The Monday morning haze is finally wearing off...

On Friday benchmark yields traveled to higher ground as fast money accounts took profits and black box short sellers tested the market's willingness to "buy the dips". Current coupon mortgages performed well for most of the day before an increase in originator hedging (loan supply selling) during after hours trading left production MBS coupon prices sitting near the lows of the week. Those price declines have however reversed course ahead of targeted Federal Reserve Treasury coupon purchases tomorrow in the long end of the yield curve.

7s, 10s, and 30s are leading the recovery rally. 7yr yields are 5bps lower, 10s are 5.3 bps better, and 30yr bond yields have fallen 5.1bps. The 2s/10s curve is 5bps flatter at 215bps wide. Trading volumes are "meh"....apathetic.

As you can see in the chart below, the 10yr note failed to break 2.50% resistance, which happens to be the middle of the 2.46% to 2.54% range. We're headed toward another test of this inflection point in the next hour.

The 5bp 2s/10s bull flattener has pulled "rate sheet influential" MBS coupon prices back into "QEII Sugar High" territory (anything over the yellow line in the chart below). The December FNCL 3.5 is +0-09 at 100-31. 101-00 has been an area of high resistance for 3.5s. The FNCL 4.0 is +0-06 at 103-08. My version of the current coupon is marked at 3.411%. Yield spreads are basically UNCH vs. the curve.

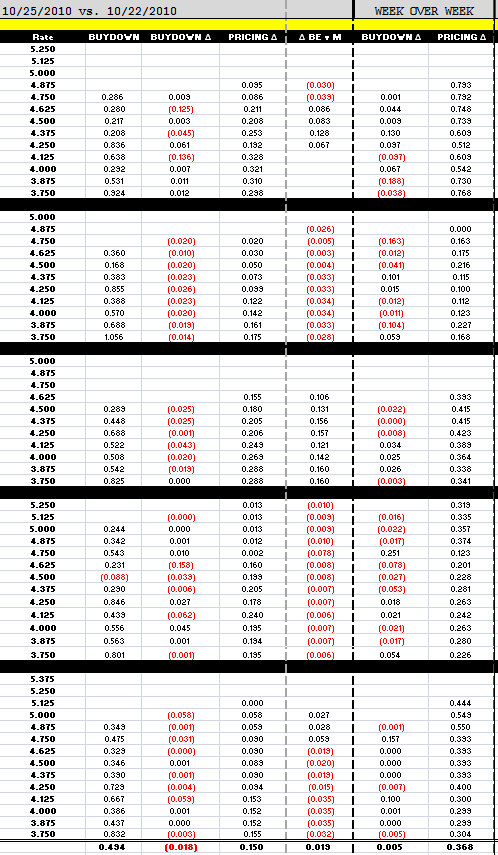

Loan pricing is on average 15bps better than it was on Friday. Day over day improvements didn't erase the 23.6bp rebate reduction we saw heading into the weekend but loan pricing is 36.8bps better than it was last Monday. Overall, loan pricing has been range bound near record highs just like MBS indications.

The bond market reacted counterintuitively to better than expected Existing Home Sales data this morning. Prices rose in low trading volumes and open interest has fallen since Friday...this price action is indicative of SHORT COVERING (black box traders). From that perspective, I remind that we are operating in a marketplace dominated by tactical motivations (short term)...meaning the market is waiting for the Fed to announce more details on QEII and until that happens we are likely to see choppy interest rate behavior dominated by the short term strategies of fast money day traders.

Chairman Bernanke did speak this morning at the Mortgage and Housing Finance Symposium in Arlington VA. He didn't offer up any new hints regarding the potential for alternative monetary policy strategies. I looked for any comments that might imply the Fed was considering a policy effort focused on addressing underwater borrowers and overtightened lending guidelines, but I saw nothing of the sort. More wait and see...

The Treasury will announce the results of a 5-year TIPS auction at 1pm.