The Labor Department this morning informed us that Initial Jobless Claims increased by 12,000 heads in the week ending Sept. 18. This was worse than forecast and the first time in five weeks that jobless claims failed to improve or at least hold steady. The previous two reports were revised higher as well, adding 7,000 more claims to the monthly total. The Labor Department said there was no funny business embedded in this data, unlike the previous two which were distorted by several states taking a guess (estimating) at their weekly claims.

Below is a recap....

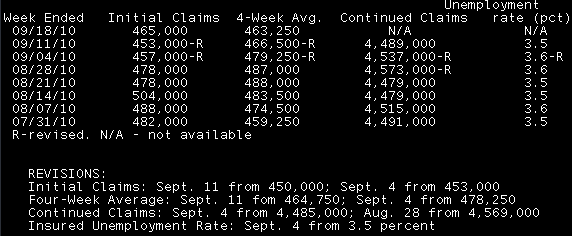

RTRS-US JOBLESS CLAIMS ROSE TO 465,000 SEPT 18 WEEK (CONSENSUS 450,000) FROM 453,000 PRIOR WEEK (PREVIOUS 450,000)

RTRS-US JOBLESS CLAIMS 4-WK AVG FELL TO 463,250 SEPT 18 WEEK FROM 466,500 PRIOR WEEK (PREVIOUS 464,750)

RTRS-US CONTINUED CLAIMS FELL TO 4.489 MLN (CON. 4.460 MLN) SEPT 11 WEEK FROM 4.537 MLN PRIOR (PREV 4.485 MLN)

RTRS-US INSURED UNEMPLOYMENT RATE FELL TO 3.5 PCT SEPT 11 WEEK FROM 3.6 PCT PRIOR WEEK (PREV 3.5 PCT)

Plain and Simple: YAWN! We learned nothing new from this release. The labor market is not improving, just like the rest of the economy it is stagnant. I am not 100% sure, I will have to check, but I believe this report covered the NFP survey week. If it did, it would imply we should be expecting positive job creation in the September Employment Situation Report. Keep this on your radar.

Market Reaction....

Bonds rally. Stock futures fall.

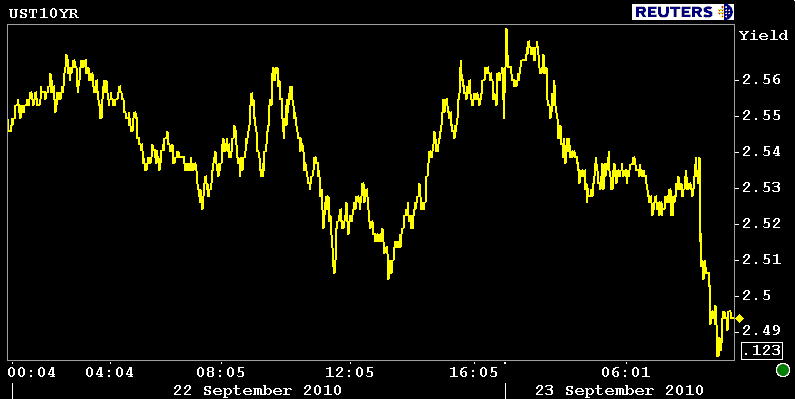

After the data flashed the yield curve flattened another 4bps, 2s/10s are now at 207bps. The benchmark 10yr note yield has moved below 2.50% resistance, currently bid +17/32 at a price of 101-05, yielding 2.494%. I expect 10s to trade in a range between 2.50% and 2.75%. Between 2.40% and 2.50% is basically no man's land in terms of technicals, but it is possible that we see a retest of 2.40% if EHS data is poor. But 2.40% has been rejected aggressively in the past month, so I would expect to see some skittish behavior as (if) 10s approach 2.40%.

Plain and Simple: Anytime we see 10s move below 2.50% I would be watching for profit taking.

After crossing through 2.50% resistance, 10s have paused from further positive progress...this is in anticipation of 10am EHS and LEI data.

Mortgages are trading wider to the TSY and swap curve. Besides the fact that MBS tend to lag benchmarks into a rally (nominal basis), "rate sheet influential" MBS" are likely lagging because dealers added inventory yesterday (they got long, maybe too long). This because lock desks were selling loan supply! About $2.5 was offered, mostly in 30 year 4.0 coupons but there was a teeeny tiny bit of 3.5 origination activity as well. This means there s/be scattered reports of rate quotes at or below 4.25%. Just remember those quotes are the most sensitive to changes in benchmark yields.

The November FNCL 4.0 is currently +0-04 at 102-25. I've got the production MBS coupon marked at 3.601%. Our technical range is clearly in play. If you are "playing the range until the range plays you", you should be hearing me send subliminal SELL signals. Read "sell" as lock in, even if 10s test 2.40% again, MBS will just widen. Lock desk should be adding more coverage soon (implies I think we've hit a near term price top) so this just furthers the notion that we should be expecting MBS to lag TSYs into a continued benchmark rates rally. Plus lock desks will be adding margin to loan pricing as they fill their pipelines with production, either way I am sending lock signals on short term positions.

EHS and LEI at 10AM.

S&Ps currently -7.75 at 1122.