending inching down slightly, by 0.1%.”

Treasury Auctions:

- 11:30 ― 3-Month Bills

- 11:30 ― 6-Month Bills

Tuesday:

No significant events as the Federal Reserve’s two-day meeting begins and mid-term elections take place.

10:00 ― The Census Bureau releases Q3 Housing Vacancies and Homeownership data.

- Treasury Auctions:

- 11:30 ― 4-Week Bills

Wednesday:

7:00 ― As homeowners take advantage of low mortgage rates, the weekly MBA Mortgage Applications index continues to exhibit a high level of refinancings, but demand for purchase applications remains weak at near 14-year lows.

8:15 ― The ADP Employment Report, a tool used for predicting the “official” employment numbers on Friday, is expected to report that 20k new private jobs were created in October. The report’s usefulness isn’t always clear though ― last month it said 39k private jobs vanished in September, while two days later, the Bureau of Labor Statistics said 64k jobs were created.

10:00 ― The ISM Non-Manufacturing Index, which measures the services, construction, and financial sectors, is anticipated to come in at 53.5 in October, pretty unchanged from the 53.2 a month before. At just a few points above the 50 level indicating growth, the index suggests the economy is growing but only modestly, much like the GDP report last Friday.

“Employment conditions improved marginally in October, and freight volumes picked up, reversing a slight decline in the preceding month, but new orders momentum probably eased downwards,” said economists at IHS Global Insight, who added that financial market conditions also generally improved.

2:15 ― The Federal Reserve is expected to release the details of a proposed second round of quantitative easing in the latest FOMC Meeting Announcement.

Economists at BBVA say the market has already priced in $1 trillion of additional long term treasury securities purchases, but the final number and timeline are still unclear.

“A gradual approach is feasible, and the announcement amount could be significantly smaller than expected,” BBVA said.

The forecasting team at Deutsche Bank believes the Fed will decline from committing to a total amount of asset purchases. Instead, it could provide a maximum amount of Treasury buying to undertake between FOMC meetings, which are every six or seven weeks.

“We envision the Committee stating its intention to purchase up to $125 billion of Treasuries on an inter-meeting basis, with policymakers then reviewing those purchases at the ensuing meeting,” Deutsche Bank predicts. “This means we could see $1 trillion of additional Treasury purchases per annum in addition to the roughly $400 billion in maturing MBS that will be replaced by Treasuries.”

IHS Global Insight believes asset purchases may be calibrated to the performance of the economy.

“So if growth and inflation revive fairly quickly, the Fed could adjust its end target downwards, and vice versa,” they wrote. “Market expectations have been all over the map, but at this point at least $500 billion is already discounted in rates and equities, so if the Fed announces less than this amount the market reaction would be mildly negative.”

Thursday:

8:30 ― There have been an average of 453k Initial Jobless Claims in the past four weeks. Economists generally believe a sustained figure below 450k is indicative of job growth in the economy, so by that measure the labor markets are more or less on the cusp of growth. In the most recent period, weekly claims fell 21k to 434k ― there would be reason to be excited if claims remain near that level over the next month, but economists are forecasting a rise to 442k in the final week of October.

8:30 ― Preliminary estimates for third-quarter Productivity & Costs are expected to show that productivity levels grew 0.9% from July to September, while unit labor costs rose 0.7%. In the second quarter, productivity fell an annualized 1.8% and labor costs rose 1.1%. Despite the GDP figures for the same period already being released, estimates range widely ― productivity forecasts range from flat to +2.5%, and cost predictions range from -2% to +2.5%.

Economists at IHS Global Insight believe unit labor costs will rise a mild 0.3%, resulting from a 3% increase in output and a 3.3% increase in hourly compensation.

- Treasury Auctions:

- 1:00 ― 10-Year TIPS

Friday:

8:30 ― The October Employment Report is anticipated to show 60k were created in October, including 75k private sector jobs. In September, the economy lost 95k jobs, but mostly as a result of temporary Census jobs exiting the data stream ― private employment grew by 64k in the month. No such distortion should be in this report.

Economists at BBVA note that the expected increase will be the first in fourth months.

“Job creation has been driven by sustained growth in private services employment,” they wrote. “Meanwhile, government layoffs will continue at the federal and local level, though at a slower pace.”

The Unemployment Rate, however, is set to remain at 9.6%.

Economists at IHS Global Insight even expect it to rise a tad closer to the 10% mark.

“The unemployment rate is expected to edge up slightly to 9.7% from 9.6%, since the economy is not generating enough jobs to keep pace with the underlying growth in the labor force,” they wrote.

9:30 ― Thomas Hoenig, president of the Kansas City Federal Reserve, will discuss the economy at the National Association of Realtors conference in New Orleans.

10:00 ― The Pending Home Sales Index is expected to rise 3% in September, following a 4.3% gain in August and a 4.5% gain in July. The report follows last week’s existing home sales report from last week, which showed sales jump 10% in September to an annualized pace of 4.53 million. But, sales were still down nearly one-fifth compared to one year ago.

“Strength was relatively broad based,” noted Deutsche Bank economists, speaking of the August report. “As we have noted previously, decade low mortgage rates and near record highs in affordability should help stabilize sales in the near term, however it will take meaningful improvement in the labor market to drive housing going forward.”

3:00 ― Consumer Credit is anticipated to fall for the 8th consecutive month in September, this time by $3.05 billion versus the $3.34 billion cutback a month before. What this means is up for debate. On the positive side, less outstanding credit suggests consumers are deleveraging ― that is, paying off debt and spending less recklessly with money they don’t have. On the negative side, less credit means less growth in the economy, and may also indicate that banks are reluctant to give out loans.

Since January, consumer debt has shrunk $37 billion, according to economists at IHS Global Insight. They noted last month that the rate of decline of household debt has been slowing since the beginning of 2010, “indicating a slow recovery on the consumer side that goes in hand with very gradual improvements in employment and housing conditions.”