Spurred on by a weak preview of official labor market data to come, the bond market upped the anti on quantitative easing this morning when the 10 year note broke 2.40% resistance and "rate sheet influential" MBS coupons moved outside the confines of our lock/float range. This implies QEII hasn't been totally baked into bond valuations and rates could go lower.

The long end of the yield curve is leading the rates rally. The 2s/10s curve is 8bps flatter at 199bps and the 2s/30s curve is 8bps flatter at 326bps. This doesn't mean TSYs aren't rallying across the curve though. New record low yields were hit by 2s, 5s, and 7s.

The 10 year note is currently +29/32 at 102-07+ yielding 2.369%. At one point 10s were up over a full point at 102-11 yielding 2.359%. If QEII is to send yields lower via TSY purchases , 2.20% is my target. I do not think buying TSYs is the solution though. In fact I think we need to see higher rates. Seems like the "shock and awe" strategy is still an option for the Fed. They have to spook the market's into fearing inflation...

Mortgages are following TSY prices higher, albeit from a widening distance. Our lock/float range has been broken!!!

The November FNCL 4.0 is currently +11/32 at 103-03. Positive price appreciations have stalled out at internal trendline resistance. If TSYs rally down to 2.20% after NFP on Friday, "rate sheet influential" MBS will lag greatly. Fortunately duration demands do create enough liquidity in the TBA market to allow lock desks to hedge with 3.50% 30yr coupons, in size. This means mortgage rates could go as low as 3.75% in the near term...

LOCK DESKS: Time to add 3.50s!!! Time to deliver 3.50s!!!

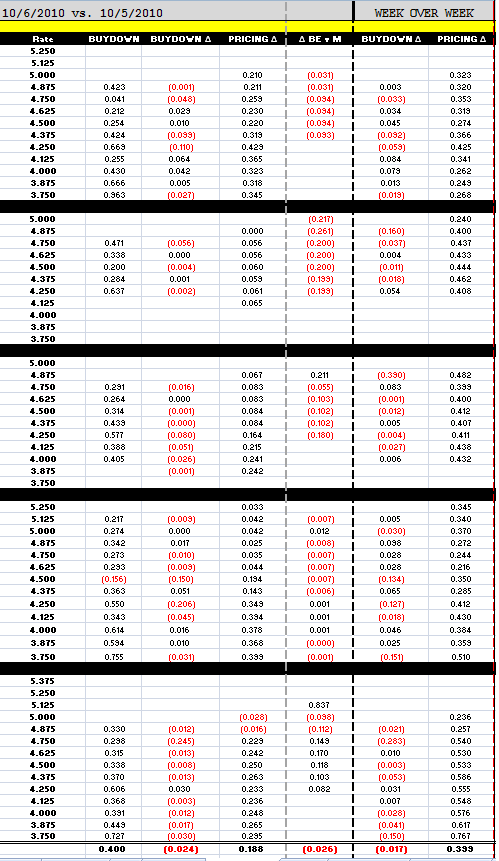

Actually I shouldn't say "could go" because mortgage rates "have gone" as low as 3.75%.....but for the most part 3.875% is a more economically efficient option for 3.50% delivery and is therefore as low as most lenders will probably go. Par 3.875% are already on the board. Loan pricing is as aggressive as it's ever been.....

ALERT: Do not forget the "I have filled my pipeline and need to slow production" reprice for the worse. If your lender is pushing turn times longer, your loan pricing is highly susceptible to these reprices for the worse. Now if your lender was a little lite on rebate this morning and has been slow to fill their buckets, you might see a reprice for the better soon.