Mortgages continued to trade well in a favorable technical environment yesterday. Read "favorable technical environment" as investor demand outpaces loan supply offerings or more simply, more buyers than sellers. It's a cheap crutch to lean on but it applies well as generally low MBS trading volumes have been dominated by fast$ day trading tactics and steady demand for low risk, longer-dated, higher paying bond yields. (vol relatively stable too)

New loan supply sales were less than $2 billion for the third consecutive day this week with originator hedging spread out evenly between 3.5s and 4.0s in 30 year coupons while 15 year paper was primarily offered in 3.5s. With price levels just off record highs, we should be expecting an increase in loan supply sales by originators soon (lock desk hedging). Current coupon yield spreads went out at the tights of the day after firming for most of the session with exception to a brief period of mid-day widening.

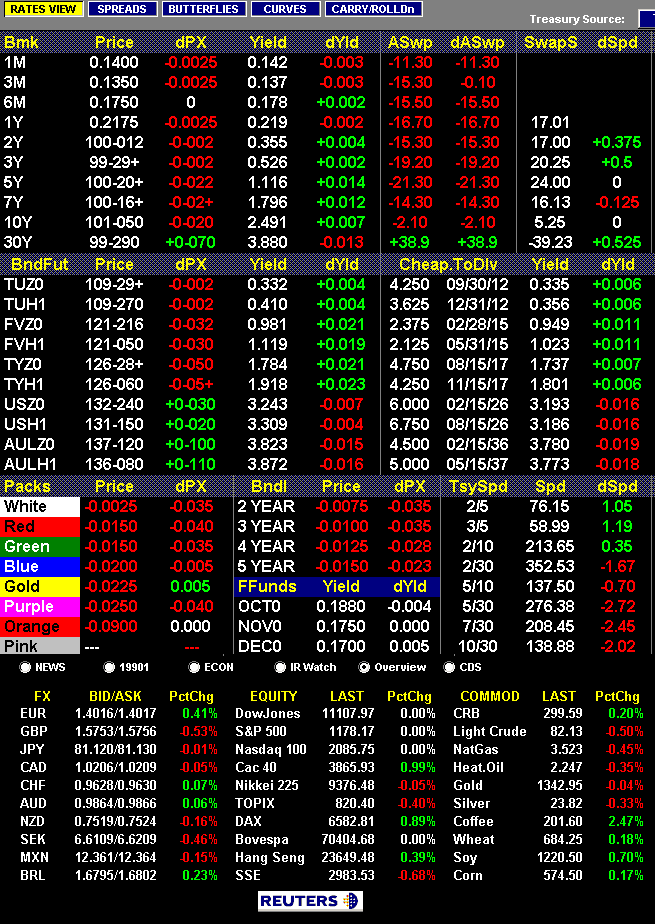

MBS prices were pulled toward record highs again as benchmark TSYs recovered from overnight weakness in Asia. The recovery rally took flight early on in the London session and carried over into domestic trading. Positive price appreciations and trading volume in general did however taper off after 10s failed to breach 2.46% resistance, indicating more guidance on QE is needed if 10s are to break 2.46%. Overall trading volume in the 10 year note was well-below average.

Reprices for the better were reported, 30 year loan pricing was on average 18.6bps better according to my model with the largest rebate improvements awarded in the note rates at or below 4.25%. 4.00% is just about borrower "best execution" again.

Key Events in the Day Ahead:

8:30 ― Economists expect to see 455k Initial Jobless Claims in the week ending Oct. 16, down from a disappointingly high 462k in the previous week. The 4-week average is currently 459k, well down from the 487k average for August but not low enough to indicate robust job growth in the economy. Continuing claims ― the tally of all Americans receiving unemployment benefits (excluding emergency benefits) ― is expected rise to 4.41 million from 4.39 million.

9:45 ― Thomas Hoenig, president of the Kansas City Federal Reserve, speaks in Albuquerque, New Mexico.

10:00 ― Leading Economic Indicators, a composite index credited with signaling changes 3 to 6 months out, is anticipated to repeat a +0.3 level in September. Some factors pointing to growth are higher stock prices, a steep yield curve, and a pickup in building permits.

10:00 ― Philadelphia Fed Survey jumped seven points in September but remained in contraction at -0.7. This month, the increase is set to be smaller, but it should be be enough for the sector to see growth. The consensus forecast is +2.0.

10:00 ― James Bullard, president of the St. Louis Fed, delivers opening remarks to the Annual Economic Policy Conference in St. Louis. His talk is “Frictions in Financial and Labor Markets.”

11:00 ― Treasury announces the terms of auctions to be held in the following week. Maturities to be offered include 2s/5s/7s and 5 year TIPS

Market Levels....

S&P futures are +5.25 at 1180, just off the overnight high.

10s are UNCH at 101-06 yielding 2.486%. The 2s/10s curve is UNCH at 213bps wide. Overnight trading flows were quiet.

The December FNCL 3.5 is +0-01 at 101-06. The December FNCL 4.0 is +0-02 at 103-14.

The dollar index is -0.19%, oil is -0.33 and gold is -0.04%,