The first step in revisiting record low mortgage rates was taken today. Selling in the long end of the curve stopped out, shorts were covered, prices rose and long open interest increased. This all occurred BEFORE Treasury auctioned $29 billion 7s. The pain trade is juuuust about played out and we're setting up nicely for a month-end rally tomorrow, the last trading day of October.

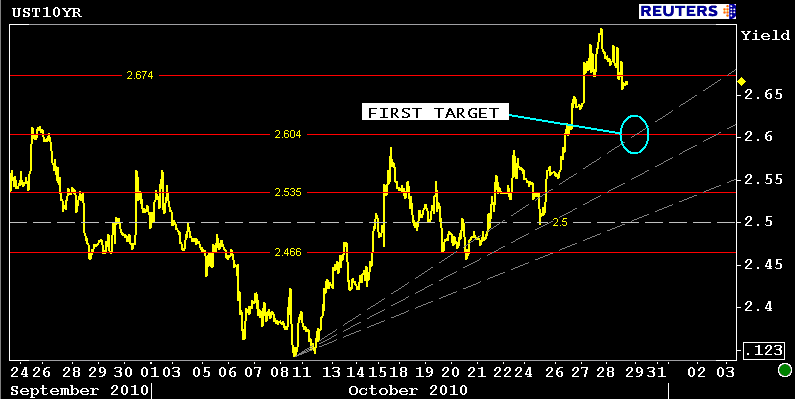

The 10yr note finished +18/32 at 99-22 yielding 2.661% (-6.8bps). 7s were the top performer on the curve, rallying 10.6bps down to 1.938% (vs. 1.97% auction stop). The 2s/10s curve bull flattened a modest 2bps as the 2yr note experienced it's own 4.7bp rally. The long bond was the weakest link with a 4/32 price rally and a meager .08bp decline in yield. Clearly this is indicative of a steepener bias in the way long end of the curve, which is to be expected if you're operating under the assumption the Fed will be successful in reflating the monetary base, cost-push inflation is inevitable (which would hopefully lead to demand pull inflation as those who have jobs demand higher wages). From that perspective, a 4.052% 30 year bond yield just isn't full enough. Some folks might also be betting the Fed doesn't venture that far out the curve too. Then again..if the Reds are to retake the House, the logical response should be bull flattener but with this election who knows. I do know that I'm very tired of hearing nasty political ads though. The MD governor's race has gotten out of control. I'm surprised the two candidates haven't turned to photoshop yet. Cartman/Coon and Friends style. Poor BP

Technically the turn-around (profit taking and new position adding) was much needed. If 10s had broken and followed through 2.70%...2.85% wasn't far off in the distance. The turn around was expected though, not because technical targets had been hit, more so because it's month-end and the November 3rd FOMC meeting is next Wednesday. Play time is over (pain trade), traders should be squaring positions today and preparing for QEII again.

Mortgages are preparing for QEII. Banks were buying back hedges while fast money was doing their own bargain buying at the perceived price lows. Relative value accounts are setting up a short on the belly of the coupon stack, where prepay risk and negative convexity are most prevalent (4.5s and 5.0s). 3.5s and 4.0s were the best performers. This was a function of the flatter shape of the yield curve, a lack of originator loan supply (waiting for prices to rise before selling forward), and modest real money asset/liability balancing bid.

The December delivery FNCL 3.5 went out +15/32 at 100-06. The December FNCL 4.0 ended the session +10/32 at 102-21. My version of the current coupon closed 5.5bps lower at 3.489%. This would put the most aggressive par 30 year fixed mortgage rates somewhere near 4.00%, which is about where rebate goes underwater on a rate sheet, according to my model. Reprices for the better were reported this afternoon, but they were not broad based. You are due better pricing from lenders but I'd expect to see hesitancy...no need to draw in new locks when the odds of rates moving lower are strong next week. That would increase your pipeline fallout and hedging costs!

Looking at previous price behavior of the FNCL 4.0, 102-21 is a familiar inflection point. 103-00 is overhead resistance.

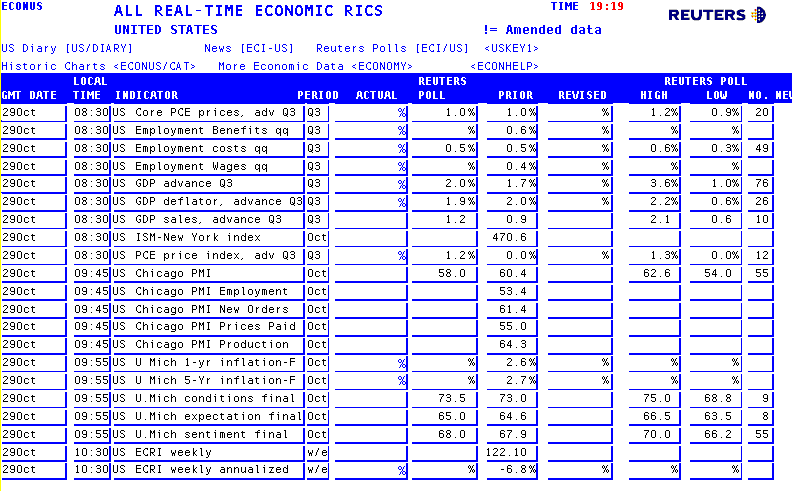

A deluge of data hits screens tomorrow. The Fed has gone ghost ahead of the FOMC, we won't hear a peep from them until next Wednesday. I'd expect to hear a ton of rhetoric on all the rights and wrongs related to QEII though! Month-end buying starts in the afternoon hours....

I have a new show: OUTSOURCED

Based on some of the comments and emails I am receiving, it sounds like a lot of MBS Commentary readers are not Mortgage RateWatch blog readers too...

If you haven't seen it yet, this post paints a pretty clear picture of my QEII outlook: MORTGAGE RATE ALERT: Don't Panic