Treasury just reopened $21 billion 2.625% coupon bearing 10-year notes. Auction demand was "meh", not great, not terrible, just "meh".

The bid to cover ratio, a measure of auction demand, was 2.99 bids submitted for every 1 accepted by Treasury. Although this is below the five and ten auction averages (3.11 and 3.10) and the weakest BTC ratio since May, it's hard to complain when Treasury is able to choose from 3 different bids.

The "high yield" was 2.475%, the lowest "high yield" on record for a 10yr note auction. The "high yield" had a tiny tail vs. the 1pm "When Issued" yield of 2.477%. This tells us the market was willing to buy supply but only if the Treasury was willing to sell at a cheaper price.

Just like yesterday, primary dealers added more inventory than usual, taking down 47.8% of the competitive bid and 23.7% of what they bid on. Both metrics are above average, which explains why the auction tailed pre-auction WI.

Direct bidders (bond fund managers like Vanguard and PIMCO) were awarded 10.7% of the reopening and 29.6% of what they bid, both metrics were below average. On the bright side, this is an improvement from the September 10yr reopening when directs added 6.9% of the issue, so this is an improvement, regardless of the debt being more expensive.

Indirect bidders, largely thought of as overseas buyers, took home 41.5% of the competitive bid and 67.6% of what they bid on. Indirects were the most aggressive bidders, this is evidenced via their above average hit rate (67.6%), but this auction takedown was MUCH MUCH less than the September award of 57.7%.

Plain and Simple: It is widely anticipated that the Fed will announce QEII in the not so distant future, which should push bond prices higher and lead yields lower. From that perspective one would assume we'd be seeing investors grabbing longer dated debt before it gets even more expensive, but auction demand didn't reflect that theory today. This leads me to believe one of two things: (1) QEII is already baked into valuations (2) Perhaps the Fed's desire to force investors further out the credit curve via lower interest rates (higher opportunity cost of savings) is already in process? Get your money out of your mattresses and put it to work!

Market Reaction...

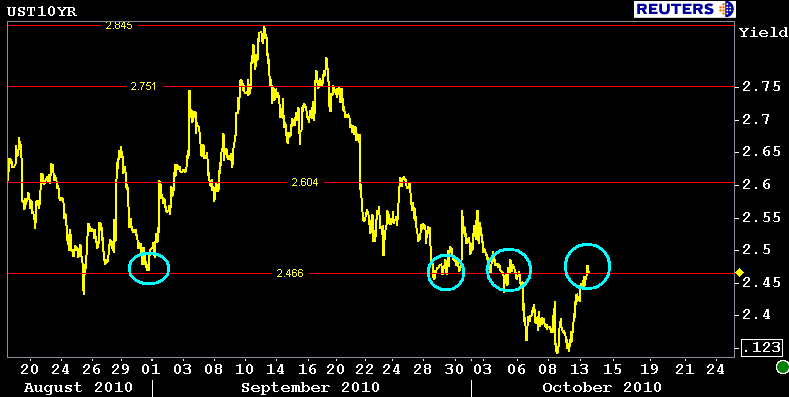

Benchmark 10s are -0-12+ at 101-09 yielding 2.477%, 4.5bps higher on the day. This is a key support level for 10s....if yields are to reverse course, now would be the time.

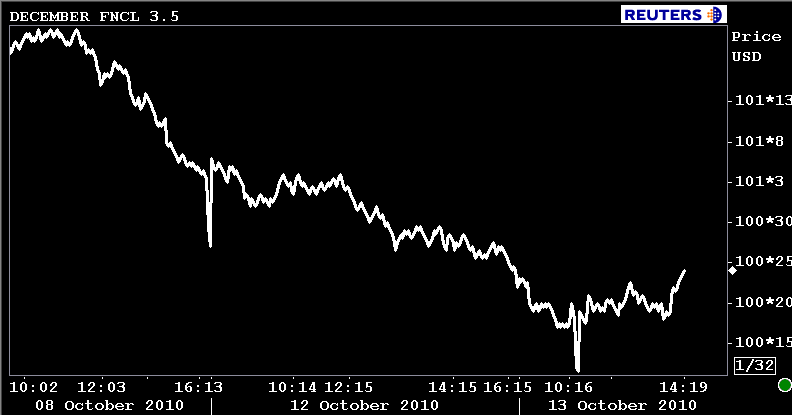

The December delivery FNCL 3.5 is +0-02 at 100-24, improved vs. pre-auction indications. The December delivery FNCL 4.0 is +0-03 at 102-31, this is the session high print.