Quick Recap

- 10s Under 2.50%. Yield Curve Crushed (in a good way)

- Mortgage Rates Improve. Loan Officers Disagree?????

- MBS Underperformed into Higher Prices, Negative Convexity an Illusion in 4.0s.

- Another RAPID REFI RUMOR hits the tape

- NOV. FNCL 4.0 ends day just above key support level at 102-21

- Origination Supply > $2bn. Over half was 3.5s. Supply a Source of Weakness.

- July S&P/C-S HPI +0.6%. Consumer Confidence Crappy

- Low Yields = High Opportunity Cost of Saving. 5s Go Off at Record Low Yields

IT HAPPENED. AGAIN.

It happened yesterday but I didn't make a big deal about it because I wanted to see how lenders would play it out today. Then it happened again today. And I am thinking it will be a good thing for mortgage rates.

"IT" is 3.5 MBS coupon supply. "IT" is almost $2 billion in 3.5 MBS coupon supply in the past two days. "IT" is the PHANTOM COUPON and it's made another appearance.

Yep. 3.5 coupon origination supply is trading. While flows have been slow over the past two days, there has been a noticeable increase in 3.5 MBS coupon sales by lock desk (hedging). This implies lenders are preparing to push mortgage rates below 4.25%, again. This makes sense, the last time these rate quotes were offered, the front month FNCL 3.5 coupon was bid at 101-10+. We almost hit that price again today.

Looking at my data, rates below 4.25% should already be on the board. The day over day improvement was 18.4bps, but check out how friendly lenders got with rates at or below 4.25%. Buydown ratios improved too. The mortgage rate rally was two-fold today.

-------------------------------------------------------

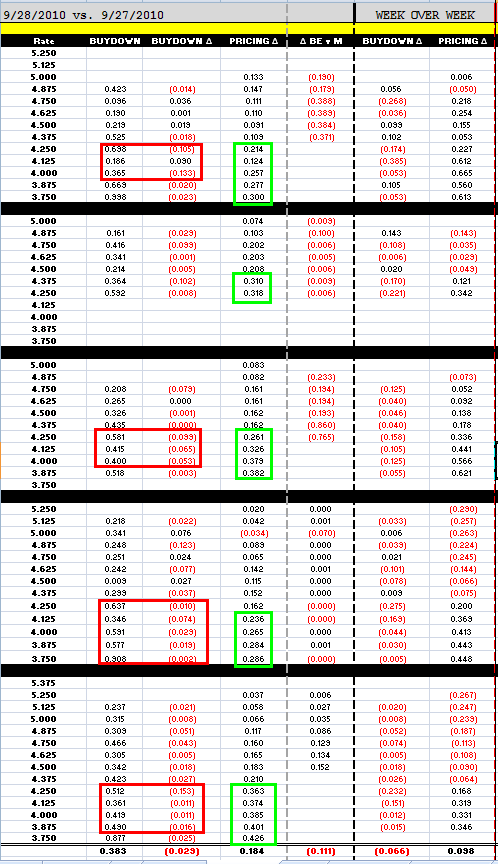

EXPLANATION OF LOAN PRICING COMPARISON

I track the daily price loan pricing strategies of the five major lenders.

Buydowns

are the cost of floating down to the next lowest note rate. Buydown

costs are matched to the note rate in the same row. For example, the

first number in the buydown column is .352%, this is the cost to float

down from 5.00% to 4.875%, as a percentage of the loan amount. This is

important because it helps an originator determine the best execution

rate/points combination for a borrower who has a good idea of how long

they intend to live in their home (breakeven on points paid vs. monthly

payment savings). In the Buydown Delta column, red is cheaper. Black is

more expensive.

The pricing change column is a direct rebate comparison of pricing today vs. pricing yesterday. Red is worse. Black is better.

The BE v M column shows you how margin is changing. RED means more margin. Black means less bps are baked into pricing.

NOTE TO CONSUMERS: I do not show the actual price lenders are

paying for loans. I would get angry emails from lock desks and

production managers.

My data indicates mortgage rates are already back at record lows, but anecdotal evidence seems to indicate otherwise. I heard some grumblings from the trenches this morning after I announced a loan pricing war was in the works. Some loan officers claim recent rebate improvements to have been on the lite side. If you feel your lenders are holding out, you are likely dealing with a lock desk who doesn't need anymore deals in their pipeline. Whether it be a function of operational capacity constraints or a warehouse line that is maxed out and waiting to be turned...the first place a lender looks to slow the spigot of business is rate sheets!

But I'm also hearing scattered reports of rate quotes being offered near the record lows we witnessed in late August. Some desks seem to be going for the gusto. Possibly because 4.25% wasn't luring float boaters ashore? Perhaps the refi market is sputtering and lenders are chumming the waters for qualified borrower?Maybe secondary has a few buckets of UFMIP floaters, folks who have app'd but haven't committed to a rate yet. How many of you are floating for the Oct.4 change in FHA UFMIP?

Either way, secondary would be looking to pull-through as many of these borrowers as possible, so they would be defensive of a competitor who was chumming the waters with lower cost deals. If you are privy to par pricing under 4.25%, remember, the last time mortgage rates dipped below 4.25%, it was only for a brief time. This is one of those opportunities to "lock at the mortgage rate lows". If you aren't seeing it yet, hopefully tomorrow brings better bps.