The first few rate sheets released this morning indicated loan pricing would be better by about 25bps today. Upon further inspection, on average, rebate is 29.6bps better than it was yesterday and a whopping 112.2bps better vs. last Friday. Not only is rebate improved, lenders have squeezed their pricing margins considerably.

Check out the ΔBE v M column. That is the spread between BEST EFFORTS delivery pricing and MANDATORY delivery pricing. That basically represents the difference between the mortgage rate pricing and MBS prices. All but one of the majors have tightened margins. Not just a little either...since the 30 year production coupon shifted from the 4.0 to the 3.5, primary/secondary spreads have tightened considerably.

Plain and Simple: The primary mortgage market just got more competitive! Lenders are begging consumers to lock in their loans!!!

EXPLANATION OF LOAN PRICING COMPARISON

Buydowns are the cost of floating down to the next lowest note rate. Buydown costs are matched to the note rate in the same row. For example, the first number in the buydown column is .352%, this is the cost to float down from 5.00% to 4.875%, as a percentage of the loan amount. This is important because it helps an originator determine the best execution rate/points combination for a borrower who has a good idea of how long they intend to live in their home (breakeven on points paid vs. monthly payment savings). In the Buydown Delta column, red is cheaper. Black is more expensive.

The pricing change column is a direct rebate comparison of pricing today vs. pricing yesterday. Red is worse. Black is better.

The BE v M column shows you how margin is changing. RED means more margin. Black means less bps are baked into pricing.

I do not show the actual price lenders are paying for loans. This is too much info. I would get angry emails from lock desks and production managers. I will tell you this though, the comparison is based on raw pricing. There isn't another markup built into my model.

---------------------------------------------------------

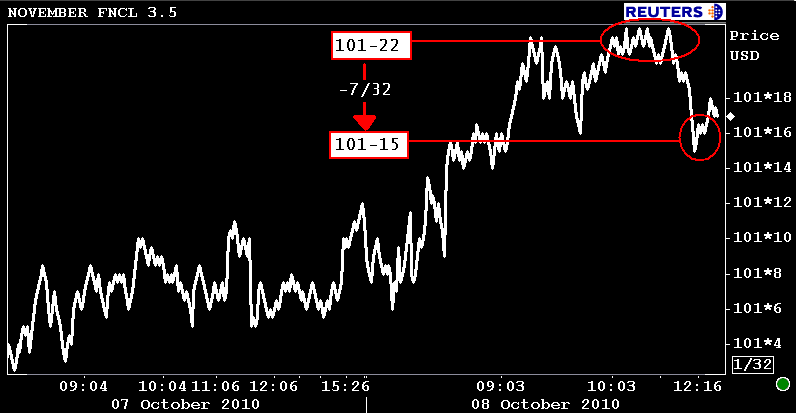

That was the good news, now for the bad...

Rate sheet influential MBS prices are off their session highs. The November delivery FNCL 3.5 is currently +0-06 at 101-17.

3.5s traded as high as 101-22 during prime rate sheet making time, but have moved as low as 101-15. A 7/32 price decline is enough to warrant a repricesfor the worse, especially on a Friday before a long weekend, especially if your lender has seen their pipeline balloon over the past 24 hours.

Beware...