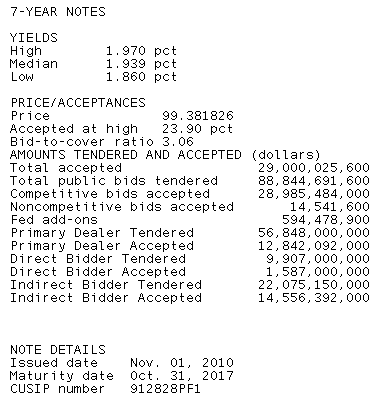

The US Treasury just sold $29 billion 7-yr notes. (Remember, bills typically have a maturity of less than 1 year, notes from 2 to 10 years, and bonds' maturity is generally greater than 10 years.)

Leading up to the auction, the 5-yr was yielding 1.25%, the 7-yr was 1.97% , and the 10-yr was 2.68%. Rates dropped quickly soon after the 1PM EST deadline, while equities remained steady.

The bid to cover ratio, a measure of auction demand, was 3.06, meaning that about 3 bids were submitted for every 1 accepted. This is the highest bid-to-cover ratio in the 21 7-yr auctions since the government began auctioning them again.

The auction came in at a yield of 1.97%, which was a few basis points above the 1pm "When Issued" yield.

Directs were awarded 5.5% of the competitive bid and 16.0% of what they bid on. This auction award is a noticeable improvement from the previous 7-year auctions but the hit rate was low.

Indirects took home about 50.2% of the issue - a relatively strong level. Compare these numbers to yesterday's 5-yr auctio . It had a bid-to-cover ratio of 2.82, with indirect bidders buying about 39% and direct bidders buying 12%. It was termed as "decent" with the lack of indirect buyers being made up for by direct bidders and primary dealers.

Plain and Simple: Overall, this 7-yr auction was very well received, and has pushed benchmark yields lower. It is definitely the best auction of the week. Indirect buyers were strong, as were the primary dealers and directs. The results play well into the thinking that fixed income securities may have sold off more than they should have in recent days.

REPRICES FOR THE BETTER ARE POSSIBLE