Not a great week. Not a terrible week. So/so seems like an appropriate description for the mortgage market over the past 5 days.

Rate sheet influential MBS prices went out 7/32 higher than they closed last Friday. I've got the production coupon marked at 3.633%. 3.50 MBS coupon supply traded forward in size on Monday and Tuesday. This led mortgage rates back down to record lows. Unfortunately a rush of loan sales from lock desk (hedging at the price highs) combined with three oversubscribed TSY auctions left dealers feeling a bit bloated with debt inventory. At that point TSY started experiencing profit taking (expected when 10s move below 2.50%) and MBS were struggling to attract buyer demand (lower and wider = bad), so dealers were forced to lower their asking prices, which increased buying interest at the yield highs/price lows.

I described this action as MBS/TSYs being "bid wanted" or "well offered". While we did hear reports of a few pockets of increased real money demand (extension trade), MBS trading flows were generally dominated by day traders (relative value) and originators hedging their pipelines this week.

The November delivery FNCL 4.0 closed +0-03 at 102-18. We failed to break internal trendline resistance but that doesn't mean there isn't room for FNCL 4.0 prices to tick higher. If prices do rally higher, we quickly run into two more layers of resistance. The next move is entirely dependent on data and Fed rhetoric...

There were scattered reports of reprices for the better today, but nothing exciting. You did get back a few bps but quotes below 4.25% are considerably more expensive than they were on Tuesday and Wednesday morning. Rebate is essentially unchanged vs. last Friday.

The main driver behind the bond market at the moment is the potential for further Federal Reserve quantitative easing. This means economic data will play a major role in the direction of interest rates in the days/weeks/months to come. If data disappoints on a consistent basis, 10s will likely retest 2.40% resistance. At that point we will find out if QEII is already baked into bond valuations or not. In the mean time the range trade is in play...10s between 2.50 % and 2.75%...the November delivery FNCL 4.0 between 103-00 and 102-00. Play the range until the range plays you.

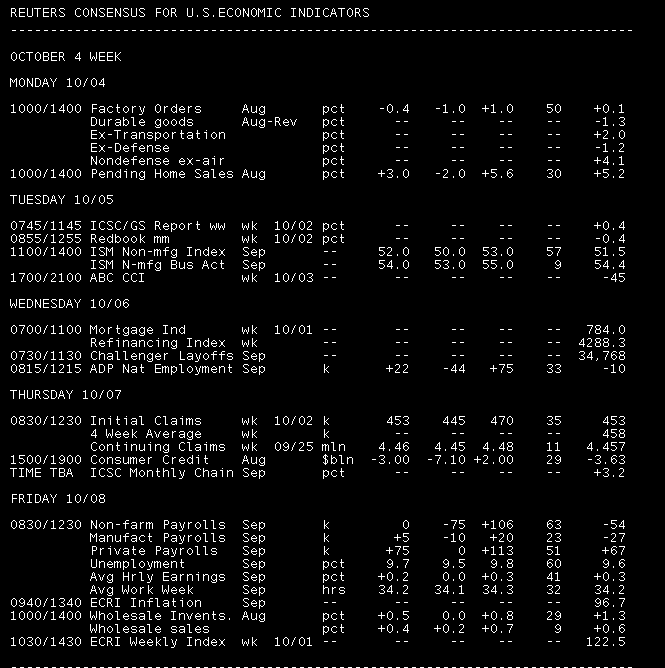

The gets started with Factory Orders and Pending Home Sales. Again, directionality is entirely dependent on data and Fed rhetoric.

See you on Monday morning....