Stocks are flagging lower and positive price appreciations across the curve have led rate sheet influential MBS coupons to their session highs after several successful retests of a highly trafficked internal trendline.

The December delivery FNCL 3.5 is currently +0-03 at 100-28. Yield spreads are moving modestly wider as TSY rally and swaps play follow the leader. I've got the production coupon marked at 3.418%. Yield spreads are as follows: +91.8bps/10yTSY, +85.4bps/10yIRS, +230.8bps/5yTSY.

I called attention to all the traffic around the above discussed internal trendline. The FNCL 3.5 runs into price resistance at 101-00.

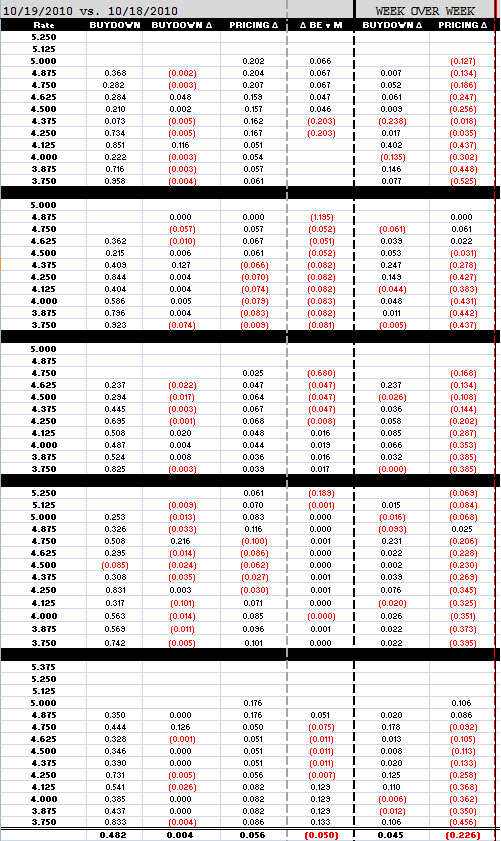

Loan pricing is pretty flat on average. Higher note rates have seen the largest day over day rebate improvements. Current coupon note rates are improved 10bps at most. Week over week, loan pricing is 22.6bps worse, on average. This time last week loan pricing was just off record highs so a 22.6bps difference isn't a big deal, unfortunately when you look closer you'll notice that par note rates are in much worse condition than note rates over 4.375%.

4.125% is Best Execution for a well-qualified consumer. 4.25% is more likely to be offered though.

One of the majors released weaker rate sheets, so too did a few of the mid-majors and regionals, with that in mind, reprices for the better are possible (if your pricing was worse this AM).