Good Morning. No really, GOOD MORNING!!!

Loan pricing is about 75 bps better in the past three days. 32bps were added to rate sheets between Monday afternoon and Tuesday morning. Plus the 25bps lenders gave you yesterday afternoon following the release of the FOMC statement. Then we add another 17.4bps in rebate, which was passed along this morning. That brings the grand total to 74.4bps! Nice little turn around in rebate.....

Although it's still very expensive to quote a rate at or below 4.25%, buydowns are cheaper too. Run a breakeven before you let a borrower buy down their rate though. Make sure they understand how long it will take to recover the points they're paying at the table.

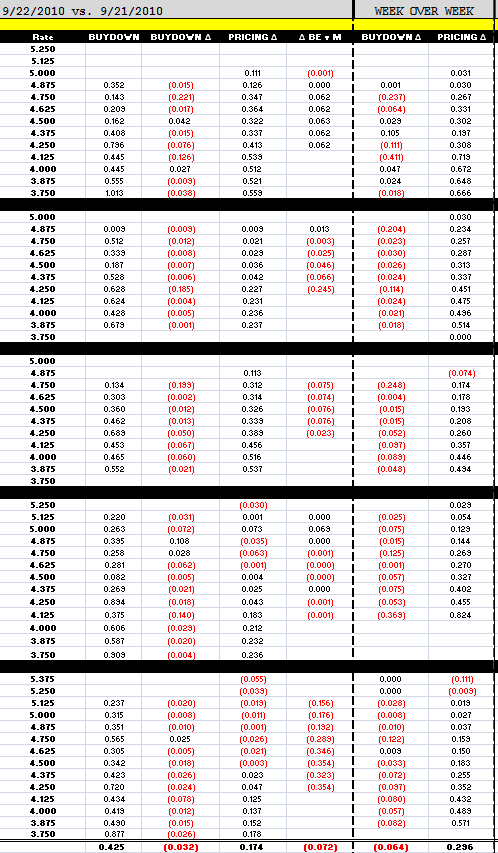

EXPLANATION OF LOAN PRICING COMPARISON

Buydowns are the cost of floating down to the next lowest note rate. Buydown costs are matched to the note rate in the same row. For example, the first number in the buydown column is .352%, this is the cost to float down from 5.00% to 4.875%, as a percentage of the loan amount. This is important because it helps an originator determine the best execution rate/points combination for a borrower who has a good idea of how long they intend to live in their home (breakeven on points paid vs. monthly payment savings). In the Buydown Delta column, red is cheaper. Black is more expensive.

The pricing change column is a direct rebate comparison of pricing today vs. pricing yesterday. Red is worse. Black is better.

The BE v M column shows you how margin is changing. RED means more margin. Black means less bps are baked into pricing.

I do not show the actual price lenders are paying for loans. This is too much info. I would get angry emails from lock desks and production managers. I will tell you this though, the comparison is based on raw pricing. There isn't another markup built into my model.

----------------------------------------------------------

The November FNCL 4.0 is trading +0-04 at 102-27. I've got the production coupon marked 1.7bps lower at 3.588%. Yield spreads are wider on a nominal basis and in OAS models. We should be expecting secondary managers to start selling forward loan supply very soon. View this additional coverage as secondary locking in at the price highs. When supply is offered, L.Os should consider locking up short term floats.

Our range is clearly still in play. Check out the technical bounces at targeted inflection points....

While I wouldn't say it's been a slow NY session in the bond market, volume isn't huge. Doesn't matter though, the volume we have seen has been generated by buyers.

The 2s/10s yield is another 6bps flatter at 210bps, production MBS coupons are trading to shorter hedge ratios, and benchmark 10s have moved all the way through our PANIC ZONE back down to 2.50%. This is where we should expect to see profit taking/dealers go the other way, especially if stocks can catch a bid off their session lows. (S&P -5.00 at 1129.75. Low print = 1126.50). While this implies we might see yields move marginally higher in the near term, the overall environment remains highly supportive of low mortgage rates.

WE ARE OFF HIGH ALERT!!!

The chase for yield continues. Don't miss my coverage of the FOMC statement, especially the part discussing inflation being below the Fed's target. This implies the Board is concerned they are losing control over price levels. READ MORE