Initial Jobless Claims and International Trade data has been released, the results were not bond market friendly.

Here is a quick recap:

08:30 09Sep10 RTRS-US JOBLESS CLAIMS FELL TO 451,000 SEPT 4 WEEK (CONSENSUS 470,000) FROM 478,000 PRIOR WEEK (PREVIOUS 472,000)

08:30 09Sep10 RTRS-US JOBLESS CLAIMS 4-WK AVG FELL TO 477,750 SEPT 4 WEEK FROM 487,000 PRIOR WEEK (PREVIOUS 485,500)

08:30 09Sep10 RTRS-US CONTINUED CLAIMS FELL TO 4.478 MLN (CON. 4.45 MLN) AUG 28 WEEK FROM 4.480 MLN PRIOR (PREV 4.456 MLN)

08:30 09Sep10 RTRS-US INSURED UNEMPLOYMENT RATE UNCHANGED AT 3.5 PCT IN AUG 28 WEEK (PREV 3.5 PCT)

08:30 09Sep10 RTRS-TABLE-U.S. jobless claims fell in latest week

08:30 09Sep10 RTRS-US JULY TRADE DEFICIT $42.78 BLN (CONSENSUS $47.3 BLN) VS JUNE DEFICIT $49.76 BLN (PREV $49.90 BLN)

08:30 09Sep10 RTRS-US JULY EXPORTS +1.8 PCT VS JUNE -1.3 PCT, IMPORTS -2.1 PCT VS JUNE +3.1 PCT

08:30 09Sep10 RTRS-US JULY GOODS DEFICIT $55.23 BLN, SERVICES SURPLUS $12.46 BLN

08:30 09Sep10 RTRS-US JULY EXPORTS $153.33 BLN, HIGHEST SINCE AUG 2008, VS JUNE $150.57 BLN, IMPORTS $196.11 BLN VS JUNE $200.33 BLN

08:30 09Sep10 RTRS-U.S. JULY CAPITAL GOODS IMPORTS $37.69 BLN VS JUNE IMPORTS $38.27 BLN

08:30 09Sep10 RTRS-U.S.-CHINA JULY TRADE DEFICIT $25.92 BLN VS JUNE DEFICIT $26.15 BLN

08:30 09Sep10 RTRS-US-OPEC JULY TRADE DEFICIT $8.04 BLN VS JUNE DEFICIT $8.94 BLN

08:30 09Sep10 RTRS-US JULY OIL IMPORT PRICE $72.09/BBL VS JUNE $72.44/BBL, +15.3 PCT FROM JULY'09 $62.52/BBL

08:30 09Sep10 RTRS-U.S.-CHINA JULY IMPORTS $33.26 BLN, HIGHEST FOR ANY MONTH SINCE OCT 2008

08:30 09Sep10 RTRS-TABLE-U.S. July trade gap narrowed to $42.78 bln

Market Reaction...

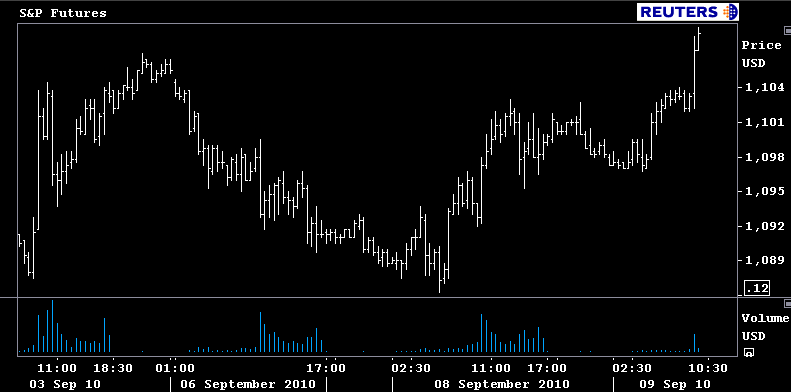

Stock futures rallied up to 1,106, the S&P's high print following a better than expected read on the labor market last Friday (NFP).

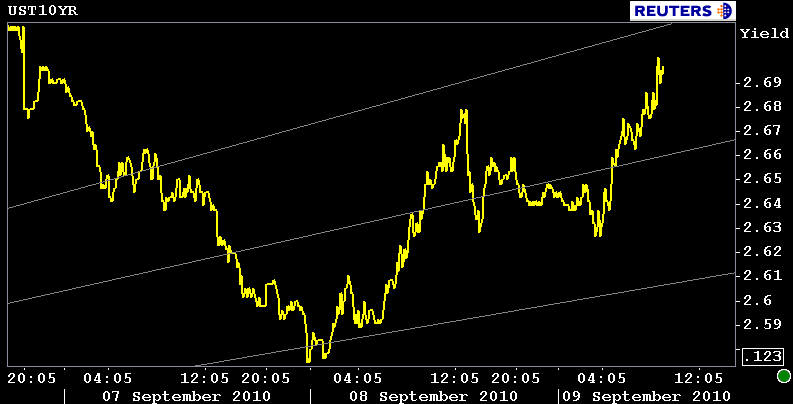

The 10-year Treasury note yield extended its overnight losses and is now -0-11 at 99-13 yielding 2.693% (+4bps). The 2s/10s yield curve is 4bps steeper at 217bps.

The October delivery FNCL 4.0 is -0-05 at 102-16. If lenders take down pricing indications right now, rebate will be worse today.

Both benchmark rates and stock futures are testing key pivot points after 830 data. Government debt traders will lean on the better than expected read on initial claims to allow the long bond to cheapen up before TSY sells $13 billion 30s later this morning. In terms of stocks, trading desks report that investors were reallocating funds from bonds to stocks in the overnight session...is this when the S&P takes a run at a sustained rally? Who knows. This market is so fickle and unwilling to commit. I say play the range until the range plays you...that means we have to assume S&Ps might run up as far as 1130 before we see a significant turn around. The S&P needs to break 1115 first (200 day moving average).