830 data is out. Jobless Claims once again disappointed, the Trade Deficit was wider than expected, and Producer Prices were a bit warmer than forecast.

As the data hit screens bond yields began to rise in unison with a knee jerk uptick in equity futures, but price levels quickly reversed course in both markets. The benchmark 10yr note traveled back to the middle of its overnight yield range while S&Ps moved to retest yesterday's lows. Rate sheet influential MBS coupons are holding their own vs. benchmarks but prices are expected to come under pressure as traders look to build in a concession before the long bond auction.

S&Ps are currently 10s are currently -3.50 at 1170.75. Stocks should find support here....

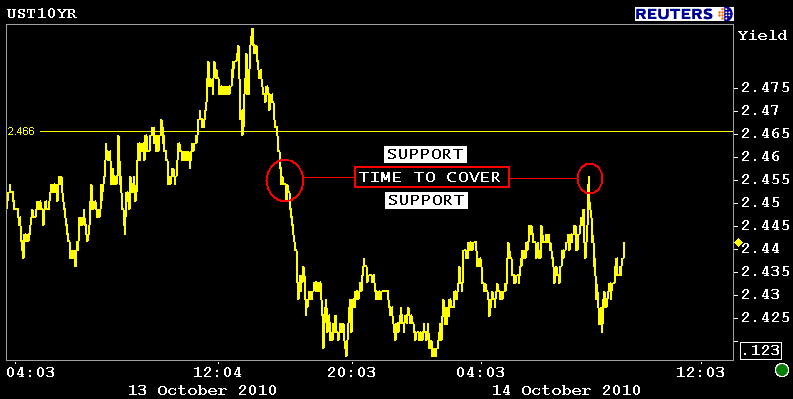

10s are -0-03+ at 101-21 yielding 2.434% (+1.2bps). Price action in the long end of the curve is indicative of short covering (profit taking)...

The December delivery FNCL 3.5 is -0-02 at 100-29. The FNCL 4.0 is -0-01 at 103-03. This is an internal trend line pivot for 4.0s. BTW I am using the 4.0 chart simply because I already had my techs drawn...

The long end of the curve is outperforming at the moment, thanks to short covering, but I would say if stocks decide they are ready to rally at 1170 support, bond traders would gladly welcome the opporunity to cheapen up the long end of the curve ahead of $13 billion 30s at 1pm.

Rate sheet influential MBS prices are basically flat but likely heading lower ahead of the bond auction (IMO). Reprices for the better were not widespread yesterday but were definitely due. If your lender didn't pass along those gains there is room to cushion MBS price losses today, if pipeline capacity allows for it. If your lender did reprice for the better yesterday afternoon, rate sheets should be slightly worse.