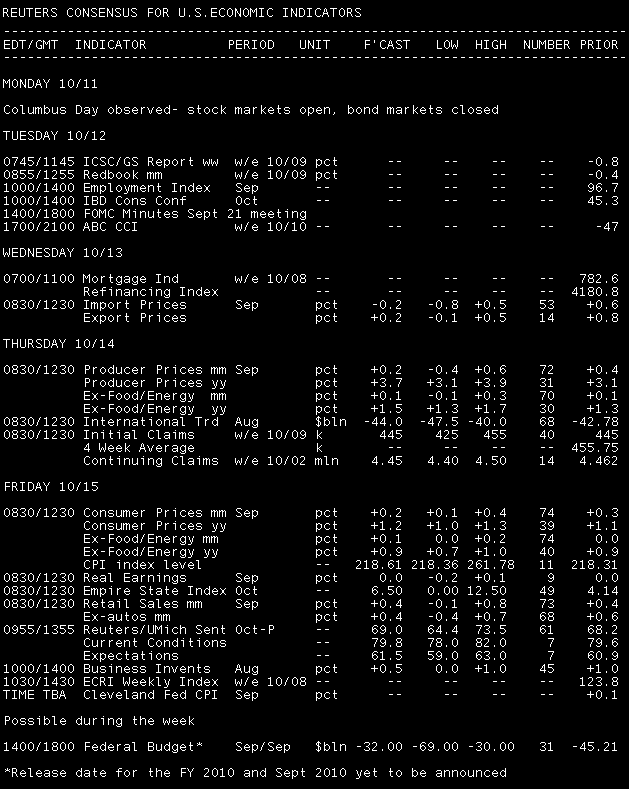

Key Events This Week:

Tuesday:

11:45 ― Thomas Hoenig, president of the Kansas City Federal Reserve, speaks at the NABE annual meeting in Denver on economic outlook and monetary policy challenges.

2:00 ― The holiday-shortened week begins on a fairly slow day until the afternoon when the Federal Reserve releases the FOMC Minutes for its Sept. 21 meeting. The results of that meeting were relatively tame in terms of new policy, but it marked the second time the Fed spoke of introducing a second round of quantitative easing, which many expect to be implemented come November. With several Fed officials on the speaking circuit this week (incl. Bernanke on Friday), QE2 is sure to be a hot topic this week.

“The Fed has made clear that the current level of inflation is not consistent with their mandate,” said economists at Deutsche Bank. “We continue to expect an expansion of QE at the November Fed meeting. As such, from now until November 3, market participants will be focused on divining policymakers’ most likely approach to QE as well as scrutinizing the incoming inflation data.”

Meanwhile, economists at Nomura say the Fed has already laid the groundwork for a resumption of quantitative easing. They hope the September minutes will offer details “on the potential scale and scope of the program, as well as any complementary measures.”

“Other than making the case for further QE, we think the minutes could include a discussion of other available options,” they added. “This would include inflation and/or price targeting, cutting the interest rates on excess reserves, buying agency securities and perhaps yield targeting for Treasuries. Unfortunately, the minutes will not include revised forecasts ― fresh figures will not be available until 24 November.”

Treasury Auctions:

- 11:30 ― 3-Month Bills

- 11:30 ― 6-Month Bills

- 1:00 ― 3-Year Notes

Wednesday:

JPMorgan posts earnings. Results are expected to be moderately higher, according to Reuters.

7:00 ― MBA Mortgage Applications fell 0.8% in the week ending Sept. 24 ― applications for purchase rose 2.4% after two weeks of declines. With mortgage rates at historic lows, potential purchasers could be enticed to get into the market now.

“Home purchase applications have been picking up over the last few weeks ― an encouraging sign that the post-tax credit bust in home sales may be coming to an end,” said economists at Nomura. “Refinancing applications have begun to decline but remain at a high level.”

2:00 ― The Treasury is expected to report in its latest Budget Statement that revenues were $32 billion short in September. Estimates range from $30 billion to $42.5 billion. Whatever the result, it adds to a year-to-date fiscal gap of $1.26 trillion, compared with $1.38 trillion in the same 11 months one year ago. It’s unclear if the market will be paying much attention, but with November elections coming up the final 2010 number is sure to figure into political campaigns to reduce the deficit and pin blame.

4:10 ― Ben Bernanke, chairman of the Fed, speaks in a discussion on business innovation at Cleveland Fed event in Pittsburgh.

6:45pm ― Jeffrey Lacker, president of the Richmond Fed, speaks to business leaders, in Chapel Hill, NC.

- Treasury Auctions:

- 11:30 ― 4-Week Bills

- 1:00 ― 10-Year Notes

Thursday:

Google posts earnings results.

8:30 ― The Trade Balance is anticipated to come in short by $44.3 billion in August, with estimates ranging between $40 and $47.5 billion. In the prior report for July, the gap narrowed substantially by $6 billion to $43.8 billion; August forecasts mostly reflect the view that the gap will widen as imports pick up, but some believe the recent narrowing was more than just a blip.

“Although the trade deficit narrowed significantly in July, we thought this was a predictable payback from the sharp widening in the deficit in Q2,” said economists at Nomura, predicting a $40.9 billion trade deficit. “We therefore think July's narrowing will ‘stick’, and in fact continue for at least one more month. For the quarter, we forecast that the net trade balance will add 0.6pp to GDP growth after subtracting 3.5pp in Q2.”

