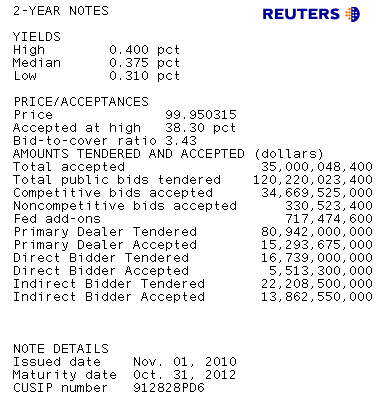

Treasury just auctioned $35 billion 2-year notes. This is $1bn less than the previous issue.

The bid to cover ratio, a measure of auction demand, was 3.43 bids submitted for every 1 accepted by Treasury. This is above the five and ten auction averages.

The high yield set another record low at 0.400%, this is 0.8bps below the 1pm "When Issued Yield", which re-illustrates the market's willingess to buy risk-free debt at the yield highs/price lows.

Primary dealers were awarded 44.1% of the competitive bid and 18.9% of what they bid on, both metrics are below average. This is a good thing!

Direct bidders who've been MIA in auctions lately, took down 15.9% of the issue and 32.9% of what they bid on. These results aren't great but they're a much needed improvement over recently fading direct buyer auction aggression.

Indirects took home 39.9% of the auction and 62.4% of what they bid on. This was a strong turnout from indirects for a 2-year note auction.

Plain and Simple: All around strong results. Auction demand was above average, the high yield was lower than the 1pm "When Issued Yield", direct and indirect buyers showed up to steal supply from the street. This comes as a relief after watching a concession get priced into the market. If higher yields/lower prices didn't draw investor demand, I would've been questioning my "play the range until Bernanke plays you" theory.

Here is the $$$ breakdown....

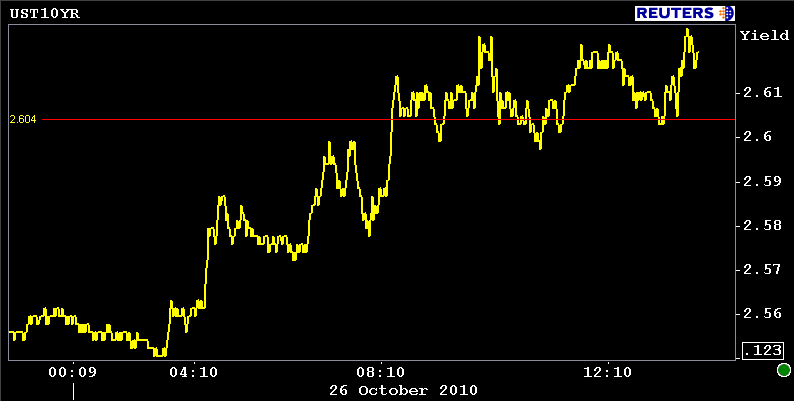

Market Reaction....

None really.

10s haven't ventured far from the 2.60% pivot all day....

The December FNCL 3.5 MBS coupon is bouncing back and forth in a 7 tick price range.