Ok so I waited a little longer to write this morning so I could see how the market played this modest move higher in yields. Plus I wanted to get a look at pricing before saying anything that might spook floaters.

The bad news is we're seeing benchmark yields tick higher today. Rising rates have led production coupon MBS prices lower, through a key layer of support all the way down to another. The November FNCL 4.0 is currently -7/32 at 102-12 yielding 3.645% (+2.4bps).

We're basically following Treasuries lower. There is little activity in the TBA MBS market. TSYs are slow too. It's a Friday....

It's been awhile since I've put BAM BAM on a chart, I was gonna do it today but there would be too much confusion. We've seen lots of touches on these inflection points over the last 45 days. The range is still play. With TSY supply ahead, the door is open for the FNCL 4.0 to retest the lower side of the range.

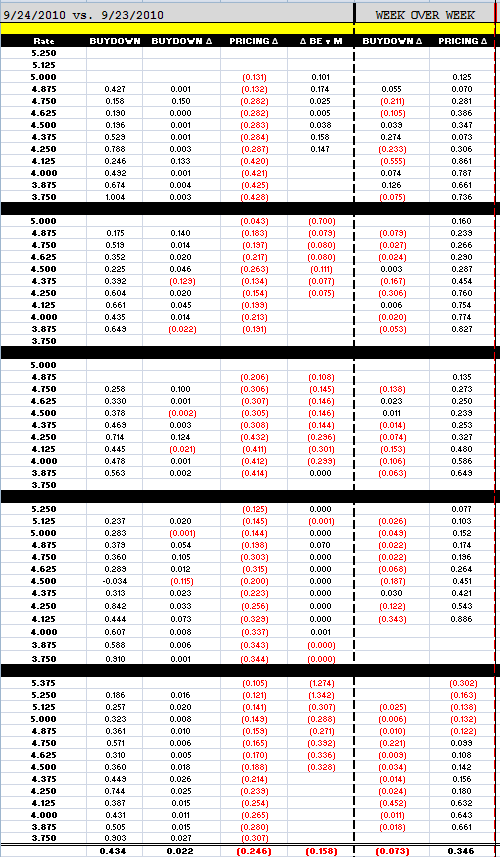

The good news is loan pricing isn't too too terrible into these lower MBS levels. Rebate was up about 75bps on Wednesday. In the last two days we've lost 0.375 of that, factoring in the first three days of the week, pricing is +34.6bps better than it was last Friday. So while you could've cashed out at the rebate highs on Wednesday, if you've been floating through the range trade, you're still in better shape than you were last week (said Pollyanna).

If you've been locking loans, let me know how much volume you've just committed. I am curious to hear if maybe lock desks overhedged into this latest shift in mortgage rates.