Interesting day. All sorts of crosswinds and chopatility out there....

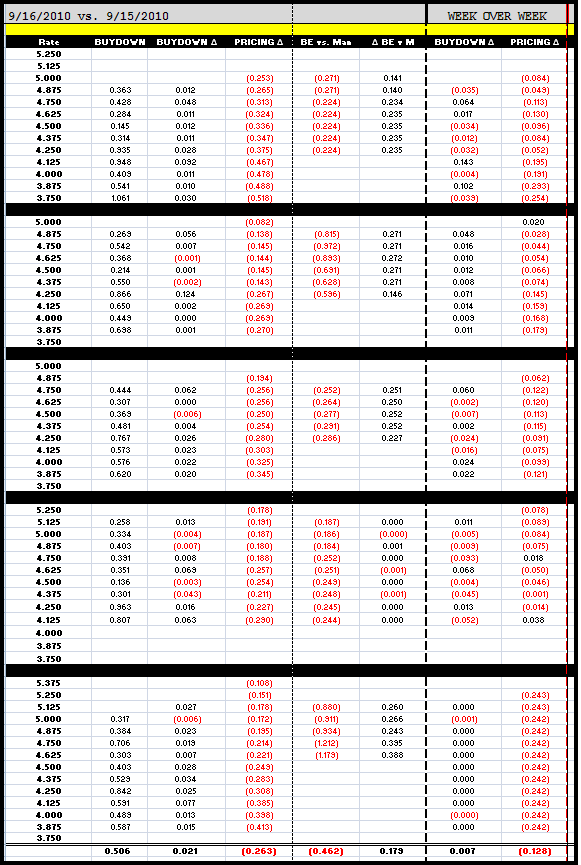

10s traded in a 10bp yield range. FNCL 4.0s traded in a 12 tick price range. Lenders repriced for the worse. Lenders repriced for the better. The November FNCL 4.0 went out -0-02 at 102-04. September has not been friendly to mortgage-backeds.

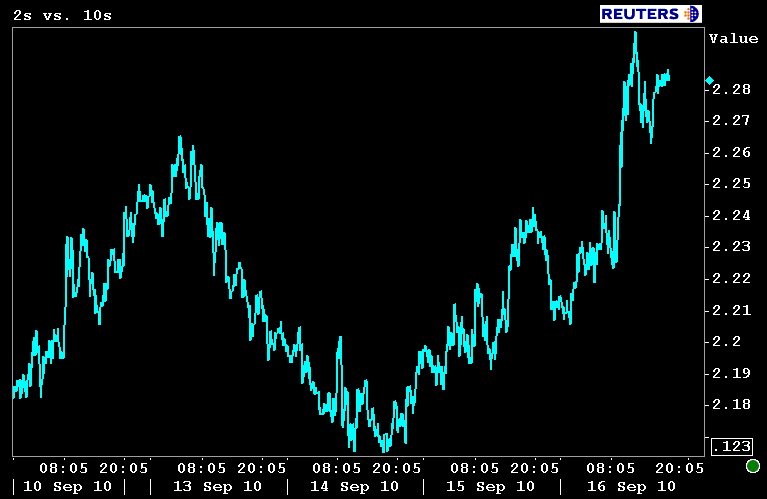

That sure does look like a downtrend doesn't it?

Mortgage rates ended the day higher. Of the majors, loan pricing was 26.3bps worse on average. Only two of the big boys repriced worse while a handful of mid-majors and regionals recalled pricing in the lunch hours. Week over week, rebate is 12.8bps worse. Check out how rough secondary treated note rates at or below 4.25%.

REMEMBER: PAR NOTE RATE PRICING IS THE MOST SENSITIVE TO RISING YIELDS

The most obvious development of the day in the bond market was the steeper shape of the TSY yield curve. 2s/10s ticked as wide as 230bps before real money bargain buyers stepped in to firm things up. 2s/10s finished 5bps steeper at 228 wide. This leaves 2s/10s roughly 10bps steeper in the last two days, which should be setting off alarm bells, but there is a logical explanation...

READ MORE ABOUT THE SHAPE OF THE YIELD CURVE

We can't overlook the Fed's open market TSY operation today, which was focused on the short end of the curve. The desk waved in $1.379bn in TSY coupons maturing between March 2012 and February 2013. We also can't forget what's playing out in the currency market at the moment. The Japanese government just sold an estimated $23bn in JPY (Yen). Those funds were likely redirected into the short end of the TSY curve. On top of that, rumors of another Federal Reserve quantitative easing effort, which helped mortgage rates recover earlier in the week, faded today. Last but not least, we can't rule out competition from the corporate debt market either.

All in all the cards were stacked against our benchmark guidance givers today and while MBS played follow the leader, there was localized weakness in our market too, which contributed to spread widening. After $3.5bn+ in loan sales yesterday and another $2.5bn today, a lack of buying interest was apparent. Bid wanted....

We're still playing the range, but that range is running out of room. We get consumer inflation data in the AM. Deflationary fears were a major contributing factor to mortgage rates being offered below 4.25% in August. This makes the bond market extra sensitive to a lack of inflationary pressures. If CPI prints in positive territory, we might be testing the outer limits of our range in the morning. 10s find support at 2.85%....

Although I can point toward logical reasons why the yield curve steepened today, it doesn't mean the curve won't continue to steepen. If this happens in a bearish manner, it would be an unfriendly event for mortgage rates.

WE'RE BACK ON HIGH ALERT...

If you did not read this post, I think it will help explain some of the back and forth behavior of the bond market: Rates Perspective Realignment. Seeking Guidance. Finding the Range