Economists at IHS Global Insight take a more mainstream view. They said the import surge occurring in May and June continues to unwind and said to expect lower imports of autos and consumer goods in both value and volume.

“Imports of petroleum products should decline in value, as lower volumes will outweigh higher prices,” they added. “We expect little change in exports in value terms, but a decline in export volumes. Higher food and raw material prices will prop up export values. We expect volumes to be hurt by a sharp drop in aircraft exports, which spiked higher in July. Overall, we expect trade to be a small drag on third-quarter growth, after being a huge drag in the second quarter.”

8:30 ― The Producer Price Index should provide the context for the Federal Reserve to implement a second dose of quantitative easing. Total and core PPI are anticipated to rise just 0.1% in September, following a 0.4% gain in total PPI and a 0.1% in core PPI a month before. Energy prices weakened last month, food prices rose, while overall consumption remained subdued amid the modest recovery.

Economists said vehicle prices will be a wild card for the core index, as September through November prices can be volatile with auto dealers importing next year’s models.

8:30 ― Initial Jobless Claims are anticipated to come in below the 450k mark for the second consecutive week in the period ending Oct. 9. New claims for unemployment benefits fell 11k to 445k in the last report, and economists now expect another 2k decline. That could be significant insofar as some economists believe it’s the 450k mark that indicates whether the national labor market is growing.

“Initial and continuing jobless claims are expected to remain elevated but significantly lower than its level during the financial crisis when initial claims reached 651K in March 27, 2009,” said economists at Nomura. “We expect continuing claims continue to decline by 12K to 4450K after decreasing four consecutive weeks.”

5:00pm ― Narayana Kocherlakota, president of the Minnesota Fed, speaks about the tools used in monetary policy

Treasury Auctions:

- 1:00 ― 30-Year Bonds

Friday:

General Electric posts earnings results. Profits are expected to be higher even if revenue dips, according to Reuters.

8:00 ― Dennis Lockhart, president of the Atlanta Fed, participates in a Q&A session with the Executive Women of Goizueta, in Atlanta.

8:15 ― Ben Bernanke, chairman of the Fed, speaks at the Boston Fed's conference on Revisiting Monetary Policy in a Low Inflation Environment.

8:30 ― Like its producer prices cousin, the Consumer Price Index should provide the framework for the Fed to initiate a more accommodative monetary policy. Headline prices are set to climb 0.2% in September after rising 0.3% in the prior two months. Despite those hefty gains, year-over-year prices are just 1.2% higher. Core prices ― which exclude volatile food and energy prices, and which are a more significant measure as far as regulators are concerned ― are expected to rise 0.1% after a flat reading in August. The year-to-year change was just 0.9%, well below the Fed’s target level.

“We expect headline and core inflation will increase slightly by 0.2% and 0.1% in September, respectively,” said economists at BBVA. “Our forecast implies that 12-month core inflation will remain stable at 0.9% for the past six months. September inflation numbers will be the last consumer prices release and it will be closely watched by the Fed before its two-day meeting in November 2-3.”

Meanwhile, economists at Nomura said the most important aspect of this report will be the rent-related components.

“After firming throughout the summer, rent inflation cooled significantly last month,” they wrote. “If this trend persists, it will imply downside risks to consensus inflation forecasts, in our view. Alternatively, if rent inflation rebounds, we may need to revise up some of our below-consensus calls. From a policy perspective, we think the CPI reading is unlikely to have a major effect on decisions. Even if the core increased by 0.25% m-o-m, the year-on-year rate would hold at 1%.”

8:30 ― Retail Sales are anticipated to continue at a fairly strong clip in September, but at levels below the previous month. Total sales should rise 0.3% after a 0.4% gain in August, while sales excluding auto purchases should be up 0.4% after a 0.5% boost. Weekly sales reports from ICSC ― which have fallen in 7 of the past 10 weeks ― suggest some downsize risks to the report.

“After getting hammered by falling gas prices, plummeting furniture sales, steep clothing retailer markdowns, and a pullback in auto sales, retail sales are recovering nicely from the rough spot in early summer when the economic outlook seemed to be getting darker,” said economists at BTMU.

“In general, the retail sector is making some headway,” they continued, “while still finding it difficult to generate acceleration in consumer spending because it continues to battle a weak labor market and consumer confidence that has the doldrums.”

8:30 ― The Empire State Manufacturing Survey, October’s first look at regional manufacturing sentiment, should continue indicating that output is growing, but only at modest levels. The index is expected to produce an 8.0 score, up from 4.1 in September but weak compared to the 20+ levels seen from February to June.

“Any further deterioration would signal downside risks to the October ISM index,” said economists at Nomura, who predict a 5.0 level.

10:00 ― A preliminary look at the Reuters / U of Michigan Consumer Sentiment report is expected to show that people are feeling only slightly better this month. Economists forecast a 69.0 score, or 0.8 points up from September’s final reading. Until job markets improve substantially, few analysts will be expecting any surge in confidence.

“The main driver of the persistence of low consumer sentiment is expectations, since consumers do not have hope for a robust recovery on the horizon,” said economists at IHS Global Insight.

10:00 ― Business Inventories, a lagging indicator for August, are predicted to rise 0.4% following a 1.0% jump in September. Forecasts are based on an already-reported 0.1% increase in manufacturing inventories, plus inferences that wholesale and retail stocks went up.